The sun’s finally peeking through the clouds, and the birds are back in full song. You know what that means? It’s spring cleaning time! But while dust bunnies in your house might be easy to spot, what about those sneaky financial cobwebs lurking in your bank statements and spending habits?

In this post we’ll run through some quick spring cleaning tips and general check-in reminders to make sure your finances are in a good place for 2025. So, grab a cup of coffee, grab your statements, and get ready for some financial sunshine!

1. Update Your Budget

Holiday spending sometimes bleeds into the new year, and your 2025 budget might already have fallen off the rails. Don’t be discouraged! There are plenty of easy ways to fix a failing budget and get things back on track.

The biggest key to updating a budget is making sure your spending reflects your current circumstances and values in life. Try to revisit every category in your spending plan, and decide what changes might need to be made. Remember to keep your budget realistic, so you’ll have a better chance of success and sticking to it!

If you feel like your current budgeting system just isn’t working for you, switch it up! Try testing out one of these budgeting techniques, like the 50/30/20 system. This means spending 50% of your income on Needs, 30% on Wants, and socking away 20% into Savings for retirement.

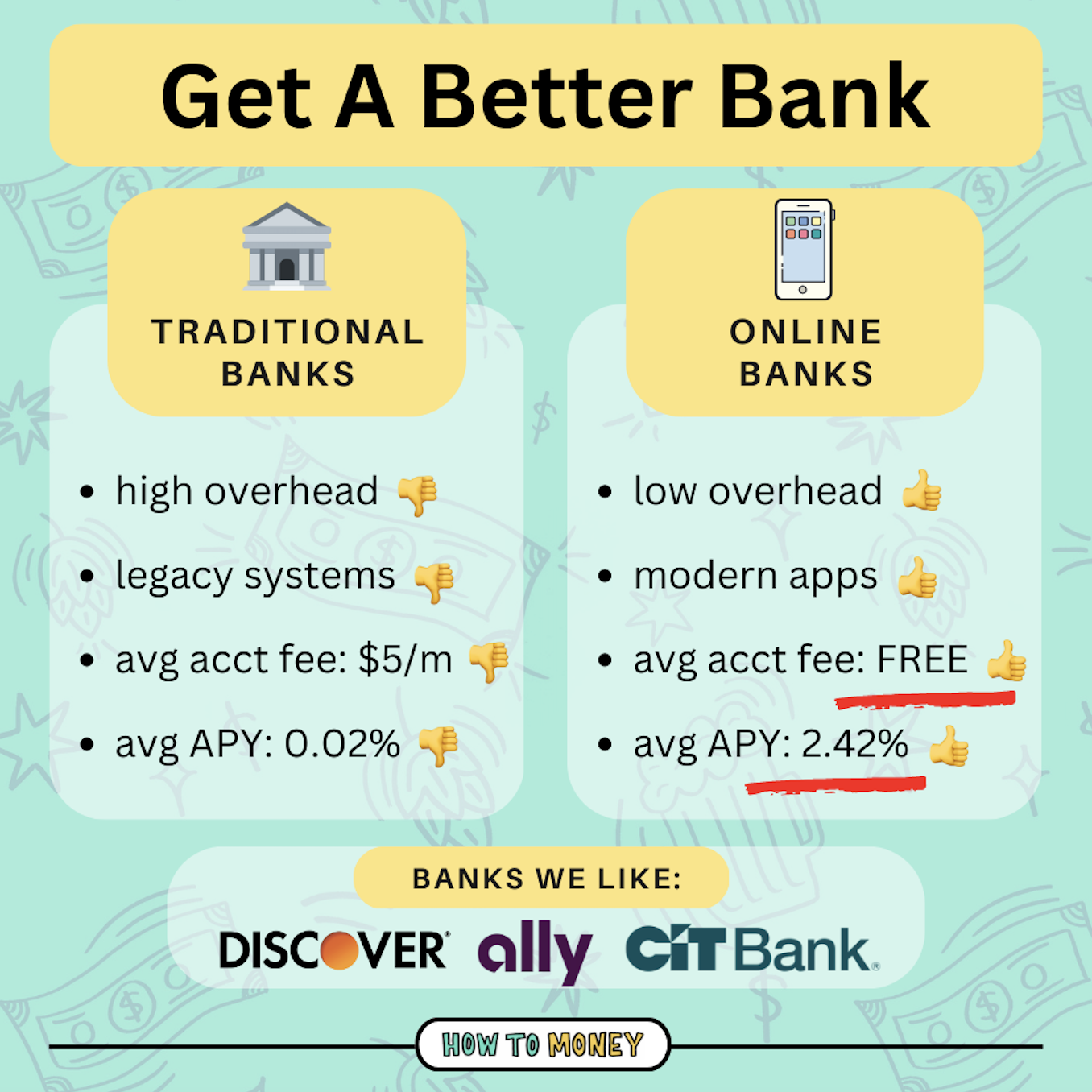

2. Open Up A High Yield Savings Account

The average person has been with their bank for over 14 years. And a lot has changed in that time! So if your bank is still charging you monthly account fees or only giving you pennies of interest each year, it’s time to find a better bank!

We love banks like CIT, Ally, and Discover. Switching to one of these online banks not only avoids all those pesky account fees, they can help you earn a higher interest rate too! The best online banks can be a great place to keep your emergency funds.

Also, moving your money to a HYSA is a great way to stop dipping into your savings account for impulse buys. If the money is out of reach, it’s also out of mind!

3. Consolidate Old Bank Accounts

Speaking of banks, if you have multiple accounts, it’s a good idea to get that money into just a few places. Close any accounts you no longer regularly use, for a cleaner financial profile. The goal is to simplify your money and make it easier to keep tabs on just how much you have in your accounts.

One exception to this is if you use multiple savings accounts to help you better manage your money. For example, if you keep your emergency savings with a separate bank to make it more difficult to access. At the end of the day, use whatever system works best for you!

**Another exception is for any of you big baller shot-callers out there who keep over $250,000 in cash in accounts… Since $250k is the limit to FDIC protection, you might wanna spread funds across multiple banks!**

4. Roll Over Your Old 401(k)

If you’ve switched jobs in the past few years, it’s time to rollover those old contributions to your new employer’s account. Or better yet, roll them over to an IRA, giving you more investment options and control over your account.

Many 401k plans are riddled with fees. The longer you leave your old 401k sitting unattended, the more this impacts your retirement savings.

If you need some help getting the ball rolling, Capitalize is a free tool that can guide you through the process! Here’s a full Capitalize review we wrote discussing their seamless their process.

5. Create A Debt Payoff Plan

Spring is the perfect time to refocus on eliminating any lingering high interest debt from your life. Just making the minimum payments costs you a lot of money over the long run, and can cause your debt to spiral out of control.

The best way to get out of debt is to create a debt payoff plan and stick to it. If you haven’t been making as much progress as you’d like to on that balance, crunch the numbers and try one of these payoff methods. That plan makes all the difference in your ability to rid yourself of that debt once and for all.

Or, if you are absolutely drowning in debt, reach out for help! The two best non-profit credit counseling services are Money Management International and NFCC. Set up a call to see how they can support you and repair your money situation.

6. Organize Your Documents and Passwords

If your desk is buried under mountains of papers from the last few years, now is the time to have a shredding party! Place all of your important documents in one folder and be sure to shred anything else that you don’t need. It’s not a good idea to have sensitive information just laying around, and removing the physical clutter from your home will leave you feeling refreshed.

Scannable is an awesome (and free) app! It helps you take photos/scans of important docs using your cell phone camera. Then you can email them or upload them to your computer for digital storage. Easy!

It’s also a great idea to organize your passwords as well. Now is as good a time as any to change that compromised or overly simple password to something that can’t be easily guessed. This is a great way to keep your finances safe and prevent fraud.

And if you’re looking for a free password manager to help you in that endeavor, Bitwarden is a great open-source option.

7. Sell Your Stuff

Free up space in your home and your mind by selling things from around your house that you no longer use. You’ll feel more focused, and it can bring in some extra cash that will get you closer to your money goals. Craigslist, eBay, and Facebook Marketplace are some of the best platforms for selling your previously loved items.

Going on a selling spree can help you declutter while giving you a nice cash infusion. Use these extra funds to jump start a new savings goal, pay off debt, or even as a way to treat yourself.

8. Revisit Your Goals

Do some deep thinking, alone or with your partner, to make sure that your money goals still align with your biggest hopes and dreams. Have things changed since you last set those goals together? If so, now is as good a time as any to start reformulating.

If you’re pursuing goals you no longer want to achieve, it can lead to lack of motivation. Getting back on the same page can spark your desire to save and invest. Even a small brainstorming session can leave you feeling invigorated and ready to take on the rest of the year in a money-smart manner.

Even the aspirations that still resonate with you could use some small adjustments. Make sure you’re still saving enough to retire comfortably, and that you’re on track to reach your other savings goals.

Here’s a money mission statement guide (including some soul searching questions to ask yourself) that will help you kick off that brainstorming session.

Related: Should I Buy It? (a bunch of self-discovery questions to help determine whether you should buy stuff)

9. Set Up Your Sinking Funds

A sinking fund is money that you set aside each month for upcoming expenses that occur somewhat regularly, but don’t occur on a monthly basis. Think car maintenance, home repair, or even holiday gifts! They’re great because they allow you to save over time. And they help you to avoid taking money out of your emergency fund to cover these expenses.

Take some time to write down what expenses you might expect to incur over the next few months or even years. Then, set up sinking funds to be prepared when the time comes. Your future self will be massively thankful for the preparation you do now! This is an often forgot item on people’s End of Year Financial Checklist!

10. Create A Credit Card Strategy

This one’s a fun one! Credit card rewards are a great way to garner additional savings each month. But you can totally supercharge your rewards with a little bit of planning.

Different cards have unique rewards systems which can benefit you to varying degrees in certain expense categories. Take some time to dig into the benefits of the cards you own. And maybe even label them by what categories you can reap the greatest rewards from while using them. For example, if one of your cards offers 5% cash back on groceries and dining out, actually labeling the card can help you remember to use it when making those purchases.

Now could also be a good time to open a new credit card and snag one of those hefty bonuses. Check out the credit card tool on our website to compare different offers and pick the best credit card for you!

Remember to only do this if you can pay your cards off on time and in full every month. If you’ve struggled with credit cards in the past, feel free to skip this task until you feel ready!

The Bottom Line:

Spring cleaning your finances isn’t just about organizing receipts or trying to spend a bit less each month. It’s about regaining control of your money systems and heading into the rest of the year feeling refreshed about your finances.

Just like a spring breeze revitalizes your home, taking these steps can refresh your outlook on money, empower you to make informed financial decisions, and pave the way for a more prosperous future. So, embrace the spring spirit, roll up your sleeves, and get ready to watch your financial health blossom!

- Top Fugal Living Tips to Cut Down Monthly Expenses

- How to Save Money (in ALL areas of life)

- Tips for More Mindful Spending

**Feature pic by JESHOOTS.COM on Unsplash