If you listened to our interview with Kristy Chen from back in 2019, you may have been shocked to learn that after growing up in China on just 44 cents a day, Kristy moved to Canada, became a millionaire and retired early at just 31 years old. Then, she left her job in engineering to travel the world as a professional writer!

In her book, Quit Like A Millionaire, she writes of her journey to early retirement. “At the end of the day, it isn’t about money, it’s about time- and how to use it wisely to live the best life possible.”

Early retirement is a shortcut you can take to the years where you don’t have to work to cover your living expenses. However, just because you’ll get there more quickly, it doesn’t necessarily mean it’s the best path for everyboth. There’s a LOT of sacrifice involved.

If you feel like how you spend your time doesn’t align with your values, then early retirement could be for you. It can allow you to buy back your time, pursue things you are passionate about, and enjoy increased financial security.

What is Early Retirement?

The formal definition of early retirement is simply retiring from work before the traditional retirement age of 65. It’s when you’ve got enough money saved that you no longer need to work anymore.

When you dig a little deeper though, early retirement is so much more than just stopping work. It’s more about starting “other stuff” earlier in life.

What “other stuff” you may ask? That’s the beauty of financial freedom – spending time doing anything you want!

Retiring early means questioning the traditional path of working 40 hours each week for 40 years. It’s choosing not to put off your dreams until your golden years, and forces you to pay more attention to your values. By retiring early, you can live life on your own terms, spending those valuable hours on the things that bring you true joy.

Sometimes, retiring early is referred to as the acronym “FIRE,” which stands for “Financial Independence Retire Early.” This is a movement that has been picking up steam over the past few decades. If you’re in the personal finance space, chances are you’ve probably already heard of the various types of FIRE.

Can Anyone Retire Early?

There seems to be a persisting stereotype that only high earners, or single and childless folks can achieve early retirement. DINKS, for instance, are prime FIRE candidates. We’re here to tell you that this is entirely not the case. While having a high income (or no kids) can certainly boost your financial abilities, it’s not a prerequisite to retiring early.

Luckily, retiring early can be a possibility for almost everyone. It’s true that it can be more difficult if you are older or if you have a lower income. However, with consistent effort and determination, you can reach financial independence and retire early regardless of your starting point.

Also, keep in mind that with all the benefits of early retirement, there are some potential downsides, too. Early retirement is a noble goal, but it’s certainly not for everyone!

The Benefits of Retiring Early

People within the FIRE community want to retire early for a variety of reasons. Most commonly, people desire more freedom to pursue their hobbies, spend time with friends and family, or to travel. However, retiring early can bring tons of other benefits to your life!

Having More Financial Freedom

When you retire early, you no longer need to work to support yourself. This gives you increased financial freedom and flexibility, allowing you to enjoy your retirement years to the fullest!

In early retirement, you get to spend more of your life deciding how you spend your time. Whether it be with your family, working on a passion project, volunteering or traveling, the world is your oyster. It’s totally your choice!

If you decide you still want to work, you have the freedom to accept a job that isn’t as stable. You can also take a job that pays significantly less because your expenses are already covered. You can work for the pure joy of it.

Less Money Anxiety

When you are financially independent, you’ll likely experience less money anxiety. This is because you’ve already saved up a large nest egg, as well as lowered your expenses. Retiring early requires a lot of forward thinking, and having contingency plans. And with all that thoughtful planning comes substantially less money stress.

When you live well within your means and spend much less than you earn, you’ll likely enjoy more financial stability. Money doesn’t solve every single problem in life, but it certainly helps!

Living Closer to Your Values

When you pursue financial independence, you are forced to think about what you value each day in life. Since your goal is to have more time, it forces you to think about how you’re going to spend it.

When you know your true values in life, it’s much easier to weigh potential purchases against your biggest money goals. You realize that each dollar you have is spring-loaded with potential. Therefore, you will really reconsider the ways in which you choose to spend or save it.

Do you really care about eating out multiple times a week when you’re working towards financial independence? What about that fancy new watch? You get to decide what moves the needle for you and cut back on things that aren’t as important.

Find Joy Outside of Money

By living a frugal lifestyle, you are better able to find joy outside of money. It encourages you to develop frugal hobbies and find cheap ways to have fun with your friends and family. This means you’ll be able to enjoy yourself while on a budget.

Plus, the journey to FIRE can be a great exercise in creativity as you take an unorthodox approach to life’s everyday challenges. When you achieve financial independence early in life, making more money becomes less of a priority. You are forced to find happiness elsewhere!

A Better Sense of Direction

Raise your hand if you felt like you were just floating through space after you graduated from school… 🙋♀️

One of the most exciting things about pursuing early retirement is that it gives you a tangible goal – with a timeline! It’s no secret that we achieve more when we set SMART goals. By joining the FIRE movement you’ll develop a stronger sense of direction, purpose and community!

Enjoy Your Retirement to the Max

Lastly, when you achieve your goal of early retirement, you get to really enjoy it to the max. In addition to enjoying more years of retirement, you’ll be confident that your finances are in check. You’ll know that you won’t have to rely on your kids for fiscal support in the future.

Plus, the earlier you retire, the more likely it is that you will be in good enough health to properly enjoy your favorite activities. Longer and more adventurous vacations, youthful activities with your kids, etc.

The Challenges of Pursuing Early Retirement

Pursuing FIRE may come with loads of benefits, but it does have drawbacks as well. Be sure to look out for these challenges while on the path to early retirement.

It can become an unhealthy obsession…

Real talk here for a second- some people pursuing FIRE elevate it above all other facets of life. They are so focused on the goal that they don’t have time to enjoy the journey.

Early retirees assume that their relationships, health and hobbies will be waiting for them when they cross the early retirement finish line. But the truth is, by prioritizing saving/investing over things like your friends and family, you change as a person over time. Everything that you dropped to pursue FIRE must be re-built on the other side, which can take decades.

Skipping out on every party with friends and family to save a few bucks, seeing your kids less often because you’re working overtime, or neglecting self care/health in the pursuit of saving up a big nest egg has repercussions.

The truth is, none of us are promised to live a long life. You might achieve FIRE only to find that you no longer like who you are as a person. You might spend 10 years breaking your back (literally) and not be healthy enough to do the things you love in early retirement. Or heck, you could kick the bucket the day after you retire and never get to enjoy the fruits of your labor. 💀

Sorry, that got dark for a second! 😅 But it felt worth mentioning.

We’re all for making sacrifices for a brighter future, but you need to have something to retire to. Make sure to maintain your relationships and prioritize some of what you love in the here and now. This is incredibly important if you want to actually enjoy both your life now and early retirement.

You might run out of money

While it’s unlikely, there is a small chance that you could run out of money in retirement. Meaning, you’ll need to return to work. It all comes down to careful forecasting and having back-up options for unplanned plot twists.

One of the biggest risks early retirees face is something called sequence of returns risk. It’s when your investment portfolio performs horribly within the first few years of retirement, and you dig a bigger than expected hole in your nest egg. Rising inflation has been another difficulty that early retirees have had to deal with.

In order to hedge against this risk, it can be a good idea to save up a bit more than you think you will need. Or, have back-up plans of returning to work a few years after you retire if need be. Be sure to also keep up with current technology for your field and to maintain your network to ensure that you’ll actually be able to break back into the workforce should you need to.

Unknown Healthcare costs

With most Americans getting health insurance through their employer, retiring early can pose some issues when it comes to receiving affordable healthcare.

This is one issue that you cannot ignore. The most common reason for personal bankruptcy is medical expenses, so do not skimp on having proper healthcare coverage.

One option would be to factor the cost of private health insurance into your FIRE number (more on this later). However private health insurance can be prohibitively expensive for some folks. One alternative could be turning to the healthcare marketplace and checking if you qualify for federal subsidies based on your income. You could also check out health sharing plans, which function similarly to health insurance, and see if they make sense for you.

Lastly, you could consider going the Barista FIRE route – working a part time job at a company that offers benefits to part time employees, like Starbucks or Costco!

You may need to sacrifice too much…

Pursuing early retirement means sacrificing now to have more later. But if you sacrifice too much of what you love right now, it could drain much of the joy out of life. You need to decide whether you truly want to retire early, or enjoy a more balanced lifestyle right now.

Likely, unless you’re a super high earner and natural frugalite, you will spend at least a decade or more pursuing early retirement. That’s a big chunk of your life! It’s crucial to take the time to think about how you want to look back on these years. It may not be worth it to suffer working a job that makes you miserable and that takes you away from the people you love just to retire a few years early.

However, if you do decide the FIRE movement is for you, you need to prioritize finding balance in the here and now even while you embark on that journey. Think about the kind of life you dream about for retirement and find a few ways to incorporate some of those things on the cheap into your current routine. Basically, don’t put off your idealized life altogether. That’s likely a massive mistake.

Remember, the goal isn’t just to retire as early as possible. If it took you 10 years to retire while working a miserable job or 15 years to retire while working a job you LOVE, we hope you’d choose the 15-year route. Sacrificing too much joy in life just isn’t worth it!

It can be a bit selfish…

Lastly, pursuing FIRE can cause us to place too much emphasis on our own lives. This can lead to neglecting our community, and cause us to forgo generosity in general. Squirreling everything away for our own future can backfire on the giving front!

Most people think “I won’t worry about giving to charity, because I can give more when I’m rich, later!”… But in reality, giving is a lifestyle habit. It’s rarely about the dollar amount, and being charitable enriches your life in hidden ways. You’ll feel more connected to your community and will develop a healthy detachment from your money. Basically, being charitable will prevent us from being visited by the three spirits this holiday season.

Prioritizing your own agenda and setting firm boundaries is necessary for retiring early. But, don’t completely forget the outside world, because we are all interdependent!

How To Retire Early:

Now that you fully understand the benefits and drawbacks of financial freedom early in life, it’s time to talk about the “how.” Fair warning – while the steps to achieve FIRE are actually quite simple, they aren’t always easy.

But like we said before,with consistent action over time, you CAN achieve financial freedom and retire early. Determination is your best friend.

Step 1: Calculate Your “FIRE Number”

The first step in achieving early retirement is to crunch the numbers and figure out just how much money you actually need to retire.

Some good news here… you probably need way less than you think! People have a tendency to grossly overestimate how big their nest egg has to be. The truth is, you don’t need 10’s of millions of dollars to retire early. You only need enough to supply a stream of income that covers your cost of living in retirement.

Begin with the 4% rule

A general rule of thumb is that you need to accumulate 25 times your annual expenses to retire. You can then withdraw 4% of your savings each year of retirement, theoretically never running out of money.

For example, if you expect to spend $50,000 each year in retirement, you’ll want to have $1,250,000 saved up in your retirement accounts to retire comfortably. Under the 4% rule, you’ll be able to withdraw $50,000 in the year you retire, then that same amount (plus inflation) every year after that.

We used $50,000 as an example, but you’ll need to calculate your own estimated cost of living. This is where knowing your true expenses now comes in handy. If you’re not tracking your expenses currently – start ASAP.

Remember, your expenses today will be different in retirement. Some budget items will be cheaper (for example, you could have a paid off house and no mortgage cost later) and some expenses will be more expensive (for example healthcare costs or travel). Do your best to envision the lifestyle you want in retirement to estimate your annual cost of living.

Add some flexibility

You may want to give some additional thought to your FIRE number depending on your personal situation. For example, if you are retiring at age 30 vs. 50, your money will need to last a lot longer. Plus, life changes a lot faster when you’re younger, and your expected spending could ramp up significantly too! So you may want to consider saving up even more of a cushion.

On the flip side, if you’ll have a paid off house and virtually no living expenses in retirement, you may be able to get away with saving a little bit less than 4%.

Make sure to spend some time factoring in the “unknown” expenses, like your healthcare costs or childcare expenses. You’ll also want to think about whether or not social security will still be around by the time you retire. According to Fidelity, the average 65 year old couple can expect to spend $315,000 on healthcare in retirement!

It’s better to overestimate

When in doubt, it’s a good idea to work in some extra cushion to guarantee you won’t run out of money. Hoping for outsized returns or that everything will go your way isn’t a great plan. It’s a good idea to stay open to the idea of picking up extra work in retirement. This can help stretch your nest egg even further should the need arise. That side hustle could be the perfect supplemental income strategy.

For example, let’s say you’ve calculated an initial FIRE number of $1,250,000 (based on the need for $50,000 per year in retirement expenses). But, after thinking further, you may want the option of private health insurance later in life to supplement existing insurance. After accounting for this, you realize that $60,000 per year is a better number to live off of, and therefore require a $1,500,000 nest egg.

By overestimating your FIRE number a little bit, you’ll build in cushion should those additional expenses turn into reality later. If you underestimate your FIRE number, you’ll run the risk of running out of money, which can increase your stress levels dramatically.

Step 2: Start Saving ASAP

Now that you have your goal amount in mind, it’s time to start saving – ASAP! You’ll need to begin socking away a large portion of your monthly income in order to make progress towards early retirement.

Creating a budget is essential to saving enough money for early retirement. By budgeting often and tracking your expenses, you’ll expose all sorts of areas where you can save more money. Eventually the goal is to increase your savings rate by carving out a large portion of your monthly income to go towards investing for your retirement.

Retirement calculators are amazing for forecasting your timeline. You can use an early retirement calculator like this one to see how long it will take you to retire at your current savings rate.

You might realize that even in saving all you can, you’ll still have a loooong road ahead of you. In that case, you will need to make room in your budget for additional savings.

We’ll give you some tips on how to increase your savings and accelerate your progress later on in this post…

Step 3: Invest!

You’ll need to start investing, because it is pretty much impossible to save your way to retirement. Here’s why:

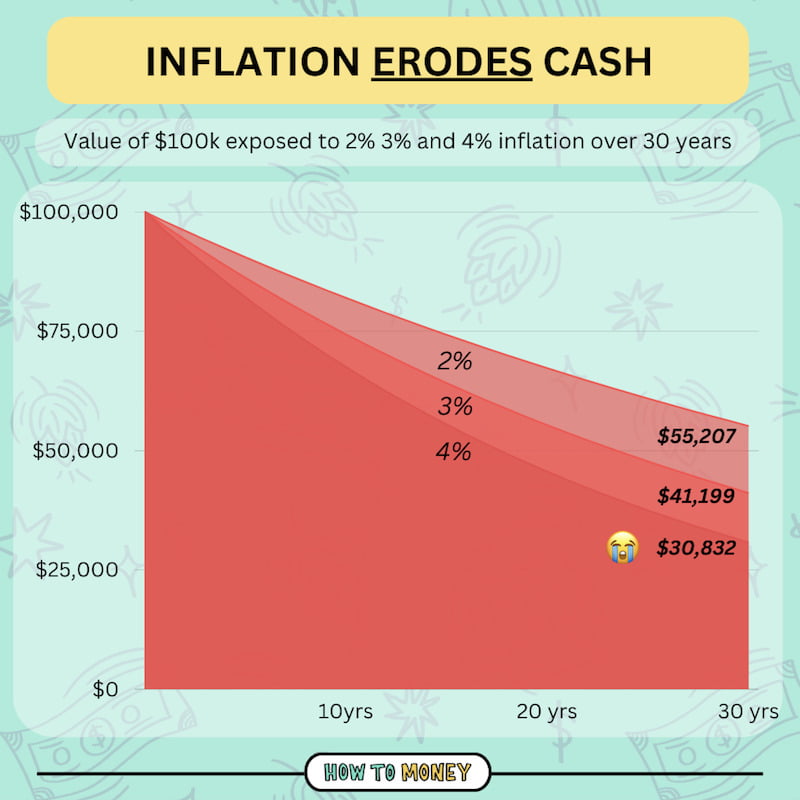

Inflation eats away at your money each year by removing some of its buying power. If you have $100, and inflation rises by 3% that year, your $100 is now worth only $97. Year after year, this has a huge impact on your ability to retire comfortably because compound interest is working against you.

However, when we invest, we put that compound interest to work for us! For example, if you have $100 invested and your money grows by 10%, you’ll have $110 dollars. Even if inflation eats $3 of that, you’ll still have $108 at the end of the year. And when funds are compounded positively year over year, they grow exponentially!

By investing your money and leaving it in your portfolio over time, your money will grow faster and faster the more money you put in and the longer you leave it invested.

Consider Your Risk Tolerance

Part of investing is figuring out your risk tolerance. While this is up for you to decide, as a general rule of thumb, the sooner you are planning on withdrawing your funds, the more conservative your portfolio should be. You’ll likely want a combination of stocks, bonds, and maybe even some real estate.

If you’re hoping to retire in under 10 years, you should keep your portfolio a little more balanced. If your timeline is longer than a decade, you can choose to be a little riskier with your investment strategy.

Now I’m not talking about dumping all of your money into crypto and luxury wines. However, you can afford to put most of your money into highly diversified index funds, and less of your money into bonds or cash.

Here’s a great guide to figuring out your risk tolerance. Remember, if you are young with a 10+ year retirement horizon, you can afford to take on more risk. Not only does your portfolio have the time to recover should a downturn happen, you are also young enough to make changes to your plan and work longer if absolutely necessary.

Where should you invest?

When you’re pursuing early retirement, you have plenty of options as to where you’ll invest your money, each with their own unique benefits.

Start with tax-advantaged accounts

For the best results, you’ll probably want to start out by maxing out your tax-advantaged retirement accounts. Your workplace 401(k), Roth IRA and Traditional IRAs or HSA should be top priority. If you’re self-employed or without employer benefits, you can start by investing in Traditional or Roth IRAs, as well as a Solo 401k or Sep IRA.

Tax-advantaged accounts will provide you with the opportunity to sock away tons of money and simultaneously defer or reduce your tax burden. For example, you can invest up to $50,000 each year within a Sep IRA, or $22,500 in your 401k as it stands.

The biggest benefit to investing in tax-advantaged accounts is that they will lower your tax burden within the year you contribute. You can subtract your contributions from your pre-tax income, effectively making it so that you are taxed on far less of your income. This speeds up your savings and retirement timeline! But it can often mean a bigger tax bill in those retirement years too.

Pro Tip- If you earn too much to directly contribute money to a Roth IRA, be sure to check out our post on the “Backdoor Roth IRA,” which allows high earners to contribute indirectly to this account.

Pre Tax Vs. Post Tax Accounts

When you retire early, you’ll want to have a good balance of money in both pre-tax and post-tax accounts. Having at least some money in the taxable brokerage accounts ensures that you’ll have access to funds before the traditional retirement age so that you can avoid early withdrawal penalties.

With pre-tax advantaged accounts, such as a Traditional IRA or your traditional workplace 401(k), your money is invested before you pay taxes on it. Meaning, if you’ll lower your tax liability for the year in which you transfer these funds.

For example, if you make $100,000 each year and invest $20,000 into your workplace 401(k), you’ll only pay income tax on $80,000.

Keep in mind, you’ll still need to pay taxes eventually. But by deferring taxes in higher income years, you can withdraw (or convert!) money in lower income years to pay less taxes overall.

With post-tax advantaged accounts, you pay tax on that money now, but you can withdraw it tax free in retirement. Our favorite example of this type of account is a Roth IRA.

So, if you make $100,000 and max out your Roth IRA by contributing $6,500, you’ll still pay income tax on $100,000. However, you won’t have to pay anything when you withdraw those funds during retirement.

What about real estate?

A great alternative to early retirement through investing in the stock market is investing in real estate.

As opposed to saving up a large nest egg through investments, like Kristy Shen who we talked about in the beginning, real estate investing allows you to live off of the rent paid by tenants from your rental properties.

Chad Carson, author of “The Small and Mighty Real Estate Investor” discusses one of the major benefits of real estate investing as opposed to index fund investing in this interview. He summarizes, “It’s recurring income- it’s a lot like your salary…you’re used to having that recurring salary and it’s a nice thing to have. Real estate can replace that.”

Sounds nice, right? Having enough rental properties to provide you with regular income… However, be prepared to put in the work! Real estate investing can take a lot of time and energy, especially in the beginning. It also has elements of a part-time job. You can eventually streamline your real estate endeavors down the line, but it’s never really 100% passive.

Pro tip: Why not consider house hacking by renting out a spare room or unit in your home to test it out? It’s a way to dip your toes into real estate investing without going all-in, fully committing to buying a property, finding tenants, the whole nine yards.

Consider a healthy mix of different investment types

You’ve probably noticed that each type of investment vehicle has its unique advantages and disadvantages. And that’s why we recommend a blended approach. Doing this will give you the ultimate flexibility in early retirement.

If you favor one type of investment vehicle too much, you may paint yourself into a corner and have to backtrack later. For example, if you favor your 401k and traditional IRA too much, you may not be able to access those funds easily in early retirement. Both 401ks and IRAs have early withdrawal penalties for pulling out money before age 59 ½.

But if you have a mix of pre-tax and post tax accounts, and maybe even a little bit of real estate, there are more flexible withdrawal options in retirement.

When planning your ideal portfolio, try to “begin with the end in mind.” How do you envision withdrawing funds from your nest egg later in life?

Step 4: Increase your savings rate

Next, it’s time to think through how you can increase your savings rate! Doing this will help you to reach your goal of early retirement much more quickly.

There are two ways to increase the gap between your income and spending. The first is to cut expenses more, and the second is to make more money. To help you achieve that goal of retiring early, we recommend doing BOTH!!

Lowering your living expenses can have a “double whammy” effect on your retirement timeline. Not only will you save more money, you’ll actually need less money in retirement to support your lifestyle.

Lower Your Expenses

While cutting small expenses like expensive lattes, canceling subscriptions, and negotiating your bills can have a massive impact on lowering your expenses, we want to encourage you to consider taking another look at the big ticket items as well. If you want to retire at an early age, big and small expenses alike need to be put on the chopping block.

Ask yourself if there is any way to cut your big three budget categories- housing, transportation and food. Could you drop down to one car for your family, or live entirely car free? Could you rent out a spare bedroom in your home, or even downsize to a smaller house or apartment? Can you cook at home exclusively with the exception of special occasions?

Taking another look at your biggest expenses and adopting more frugal values can help to seriously accelerate your FIRE progress. 🏃♂️⚡️ Here are some related posts you can check out:

- Ways to lower your car expenses (so you can invest all that money instead!)

- How to start house hacking (use your house like a rental propety)

- Tips to slash your grocery bills

Increase Your Income

Another way to drive up your savings rate is to increase your income. Doing so can provide you with more margin in your life, allowing you to save and invest even more.

Make a plan to start earning more. Whether you decide to switch jobs fields entirely, or ask for a raise at work, increasing your salary can have a massive impact on how quickly you are able to retire.

If you feel like you’ve hit a ceiling in your current position, ask yourself if you could earn more by pivoting job fields, or by increasing your skill set through higher education or additional certifications. Leave no stone unturned!

You can also earn more on the side by creating a side hustle you enjoy. Whether it’s walking dogs in your neighborhood or opening an etsy shop, turning your extra time into cash can also help you to move further along your path to financial independence. Plus, if you grow your side hustle enough you could potentially transition to doing it full time.

Bonus- “15 Side Hustles for Couples- Earn Cash, Together!”

Utilize credit card rewards!

In the FIRE community, it’s common to use credit card rewards to travel on the cheap. Taking advantage of large sign-up bonuses can help you to see the world while still prioritizing your nest egg.

We’ve created a credit card tool to help you compare different credit sign-up offers. When credit is managed responsibly, these bonuses can help you make that family trip a reality, even on a budget. Every little bit you save counts towards hitting your FIRE number!

Here are some of our fav cards for big welcome bonuses:

Avoid Lifestyle Creep

As we earn more, our expenses tend to grow in tandem. This is referred to as lifestyle creep. It’s important to be aware of this, and attempt to keep your living expenses about the same even as you make more money.

The most financially successful people are pros at this. For example, most millionaires drive normal used cars as opposed to luxury vehicles. In fact, you could be living next door to a millionaire and not even know it, because they live well below their means. Aiming for stealth wealth is the goal. It’s a sure fire way to ensure that you won’t lose progress towards your goals by trying to keep up with the Joneses.

Take advantage of Catch-Up Contributions

If you are over the age of 50 but still aim to retire early, you have an even greater opportunity to sack away large amounts of money. This is thanks to something called “catch-up contributions.” You can contribute an extra $7,500 to your 401(k) each year, which can increase your portfolio greatly by the time of retirement.

Eliminate Debt From Your Life

Lastly, you’ll want to work towards eliminating debt from your life, especially high interest rate debt. Being in debt while trying to grow investments is like competing in a triathlon with an anchor strapped to your shoes. That debt is working against you.

“Bad Debt,” like credit card debt with high interest rates or payday loans, is especially harmful to your early retirement goals. It puts compound interest to work against you, causing your debt to skyrocket quickly. If you have any lingering high interest rate debt, it’s important that you work hard to erase it from your life by creating a debt payoff plan and sticking to it.

If you have “good debt,” or lower interest rate debt on an appreciating asset like your home or education, it’s okay to hold off on paying this off until later into your financial journey when you reach Money Gear 6.

Step 5: Plan your withdrawal strategy

We touched on this earlier – withdrawing your funds in early retirement can be tricky, so it’s important that you plan your withdrawal strategy well in advance. Essentially, you need to begin your early retirement journey with the end in mind.

The complication stems from the fact that you typically need to be 59 ½ to withdraw money from your retirement account without penalty (I love the validity this adds to half birthdays! 💁♀️). So how can you access these funds to live off of during your early retirement?

Believe it or not, there are ways around this rule. They can be a little bit confusing, so you’ll likely want to work with a tax professional before attempting this on your own.

To withdraw your funds early, you can use the Roth conversion ladder. Or the 72-T Rule, outlined here in this post from the Mad Fientist.

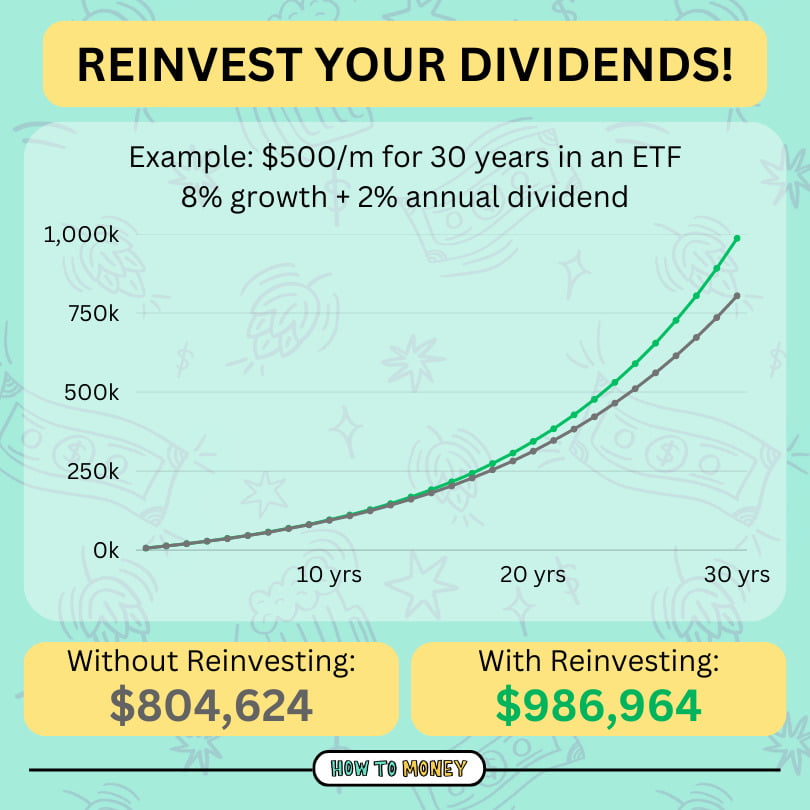

In addition to selling investments, you’ll also be able to take advantage of dividends from your stock and bond portfolio. When you purchase stocks, you’ll be paid a portion of corporate profits from the company, or companies within your index funds.

As the money in your portfolio grows, those dividends can become significant. However make sure that before you reach retirement, you opt to have those dividends reinvested.

If you’ve decided to house hack, or purchase a rental property, you can also use the rental income to live off of in retirement. This can be especially effective if you’ve paid off the mortgages on your rental property.

Lastly, if you are planning on pulling funds from a brokerage account, make sure you plan for capital gains tax. When you sell your investments for a profit, the IRS sees it as income, and you’ll pay taxes on it, so plan ahead before you make any withdrawals.

Tips for Success

As you can see, you can follow some pretty concrete steps to achieve early retirement. However, how you get there will be different for everyone, and it won’t necessarily be simple. You could spend decades of your life pursuing early retirement, so you’ll want to look back on these years fondly. Here are a few tips to better enjoy the FIRE journey.

Enjoy the Gamification

You’ll need to stay excited about your goals if you want to retire early. One way to do this is by adding gamification elements. Brainstorm a few ways to make your finances more “game-like”, including challenges and rewards.

For example, get a friend involved and competing with them to see who can cut their spending the most. Or treat yourself (without breaking the bank) when you reach certain milestones.

Don’t Neglect Emergency Savings

When you’re laser focused on achieving FIRE, it can be easy to funnel all of your extra cash into investments. But, it’s important to make sure you have a fully funded emergency fund, set aside in liquid savings. Having some cash on hand, between 3-6 months of living expenses, ensures that you won’t need to sell your investments at a loss should you come upon financial hardship.

Rethink Happiness

When you’re pursuing FIRE, you’ll likely need to say no to some things you might want to do. Retiring early requires making big sacrifices. It’s only natural that you might occasionally feel a little bit of FOMO or disappointment. That’s why it’s important to clearly identify what actually makes you happy.

If you’re seeing pictures of perfect homes or luxurious travels on the internet, it’s important to remember that when you scroll on social media, you’re seeing a highlight reel of someone else’s life. Their escapades could very well be funded by debt! Or they may have other aspects of their life they choose not to share online. At the end of the day, you’re only getting part of the story.

If you’re starting to feel a little bit of fomo coming on, ask yourself- would you rather have an instagrammable life, or the freedom to spend the majority of your time doing things that you truly value?

You might realize that many of the most satisfying things in life are free! Whereas spending outside of your means or on things you don’t value only leaves you with more anxiety.

Another thought — might also realize that taking a year off work is enough time to “reset”, and then pursue a new career path. Working might still be a great option for you afterall.

Choose the Best Form of FIRE for YOU

It’s also super important to think through what lifestyle you want in retirement. Do you plan to continue your frugal lifestyle after you leave work, or do you want to live large in retirement?

Did you know that there are different types of FIRE that you can pursue based off of your desired post retirement lifestyle?! For example, Lean FIRE focuses on keeping your expenses super low, allowing you to retire with less money saved. Whereas Fat FIRE focuses on retiring with more money invested, allowing for a more lavish lifestyle!

There are many ways to pursue financial independence. Choose the one that’s right for you, not just what everyone else is doing.

Use the Money Gears for Direction

If you still need a little more direction for where to start, use the money gears to better understand where you are in your financial journey. They can give you a sense of direction and milestones to celebrate.

Whether you want to rite early or not, it’s still important to save and invest your money. Eventually you will need to retire and stop working. And by getting your finances under control earlier vs. later, you’ll make it a lot easier on yourself!

Retire To, Not From

Lastly, make sure to spend time working to build a life for yourself as well as building up your finances. The happiest retirees tend to have plenty to look forward to in retirement, not just time spent away from work.

Make sure to take care of your health to the best of your ability while pursuing FIRE, and not to neglect your hobbies and relationships. Otherwise, you may find yourself unhappy and bored with work no longer a part of your life.

If you’re worried about finding purpose and fulfillment in your life after retirement, take the time to plan out what you want your days to look like. Choose a few hobbies you’d like to pursue, pick a charity you would like to volunteer for, or make a travel bucket list. Better yet, pick a passion project of yours that you’ve always wanted to pursue and get to work! That way, when you enter retirement, you’ve already come up with a plan for how you will manage your time.

The Bottom Line:

Early retirement is simple, but it’s not easy. It requires a lot of sacrifice and hard work, but if your priorities are in the right place it can be absolutely worth it.

By following the above steps, you’ll be able to enjoy a comfortable and early retirement, all while maintaining balance in your life and keeping money in its proper place.

Joining online groups and communities of other early retirees can be a great way to learn more. The more people you connect with that are part of the Financial Independence Retire Early movement, the more ideas and inspiration you’ll have for your journey.

Related Posts: