Taking on a small amount of student loan debt can ultimately result in a meaningful payoff for many folks. On average, people who hold a bachelor’s degree earn more than those with only high school diplomas throughout their lifetime. By a long shot.

But borrowing too much can have a negative impact on your finances. Those recurring monthly payments for decades to come can become burdensome. And if you don’t have a plan to pay off your student loans, that debt can “linger” and affect you long into adulthood. So here’s the scoop on how to pay off your student loans (without losing your mind in the process 😉).

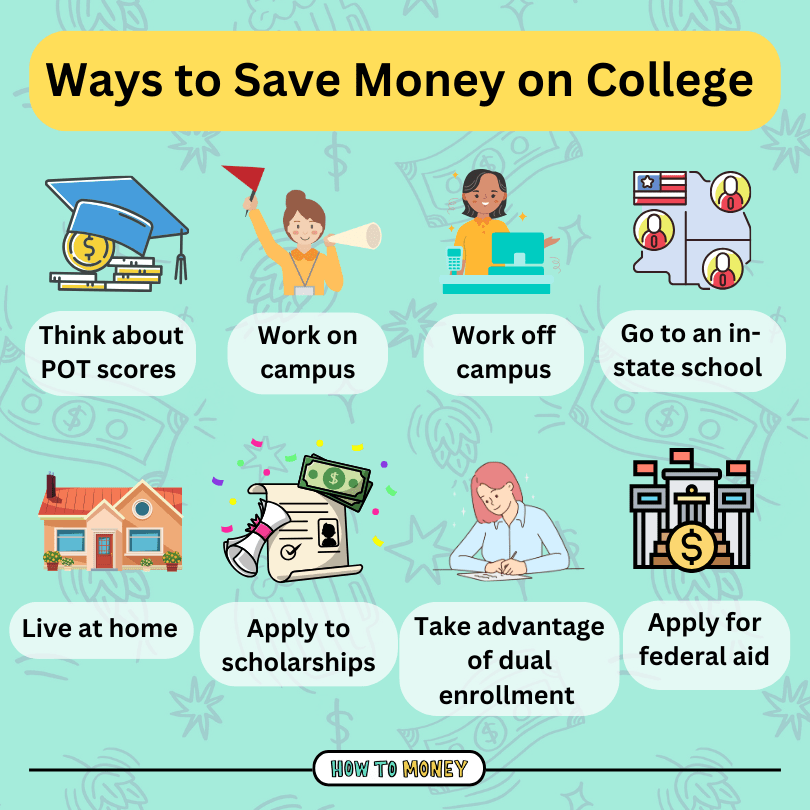

Saving money on college

If you’ve already snagged your degree, you can skip this section because we’re going to be talking about some ways to seriously cut back on the cost of college before you take the plunge. For those still in school, we want to encourage you to avoid taking on student debt as much as possible.

Here are a few tips that we think will help you save a meaningful chunk of money on that college degree!

Not all of these strategies will work for every student or family. But don’t rule them out too fast without giving them the “good ol’ college try.” See what I did there?

They say “the decisions you make in college will affect you for the rest of your life”. And financially speaking, that is entirely true! Being a financially savvy college student puts you miles ahead of those who just opt to go to their favorite school without considering the long-term ramifications of that decision.

Is college even worth it for you?

Firstly, it’s important to ask yourself if college is even the right path for you to take. Do you actually need to seek higher education for your desired career?

The truth is that 32% of college students don’t end up getting the degree they set out to achieve. That means that they are stuck with school debt without the increased earning potential that comes from graduating. Bearing this in mind, whether or not to go to college is a decision that shouldn’t be made lightly. Remember that there are plenty of successful people who did not go to college. It is not your only option when it comes to living a fruitful and purpose driven life.

We’re also not telling you to give up your dream of becoming an engineer to avoid taking out student loans. That would be short-sighted. But if you’re unsure of what you want to do for a career (or alternatively, know exactly what you want to do), it might be worth looking into alternatives, like trade school or community college.There are plenty of high paying career paths that don’t require traditional 4-year degrees.

Maybe you’re a gifted photographer, or have a product you’ve always wanted to create. Maybe you’ve always dreamed of being your own boss. Or maybe you just like using your hands at work. Could entrepreneurship be a better path for you? Consider starting your own business to build the career you want, avoiding unnecessary student loans.

Most young entrepreneurs can start a business with zero dollars and build something great.

Think about POT scores (Pay Over Tuition)

In some cases, it can make sense to take out a larger student loan (although we still advise against it if possible). Take doctors, for example. Medical school costs roughly $218,000 on average. Yup, I typed the correct amount of zeros. 😅

The good news? The average starting salary for a doctor in New York is $252,000 each year. Now you can see why people still pursue this career knowing full well how much money they will need to borrow. The juice is typically worth the squeeze.

However, not all careers are worth taking on massive amounts of debt for. A good way to judge whether or not a college major is worth the money is to calculate your “POT score,” or pay-over-tuition score.

Here’s how to calculate it:

(Median Salary for Career Path – Minimum Wage) % tuition cost

Who said you’ll never need to use PEMDAS in the real world? 😉

Here’s an example: Let’s say you want to get a degree in engineering. The cost of a 4-year in-state college might cost you around $28,280. Since the federal minimum wage is currently $7.25 per hour, working full time for minimum wage would yield you $15,080 per year. The median engineering salary sits around $100,640. Here’s the math:

($100,640 – $15,080) % $28,280 = A POT score of 3.02. Pretty great!

Now imagine you go to a more expensive, private college, bumping your tuition costs to $65,000 over the course of 4 years. It’s going to have a big impact on that POT score.

($100,640 – $15,080) % $65,000 = A POT score of 1.31 Still not terrible, but definitely not as good as before.

Using the pay-over-tuition calculation is a great way to compare schools and degrees against each other. The goal is to figure out how to get the greatest value from your education. Minimizing the cost and maximizing your earning potential is the best recipe for creating that all-important value.

Work on campus

There are so many awesome benefits to working on campus. Not only will it provide you with extra cash to put towards your education- you’ll likely live in a dorm close to where you work which means you can probably just roll out of bed 15 minutes before your shift. In addition to getting valuable work experience, you’ll seriously cut back on transportation time.

Certain campus jobs can even come with special money saving perks. For example, becoming an RA often means having your housing costs completely covered. This can save you thousands of dollars each semester! Working in the dining hall could mean getting a free meal plan, or at least free food during shifts. Some on campus jobs will even offer you tuition waivers! Be sure to contact your school and ask about what work opportunities they offer for students.

Work off campus

Even if you can’t secure one of those coveted on campus jobs, it’s still a good idea to get a job off campus if you can manage to work alongside your studies. Earning money and paying off part of your tuition as you go will help to cut down on the amount you’ll be owing once you graduate. Trust me, future you will be grateful!

Plus, plenty of companies will even pay for some of your tuition. Big companies like Target, Starbucks and Chipotle offer this as a job benefit, even for part time workers. Again, you’ll also gain valuable work experience that will put you ahead of your peers come graduation.

Go to an In-State College

When trying to cut back on college costs, it’s important to choose a school you can afford. Opting to attend a state university can save you tens of thousands of dollars over the course of a 4-year degree.

The difference in cost between state schools and private schools can be huge. For example, state tuition in New York is just $7,070 per year, versus the average private school tuition being around $43,000 in the New York area. That’s a massive discrepancy!

The reality is that certain state universities can be just as prestigious as private schools, and offer similar amenities at a significantly lower price! Yes, sometimes fancy private college connections can get you ahead in certain conversations. But it’s an expensive perk with not a lot of certainty!

Commute to School

If your school is under an hour away, you might want to consider commuting for some years of college as opposed to living on campus all four years.

You can expect to pay around $12-15,000 each year in room and board. This means shelling out around $60,000 over the course of four years. Consider if that money was invested instead. That $60,000 could become $129,000 over the course of a decade. Or that $60,000 could be set aside as a down payment for a house. That’s not chump change!

Certain folks might also prefer commuting to college as well. Sure, it might not be as convenient. But you won’t have to share your room with a stinky roommate who snores at a volume of 103 decibels. Plus, you’ll get to cook meals in a legit kitchen instead of eating that institutional meal plan food. You can enjoy more privacy, and the savings will often make this a worthy choice if you’re not too far away.

Apply to Scholarships

Applying for scholarships can feel like a daunting and tedious process, but it is one of the best ways to reduce your student debt burden.

If you are in high school, ask your student counselor if there are any scholarships you can apply for through your school. This is going to be your best bet at earning some extra cash for college. Your guidance counselors are there for a reason. Utilize them!

You can also call your college and ask them if they offer any academic or talent based scholarships you can apply for. Most of the time, these scholarships and their applications can even be found on the college website.

Remember that even smaller scholarships, like $500 ones, are offering real money that will make a difference. Think about it, if you take 2 hours to apply for a scholarship and you actually get it, you just got paid $250 per hour of work. Not bad, right!?

You can also reach out to local organizations in your town like cultural institutions, local theaters, and sports organizations to inquire about whether or not they offer any scholarships for graduating high school seniors.

Dual Enrollment/AP Classes

Did you know that there’s a way to start college with tens of college credits, saving you time and money? Many high schools offer dual enrollment and AP courses, which can allow you to earn college credits while still in high school.

Dual enrollment courses partner with accredited colleges and offer you a steeply discounted rate for real college credits. AP courses are free to take, and depending on your score on the AP exam (which does cost a little bit of money), many colleges will accept the class and give you college credit. If you earn between 12-16 credits while still in high school, you’ll have the potential to graduate a semester early!

Apply for Federal Aid

Lastly, make sure to apply for federal aid every year of college by filling out the FAFSA. Even if you don’t think you will qualify, still make sure you submit that application. If you don’t, you could be leaving money on the table. You might earn too much to qualify for federal student aid. But if you don’t fill out the FAFSA, you’ll likely miss out on other merit-based financial aid opportunities too.

Don’t forget to apply as soon as that bad boy opens up each year. The FAFSA is first come first serve, so you’ll have a better chance of getting a more significant aid offering the earlier you apply.

How to Pay Off Your Student Loans

So you’ve just graduated, and now the clock is ticking until your lender demands you start coughing up those dollars you borrowed. What now?

Well first of all, congratulations on earning your degree! It is no simple feat, and you deserve to celebrate that accomplishment. Might I suggest treating yourself (just a little) to celebrate?

At the same time, after you’ve recovered from weeks of finals, it’s a good idea to come up with a plan for how you’re going to start paying back that money you borrowed. Luckily, we’ve got you covered. Here is a step by step guide on how to manage paying off your student loans.

Step 1: Pick Your Repayment Plan

One of the most crucial steps in paying off your student loans is picking the right repayment plan for your personal situation. This will affect your payment amount, timeline, and whether or not you’ll receive any student loan forgiveness.

It’s worth noting that the following payment plans only apply to federal student loans. We’ll talk about private loans a little later.

Paying Back Federal Student Loans

For federal student loans, you have a few different options when it comes to payment plans. Picking the right plan for you can help you to better manage paying off your student loans according to your goals.

In general, you can choose between two main types of repayment plans: fixed payment plans and income driven repayment plans.

Fixed plans are set on a 10 (or 25) year timeline, and each month, your payment will be determined ahead of time to ensure your loans are eliminated at the end of that set period of months.

Income driven repayment plans are based on a certain percentage of your income, and will fluctuate over time as your income changes. It also means that you will likely pay them off over a longer time period (20-25 years). However, at the end of that agreed upon time period, any remaining balance will be forgiven.

Standard

The standard repayment plan is a fixed payment plan. For standard repayment, your loans are broken down into an amount that will ensure your loans are paid off within 10 years. This is the best repayment plan if you are not concerned about reducing your monthly payment and want to pay the least amount of interest overall.

Graduated

Similar to the standard repayment plan, this repayment plan is also a fixed payment plan set up to ensure that your loans will be paid off within 10 years. However with this plan, your payments start out low and increase every two years. This plan assumes that as you continue your career, you’ll make more money. However, it’s important to remember that this isn’t always a guarantee.

Extended Plan

To qualify for the extended plan, your loans need to total more than $30,000. This plan is a fixed payment plan which extends your repayment timeline to 25 years. The extended plan contains its own versions of the standard and graduated payment plans.

Save Plan (IDR)

So you want to get your monthly payment as low as possible and receive maximum loan forgiveness? In walks the SAVE plan, or “saving on valuable education” plan.

This new income driven repayment plan sets your monthly payment at 10% of your discretionary income. In July 2024, that payment amount will drop to just 5% of your discretionary income. If you make less than $32,800 (or $67,500 for a family of 4), your payment could even be $0 each month. Not too shabby!

This plan lasts 20 years for undergraduate loans and 25 years for graduate loans. At the end of the payment term, any remaining balance is forgiven. However, if your principal loan balance is $12,000 or less, you could see forgiveness in as little as 10 years. For each additional $1,000 you borrowed, you’ll keep paying for another year. For example, if you borrowed $11,000 you’ll see forgiveness in 11 years.

Perhaps one of the coolest parts of this new IDR plan is that any unpaid monthly interest will be eliminated. That means if your payment doesn’t cover the loan interest, as long as you make on-time payments, even if they don’t cover your loan interest, your loan balance will never grow as long as you continue to make on time payments.

Plus, your payments will likely be lower than they would be under previous IDR plans because the payment is now based on the difference between your adjusted gross income (AGI) and 225% of the poverty level. Former IDR plans based your payment as income minus 150% of the poverty line.

If you were previously enrolled in the REPAYE plan, you’ve been rolled into this plan and will receive the same benefits. If not, you can apply for the SAVE program here.

All in all, if your goal is to have the lowest possible payment, this repayment option is a solid plan for many people.

The PAYE Plan (Pay As You Earn) and ICR (Income-Contingent Repayment)

With the addition of the SAVE program, the Pay As You Earn and Income-Contingent Repayment plans will be eliminated. If you are already on one of these programs, you are able to stay on them. However, should you switch your plan after July 1, 2024, you won’t be able to get back on the plan. Similarly to SAVE, these programs limit your monthly payments to between 10-20% of your discretionary income without the added benefits of SAVE, like the subsidized interest.

Public Service Loan Forgiveness (PSLF)

If you work in public service, or plan to work for the government or a qualifying non-profit in the future, it’s important to get well acquainted with public service loan forgiveness, or PSLF.

This program allows your loans to be forgiven after just ten years of working full time for the government or qualifying non-profit employer. The good news is that your specific job type doesn’t matter, so long as your employer qualifies.

Search for your employer here. If they are listed as PSLF eligible, you may qualify for forgiveness!!!

After making qualified payments on your payment plan, your remaining loans will be forgiven in full at the end of that ten year period. This is not a payment plan in and of itself, but a program that multiple repayment plans qualify for.

So, if you want to see the greatest benefit and are confident that you will spend at least 10 years working for a qualifying employer, you’ll likely want to take advantage of one of the income driven repayment plans, as you could see the highest amount of loan forgiveness here.

Should you refinance federal student loans?

If you have federal student loans, chances are you’ve gotten one of those offers in the mail trying to get you to refinance your loans with a private lender. Refinancing is when you get a new loan from a different lender to pay off your current lenders, oftentimes securing a lower interest rate in the process.

While you may be able to get a lower interest rate or lower your monthly payment, it’s important that you think twice (maybe even three times) before refinancing with a private lender.

Refinancing is FINAL and there is no turning back. While it may work for some folks, in most situations it probably isn’t going to be the best move if you have federal student loans. Lower interest rates are great, but you’ll give up all of the benefits of federal student loans without the option to ever get those perks back.

For example, should your income change, you won’t be able to apply for an income driven repayment plan. You give up all options for loan forgiveness, and for deferral and forbearance should you be unable to make payments. Even the way unpaid interest is capitalized is different, with a significant benefit for those with federal student loans.

If you have a very small amount of student loan debt and are planning on paying it down as fast as possible, a refinance could make sense. A lower interest rate could allow you to tackle those loans over a shorter time period. However, don’t make the decision lightly.

Related: Check out this post for more guidance on whether or not student loan refinancing could make sense for you.

Repaying Private Student Loans

When it comes to repaying your private student loans, you’ll need to make payments according to the agreement you signed when you took out your loans. Meaning, you won’t be given the option to select a repayment plan post graduation. However, if you are unable to make payments, most loan servicers will work with you to try and keep you from defaulting on your loans.

Unfortunately, private student loans leave you with very few repayment options, which is why we typically advise against taking them out if you can avoid it. If you want a different repayment plan, your best bet will be to shop around for a refinance. Try using a website like Credible or Splash Financial to compare rates from different lenders. Sometimes, you can even snag a bonus from your new lender to sweeten the deal.

Step 2: Find your loan servicer

Once you’ve decided which repayment option is best for your unique situation, it’s time to figure out just who the heck your loan servicer is. If your loans were paused during the pandemic, you probably received countless update emails as your loans changed hands multiple times. Don’t worry though, there is an easy way to find out where your loans are.

Simply log on to Studentaid.gov, head to your dashboard, and scroll down to where it says “my loan servicers” on the right hand side. It should contain a link that will take you to your loan servicer’s website.

If you would like to apply for one of the “fixed repayment” rate plans other than standard repayment, you’ll need to call your servicer and ask them to sign you up for one of these. However, if you want to apply for the new SAVE program, you can do so here.

Now that you’ve found your loan servicer’s website, this is the interface you will use to make your payments. Once you access your account and are enrolled in your payment plan, you’ll be able to see how much you owe, as well as what your monthly payment will be.

Step 3: Make Room in Your Budget to Pay Off Student Loans

Now that you know what your payment will be, it’s time to find the room to make payments within your budget. If you haven’t created a budget yet, make sure to check out this mega post on budgeting for beginners. This will walk you through the entire process of creating a budget that aligns with your values and goals.

If you’ve already created a budget, you’ll need to find money in your current budget to cover this new expense. Seeing that the average student loan payment is $503 each month, here are a few ideas on how to find that money within your budget!

- The average American spends $273 each month on subscriptions! Could you pare it down to just 1 or 2 at a time? Savings ~$223/month

- Choose a few bills to negotiate this month. For example, switching your phone bill from one of the big providers to one of these cheap phone plans can save you around $40 each month!

- This one hurts me as much as it hurts you… The average person spends about $300 each month just on dining out! Can you get more creative cooking at home and cut this in half? Savings ~$150/month

- Can you pay off a lingering credit card debt? That could free up some extra money to put towards your student loan each month. Savings ~ $100/month

Total budget savings: $513

Alternatively, you could work towards increasing your income to accommodate this new line item in your budget. Consider asking for a raise at work, or starting a side hustle to bring in a few hundred extra dollars each month.

Step 4: Set Up Autopay

Next, it could be a good idea to automate your student loan payments. This will ensure you never miss a payment or are late. It also gives you peace of mind because it’s one less thing to worry about forgetting each month.

Since your payment will likely stay the same for long periods of time, it doesn’t pose the same danger of encouraging an “out of sight, out of mind” spending mindset. Debt payments and retirement savings are best done on auto-pilot.

Just remember to always make sure your checking account has enough cash to handle the payment to avoid those pesky overdraft fees. Or missing a payment because of insufficient funds.

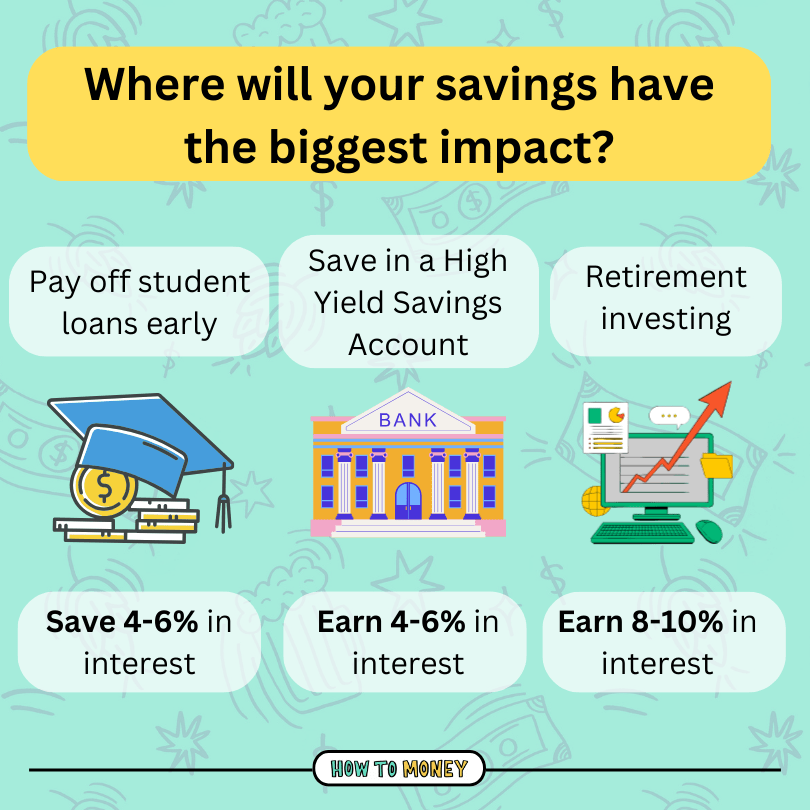

Should You Pay Off Your Student Loans Early?

If you hate your student loan debt (and why wouldn’t you), you might be wondering if it’s a good idea to pay them off as fast as possible. Well, hold your horses. The answer is “maybe.”

This really depends on your interest rate and your personal comfort with debt. To understand the nuance, we need to talk about good debt vs. bad debt.

Typically, good debt carries lower interest rates and is tied to something that appreciates in value. For example, a mortgage. However, just how good they are heavily depends on your major and career path. Taking out a crushing amount of student debt to go into a lower paying career field often won’t leave you with the same returns as going into something typically lucrative like STEM (no shame- this is coming from a music major!).

On the other hand, bad debt carries high interest rates and is usually taken out to pay for depreciating assets, like consumer goods. Examples of bad debt include credit card debt, personal loans, and payday loans.

If your student loan has a lower interest rate, below 6 or 7%, you may not need to rush to pay it off early. For example, if your interest rate is in the 4% range, you could put your money into a high yield savings account and earn the same amount of interest, if not more!

Effectively, you’re counteracting bad interest with good interest. Plus, if you invested it into the stock market, you could earn even more over the years. If you’re a total math nerd, you might find that by paying off your student loan debt early, you’re actually in a position to miss out on the ability to earn more (and save on taxes) through investing.

However, if having this debt hanging over your head causes you stress and anxiety, it could make sense for you to pay it off early. Yep, even if it’s not the most mathematically beneficial route to take. You can’t put a price on peace of mind! Just make sure you are investing enough for retirement before redirecting your efforts to those pesky student loans.

Methods to pay off student loans early:

If you’ve decided that you want to pay off your student loans early, there are plenty of strategies you can use to cut them down to size in a relatively short amount of time. Here are just a few ways to funnel more cash towards those loans.

Make Extra Payments

For the “extra payment method,” switch to making bi-weekly payments as opposed to monthly. Just take your monthly payment amount and divide it by two, then pay that every two weeks. For example, instead of paying $500 once a month, you’ll pay $250 every two weeks.

Here’s the beauty in bi-weekly payments… Because every month has 4.5 weeks (not just 4), you’ll end up making two extra half payments a year. This amounts to one extra full payment against your loan principal. This can make a serious difference in your payment timeline.

For example, if you had $15,000 worth of student loan debt borrowed at 5%, and your monthly payment was $159, making just one extra payment a year (amounting to just an average of $13 more each month) will shave an entire year off of your student loan repayment period. Meaning, you’ll crush those loans in just 9 years instead of 10.

Find a Job that Pays Towards Student Loans

The ultimate life hack is paying off your student loans early… not with your own money, but with that of your employer!

Did you know that certain companies will pay money towards your student loans? Employers like Staples, LiveNation, Penguin Random House and many more offer this incredibly helpful benefit. So don’t forget to think about secondary benefits, beyond just the starting salary, when you’re looking for work.

If you want to make the greatest progress towards paying off those student loans, continue to make your usual payments while your employer contributes additional cash as well.

Use Your Tax Returns (or any Bonus Money)

Okay, so I know that when you get that tax return in the spring it feels like free money. Which means it can be extra tempting to blow it in classic “treat yo self” style at the mall or at your favorite restaurant. But I think people really underestimate just how big of an impact this money can have on your life when you use it to improve your finances.

Say you snag a $2,000 tax return, or a bonus from work every year in December. You could pay off $20,000 in student debt in just 5 years, as opposed to 10 if you funnel it towards your debt instead of juicing your spending.

If you want to pay off your student loans early, any time you get “surprise money,” like a bonus or a tax return, put it towards your student loans and watch years of repayment melt away before your very eyes.

Make larger payments

Lastly, the simplest method to pay off your student loans more quickly is to just make larger monthly payments. Even as little as an extra $50 each month could shave years off your repayment timeline.

Sticking with our example from before, if you wanted to pay off $20,000 of student loans at 6%, your monthly payment would be $212 over the course of 10 years. By paying just $50 more each month, you’ll shave off a little over two years of repayment and save $1,336 in interest.

What should you do if you can’t repay?

Sometimes, financial disasters may strike. You might be smacked with unexpected medical bills, or get laid off. Or maybe you’ve only graduated a few months ago and you aren’t making as much money as you expected. It happens to the best of us, and in some circumstances you may find yourself unable to pay your student loan.

If this is the case, be sure to call your student loan service provider and let them know ASAP. Never run away from your debt obligations – confront them head on.

Private or federal, lenders should work to help you avoid defaulting on your loans. If you have federal student loans, they may be able to provide you with deferment or forbearance, which will allow you to stop making payments for a predetermined amount of time. Private lenders may be able to temporarily lower your payments to something manageable for you given your current situation.

Once you strike up a deal with your provider, it’s time to work like heck to find the money for that monthly student loan payment. Whether that means applying to more lucrative jobs like crazy, getting your side hustle up and running, or working to slash other expenses from your life, it’s time to get to it. Forbearance only lasts a few months, and defaulting on your loans can have disastrous consequences on your life and credit. They can even garnish your wages and withhold your tax returns, so seriously- you need to avoid this at all costs.

The Bottom Line:

Nobody loves paying off their student loans, and sometimes you really do wish you could time travel and shake some sense into your teenage self. But at the end of the day, you can’t change the past. Avoiding or postponing tackling your student debt will only hurt your finances. It’s important to be proactive when it comes to managing your student loans to protect your financial wellbeing.

Hopefully this post has cleared up some of the acronym confusion, and has made your student loans a little easier to understand. With time and effort, you’ll watch those loans diminish over time as you move further along your path to financial independence.

Related Posts: