Making a budget is easy, but fixing a failing budget can be another story! There are a ton of reasons why we may have trouble sticking to our budgets — incorrect forecasting, constant overspending, or a lack of discipline to stick to it.

But even if you have a disaster of a budget, it’s super important to keep trying to find a system that works for you. Mastering this all-important financial task can truly turn your life around!

So let’s talk about ways to course correct a failing budget. Not everyone budgets the same, so we’ll cover an array of ideas that you can try and see what works best for you.

1. Identify the problem spots

First, take a quick moment to look in the rear view mirror and reflect on why your previous budget failed in the first place.

It may be painful to think about, but identifying those weak spots can quickly reveal where you need to focus your fixing efforts.

It helps to dig deep, asking yourself “why” multiple times to reveal the true root cause. You might find different issues from what you originally thought.

For example:

Why did my budget fail? → I accidentally overspent on fast food last month.

Why did I accidentally overspend? → I didn’t keep track of my receipts and forgot how much I had already spent eating out.

Why didn’t I keep and track my receipts? → It’s just too time consuming and manual.

In the case above, “overspending” might not be the root cause issue for the budget not working. It’s more about organization and doing the manual tasks well OR finding an automated system that actually works for you.

2. Get help with an app like YNAB

You Need A Budget is a digital budgeting app that helps track your expenses and meet savings goals by assigning every dollar “a job.” It’s hard to screw up because the app does most of the work for you!

YNAB has an annual fee — it’s $99 per year (or free for students). But, before you rule this option out, listen to this stat… The average YNAB user saves over $6,000 within the first year of using the software! That’s not chump change. YNAB has an extremely loyal customer base and endless support materials from the community. It’s hard to go wrong with this software.

So if you’ve tried manual budgeting and need to bring in the help of a heavy hitter to save time and automate tracking, YNAB is for you. They also have a free 34-day trial, so there’s not much downside to at least trying it!

3. Fix overspending problems

Overspending is kind of like showing up late to work. It’s OK if it happens once in a while when you’re having an off day, but if it’s a regular routine, it really starts to impact your overall performance and success.

Here are a few ways to help correct overspending:

Use cash instead of credit cards

The best thing about using physical cash to pay for things is that you can’t spend what you physically don’t have. Envelope budgeting a.k.a. “cash stuffing” is making a huge comeback with younger generations for just this reason. It really works!

Sure, it’s not the most convenient system. And you might not want to be carrying huge wads of cash around. You can try using debit cards to accomplish the same result. Either way, cutting up those tempting credit cards is a proven way to put an end to overspending.

Set more realistic budget goals

A friend of mine used to spend about $1000 per month on alcohol and bars. Not kidding! He wanted to drastically reduce this, so he set himself a monthly budget goal of only $50 per month for alcohol.

And do you know what happened?… He absolutely blew it! He found it extremely hard to quit cold turkey. The truth is, people don’t refashion their spending habits overnight.

If you’re having problems overspending, have a look back at the goals you’re setting for yourself. Are they realistic? Is there a way you can scale back slowly to form new frugal habits?

Make shopping lists

Before heading to the grocery store, make a list of the stuff you need to buy. When you’re at the store, only buy stuff on your list! Sticking to a written list helps avoid impulse spending or getting distracted from your original shopping mission.

Work on your FOMO

A lot of unnecessary spending stems from the feeling of wanting to fit in and having what others have (or don’t have). The sooner you can kick this feeling, the better it is for your wallet.

Check out our full post on avoiding financial FOMO. This will help you redirect the dollars you’re spending on random purchases and funnel it more towards stuff that actually adds value to your life over the long haul.

Have a release valve

Sometimes the itch to splurge on something needs to be scratched. Budgeting isn’t about sucking all the fun out of life and never spending a cent on luxurious items and experiences. Splurging (in moderation) is a part of life and should be part of your budget too!

So, figure out small ways to treat yourself within the confines of your budget. Small splurges sometimes give you the same dopamine rush as big splurges. They just cost a lot less!

4. Switch up budgeting methods

A common reason people fail at budgeting is because they overcomplicate things when they’re starting their budgeting trek. Perhaps a simpler, less rigid budgeting system would help?

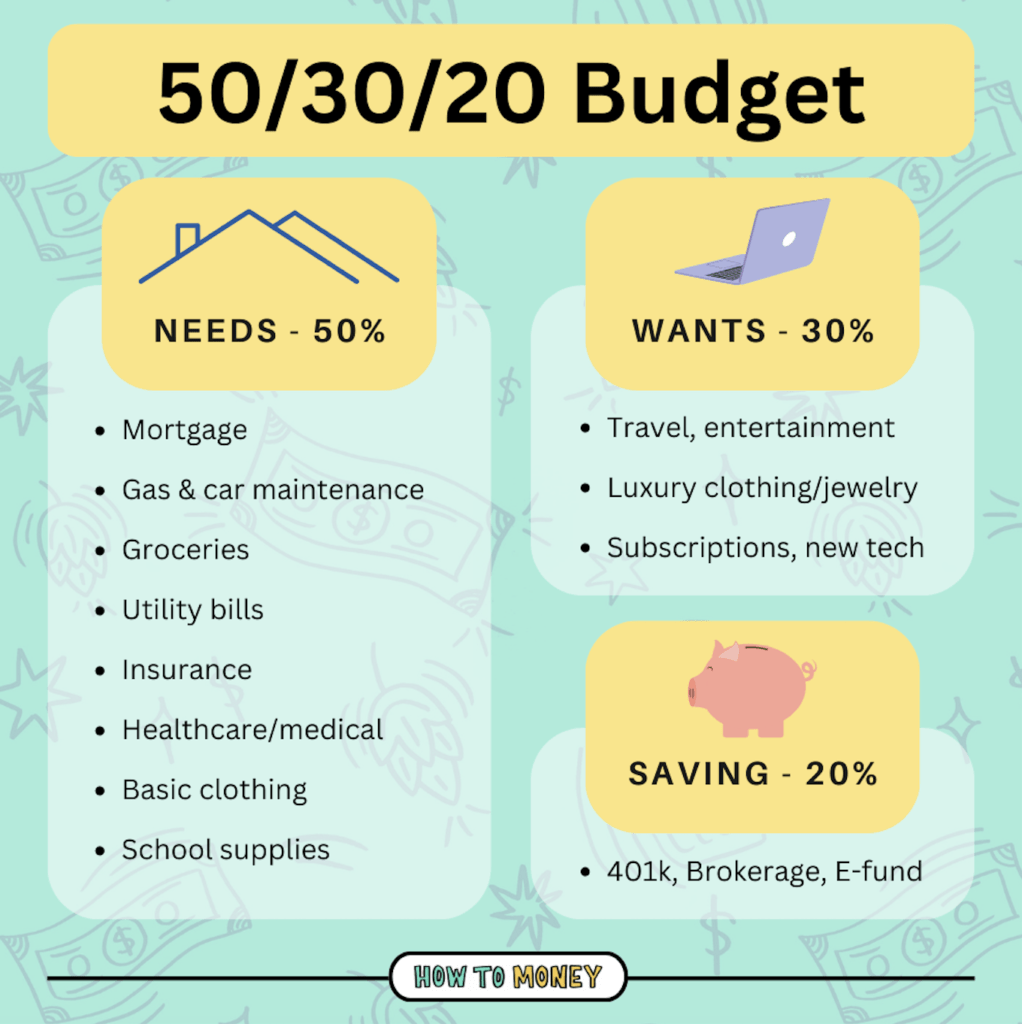

For example, instead of tracking every dollar and cent, you might have more success by using a basic 50/30/20 budget. Or, perhaps just an 80/20 budget would be even simpler. These methods involve setting aside 20% of your income for savings, and spreading the rest of your money across needs and wants.

On the flipside, maybe your budget is too broad and you need to drill down into your specific spending categories more. A zero based budgeting system might be better suited to you, allowing you to specify exactly where each dollar should be spent.

Like we mentioned earlier, everybody budgets differently. So it’s OK to keep trying different budgeting methods until you nail the one that works best for you.

5. Start paying yourself first

Another very common reason people feel their budget isn’t serving them well is that they don’t seem to be saving enough money at the end of each month. If this is the case for you, try paying yourself first!

Paying yourself first means that as soon as you get your paycheck you transfer a specific amount of it immediately to your savings accounts. Whether it be retirement savings, sinking funds, or general long-term/short-term savings. By deducting that money first it completely removes the temptation to spend it on something else.

If your workplace has a 401(k) plan, set up automatic contributions from your paycheck (and be sure to get any match possible from your employer). Outside of a 401(k), you can set up automatic recurring transfers from your checking account to various savings accounts immediately on every payday.

Paying yourself first is super important if you’re trying to build wealth with a small income. It can be really tempting not to invest at all if you don’t have much money. But small savings add up over time, and compound greatly!!

6. Make it more fun and gamify

Do you know why video games are so fun? Because there are levels, challenges and rewards. Making progress becomes a fun endeavor.

Well, have you thought about trying to make your budget a little more “gamified”? Here are a couple of ideas…

- Money challenges: Try some of these money saving challenges to spark some fun in your money life.

- Have a competition: For couples budgeting, you could try a friendly competition against your partner. Who can out-frugal the other person? Or, maybe you could challenge a friend who has similar money goals to an enjoyable money-saving competition.

- Better define your “levels”: Chop up your big goals into tiny little milestones. A thousand small wins on the journey towards that epic win will help keep you motivated along the way!

- Celebrate constantly: Sharing wins with others (kinda like humble bragging) keeps you motivated and stokes more money conversations. Join the HTM Facebook Group if you need a place to brag about your successes!

All in all, budgeting can be as boring or as fun as you want it to be. A little creativity and positivity goes a long way!

7. Get a side gig or new job

Earning more money doesn’t solve all your financial problems. Sometimes it actually adds fuel to the fire.

That being said, if you’re completely squeezed financially every month and have a very tight budget, sometimes making an extra few hundred dollars can be really helpful.

The good news is, there’s no shortage of gig apps or after hours jobs these days. If you’ve got access to a cell phone, computer, or a car there are a ton of opportunities where you can start making money right away.

Careful though, not all side gigs are equal. Here’s a guide to choosing the best side hustle for you.

8. Tie your budget to more meaningful goals

Our last tip to help fix a failing budget budget is to make it more personal.

It’s easy to get lost in the numbers, spreadsheets and calculations… But the reason budgets exist in the first place is that they help you achieve your biggest dreams in life! Sometimes we just need to remind ourselves what those dreams are, and make sure our budgets are pointing us squarely in that direction.

For example, my wife and I are trying to cut back on our restaurant spend each month (this is tough, because we love happy hours!). But, another way we can think of this budget item is that when we skip that restaurant visit, that means cooking together at home and enjoying some sweet family time. Eating home cooked meals with parents and siblings is one of our cherished childhood memories, and we’d like to pass that along to our kids.

Anything you can do to tie your spending to your values in life will make your budget more successful and sustainable.

9. Build a buffer

Life happens.

Although planning out the month in advance while budgeting is a great way to anticipate upcoming costs, sometimes expenses may catch up by surprise. In this case, it can be helpful for some folks to have a buffer in their budget to catch all of those seemingly random expenses that seem to pop up!

Suddenly, that last minute baby shower invite doesn’t throw you off of your budgeting game. You simply take that money from your buffer fund, and move right along without having to redistribute all the money in your budget.

The Bottom Line:

Sometimes budgeting can take a bit of trial and error. Plus, as your financial situation changes and grows over time you’ll need to adapt and make modifications to match.

If your current budget is failing, congratulations. Most people don’t even have a budget. Begin by reflecting on what went wrong, and continue striving for a system that works for you.

Related posts: