Should I buy it? With the amount of advertisements we see on a daily basis, chancer are you ask yourself this question on the daily.

We’re not here to tell you what you should or shouldn’t be buying with your hard earned dollars. And there’s no clear answer anyway because everyone’s financial situation and lifestyle is different.

But, we can tell you this: living within your means, practicing self control, and knowing when you have “enough“ are invaluable skills in life. They can mean the difference between living paycheck to paycheck your whole life or growing massive amounts of wealth.

Strap in, there’s a lot of self discovery in this post.

These questions below will help you determine the true personal value of something and decide whether you should buy it or not. It’s important to be brutally honest with yourself, as YOU are the only one responsible for the outcome, whichever decision you make.

1. Is this a need or a want?

Let’s go back to budgeting 101 for a moment…

Needs are things that are absolutely necessary to live a healthy and safe life. For example, food, clothing and shelter are necessities. We need these to survive.

Wants are modern luxuries we can live without. Flashy sunglasses, aftermarket car modifications, or bling bling on your pets collar are good examples. These are things you might want, but you definitely don’t need them to survive.

Right now, your budget probably covers a mix of both needs and wants. And that’s a good thing!

Life’s luxuries and fun experiences are things you should spend your money on.

But, you notice the majority of your money is going towards unnecessary wants, you may be falling victim to lifestyle creep. It’s a slippery slope! Because the more excess stuff you accumulate in life, the more you want and crave.

So, is this thing you are considering buying a need or a want? How much of your budget have you already allocated to lifestyle upgrades? Is this purchase excessive?

2. Can you afford it without going into debt?

Spending money you haven’t earned yet never works out well. One of the golden rules of credit cards is only buying things you have the cash to cover.

It is true, of course, that large purchases like a house or college education might need to be financed in order to afford them. But for anything else, it’s best to only buy things you have saved money for.

Also, taking on debt is a sure way to pay more than the sticker price for something. Sure, the sticker price might be $100 at the time of purchase, but with fees, interest, etc. you could be paying double that cost over the long run!

So if you have to take on debt, it’s a clear sign that you probably shouldn’t buy it.

Related- Creating a Debt Payoff Plan

3. Will buying this strain you financially?

Adding to the point above… Even if you’re not going into debt to buy something, that doesn’t automatically mean you get pounce at the purchasing opportunity.

Usually buying X, means you have less money to afford Y. Life is all about tradeoffs, right!?

Spend some time pondering whether picking up this new item will strain your bank account. It might bring your balance down to uncomfortable levels, causing money anxiety.

We recommend always maintaining a 3-6 month emergency fund, which should only be used for emergencies. If you have to dip into your savings to afford things, you should think twice about buying it.

4. Is this the absolute best deal?

Doing some competitive research and shopping around can save you meaningful dollars. There are a number of deal sites and apps that can help you quickly find potential coupons and discounts. For example, browser extensions like Honey and CapitalOne Shopping can search the web for coupons which can be applied to your cart!

Also many retailers these days have the ability to add items to a “wish list“. These have a double benefit…

First, putting things on a waiting list gives you time to walk away and reconsider your purchase. Sometimes after a few days, the thrill of buying something fades away and you realize you don’t actually want it anymore.

Next, many retailers will send you price alerts, discount coupons, or notify you when they have an upcoming sale.

Spending time shopping around for the best price is always a good idea. And remember, you can always try asking for a discount!

5. What are the secondary costs?

Time, maintenance, insurance, repairs, accessories… These are all examples of secondary costs that may pop up later after a purchase.

The sticker price of an item might be great, but after considering all of the hidden secondary costs, perhaps it’s not such a great deal after all.

For example, you might be considering buying a new TV. But, after thinking about the secondary costs, you realize that you also will need upgraded compatible cabling, a new universal remote, and different size wall mount.

All these small expenses really add up! Not to mention the $50 in pizza and beer you promised your friend to help you install the new set-up.

Secondary costs might turn a $500 item into a $800 expense. Be sure to run the numbers first. And include any ongoing costs when you’re considering whether or not you should buy that item to begin with.

6. How many hours will this item cost me?

Have you ever calculated your personal hourly rate? It’s a really cool mental exercise that can help you determine how many working hours it takes to afford stuff.

First, take your annual salary and divide it by 2080 (this is how many hours are in a year if you work 40 hours per week for 52 weeks). For example, if you earn $50,000 per year, your hourly rate is about $24 per hour.

Using that hourly rate, you can now calculate how many hours you’d need to work in order to buy something. So if something you want is $100, and your hourly rate is $24, you’d need to work a full 4 hours just to afford it.

This is a great way of reframing any purchase you’re thinking of making. It’s easier to swipe your card when you’re forking over dollars, but what about when it costs you something even more precious, your time? Is that purchase really worth it now?

7. Can I borrow or rent this instead?

Before you swipe (or tap!) your credit card, ask yourself if it’s possible to borrow or rent this item for cheaper.

Borrowing items you’ll only use a few times is a great way to save money and deepen your relationship with your neighbors and community. Try checking your local buy nothing group on Facebook, where people list things they’re getting rid of to see if someone else could use it.

And nowadays, there are plenty of things that you can rent for a fraction of what it could cost to purchase that item. Tools, electronics, and clothes are just a few things you can rent to save a few bucks.

Pro tip: There are tons of freebies out there that you can take advantage of if you know where to look! 😉

8. Is there a better use for that money?

Sure, you might be able to afford this item without going into debt and without putting a strain on your finances. But is there a better use for that money?

Consider your money goals, and ask if passing on this purchase could bring you one step closer to achieving them. Will a new iPhone make you as happy as saving up a new down payment for that house? Maybe! That’s up to you to decide.

A good exercise you can do is to transfer the same amount of money that an item costs to your savings account. That way, you can walk away with that new gadget you wanted while also making progress on your biggest goals.

And if you can’t afford to do both, just hold off on the purchase until you can.

9. Who are you buying this for?

Mentally and emotionally, who are you trying to impress with this purchase?

Social media is a huge part of our lives now, and it’s easy to be influenced by what you see online. After scrolling for a few minutes, it’s not unlikely that you’ll start to compare yourself to the people you see in your feed.

Take a second to remember that a) social media is a “highlights reel” that doesn’t reflect everyday life, and b) it never tells the whole story.

That beautiful kitchen you see on an influencer’s page could be entirely funded by credit card debt. The friend who is constantly vacationing at all-inclusive resorts might have no savings whatsoever.

So make sure that this purchase reflects your values, and that you don’t just want it because you want to impress others.

Sometimes we spend to “keep up with the Joneses” without even realizing it! But if we want to make smart money decisions it’s crucial to keep that reactionary spending in check.

10. What is the “cost per use”?

When in doubt, I try to think about the “cost per use” of an item. This can help you to determine whether or not similar purchases in the past have brought you value.

All you do is take the price you pay and divide it by the number of times you think you’re planning to use it.

For example, if you purchase a fancy coffee maker for around $400, but you keep buying coffee out and only use it 10 times, the cost per use is $40.

But if you use that coffee machine every day for 6 years, the cost per use is only $0.18!

This isn’t a hard and fast rule, but sometimes a lower cost per use suggests that an item has brought you more value.

11. Will it add value to your life?

Lastly, it’s important to start thinking of purchases as the value that they can bring into your life.

Will this actually move the happiness needle for you? Asking this question can prevent you from making purchases that don’t actually align with your beliefs.

Some big ticket items are hard to think about spending money on, but actually provide a huge amount of value.

For example, spending $8,000 installing a backyard deck might be stressful to think about.

But, creating a space where your friends and family can come together and enjoy each other for decades, making lasting memories, might be well worth the cost.

On the flip side, you might really want to buy a new fancy dress. But after thinking about your lifestyle and true values, you realize a new dress will probably just take up a permanent residence at the back of your closet after just a few wears.

The more money you save by avoiding purchases that don’t add value, the more you can spend on things that you do value!

12. Can you delay this purchase?

Another great way to decide whether or not you should buy something is to consider the timing of this purchase, and whether or not it can be delayed.

For example, once it hits around October every year, I try to keep purchases for myself to a minimum knowing that the holidays are around the corner. Instead, I’ll keep a running list of things I want, and when family members ask me what I want for Christmas, I actually have a solid list of purchases I’ve been delaying. I get something I need, and they get the satisfaction of giving a gift they know I’ll use. Win-win!

Another way timing can affect your purchase is to take the current season into consideration. For example, if there are only 2 weeks left of summer, that pickleball court summer pass will be worth less than if you decided to get it next summer right at the start of the season.

Reflect on your purchase

If you end up deciding to make the purchase you’ve been debating about, it’s important to remember to reflect on your choice down the line.

A few weeks after buying something new, take some time to think about whether or not you are happy with your purchase. Doing so can help to inform your decisions in the future.

For example, if you purchased a gym membership a few months ago, but have only gone twice, it could be a good idea to set a mental reminder to avoid aspirational spending.

On the flip side, if you find that you were totally satisfied with your purchase, you now know that similar purchases have the potential to bring you joy.

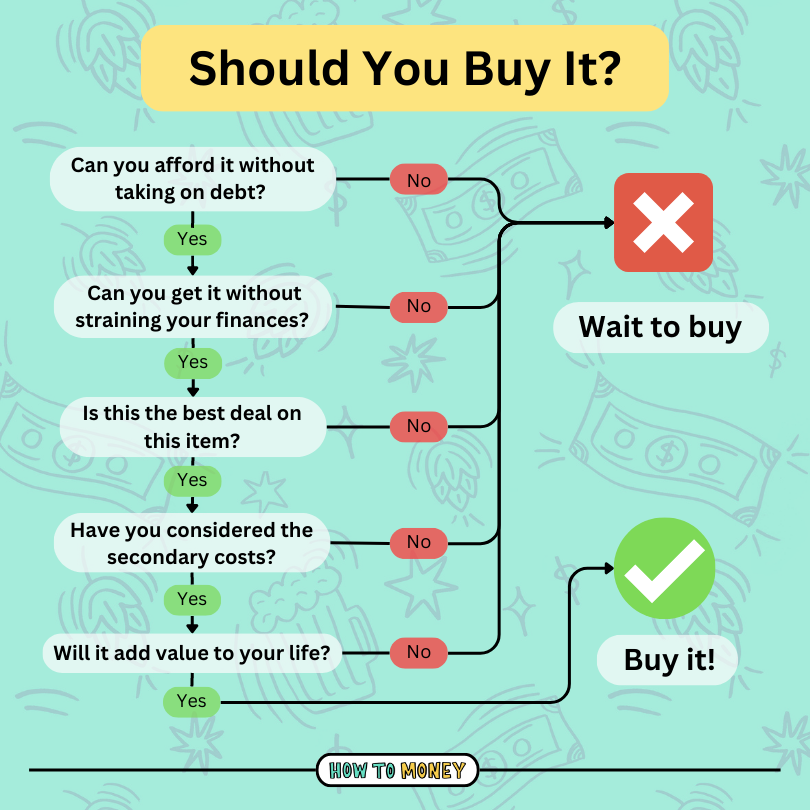

Should You Buy It Flowchart:

Here is a flowchart with a subset of questions. If you answer “No” to any of these, you should probably hold off on making that purchase!

The Bottom Line:

We all make purchases we regret sometimes, but incorporating these mindful spending questions into your life can help you significantly cut down on them.

At the end of the day, the less money you spend on items that don’t bring you value means more money you can funnel towards your bigger money goals and the purchases that bring you the most joy!

Related Posts: