So much of our lives revolve around our credit scores. Good credit can help you secure the best terms for home or car loans, avoid having to pay deposits to utility companies, and even allow you to nab the best credit cards with great rewards and bonuses!

However, if you’ve gone through financial hardship in the past and missed a few bill payments, you probably feel like you’re still being punished for prior mistakes. Having a lower credit score can lead to getting bad terms on loans or being turned down altogether. It can mean the difference between getting swiftly approved to rent an apartment, or struggling to find a place to live. Some government jobs even refuse to give certain security clearances to those whose credit has seen better days. Ouch!

Rebuilding your credit takes time and consistency, and while there is no quick fix, it’s definitely a worthwhile pursuit. This is why it’s so important to take action towards repairing your credit today. Future you will be thankful you did!

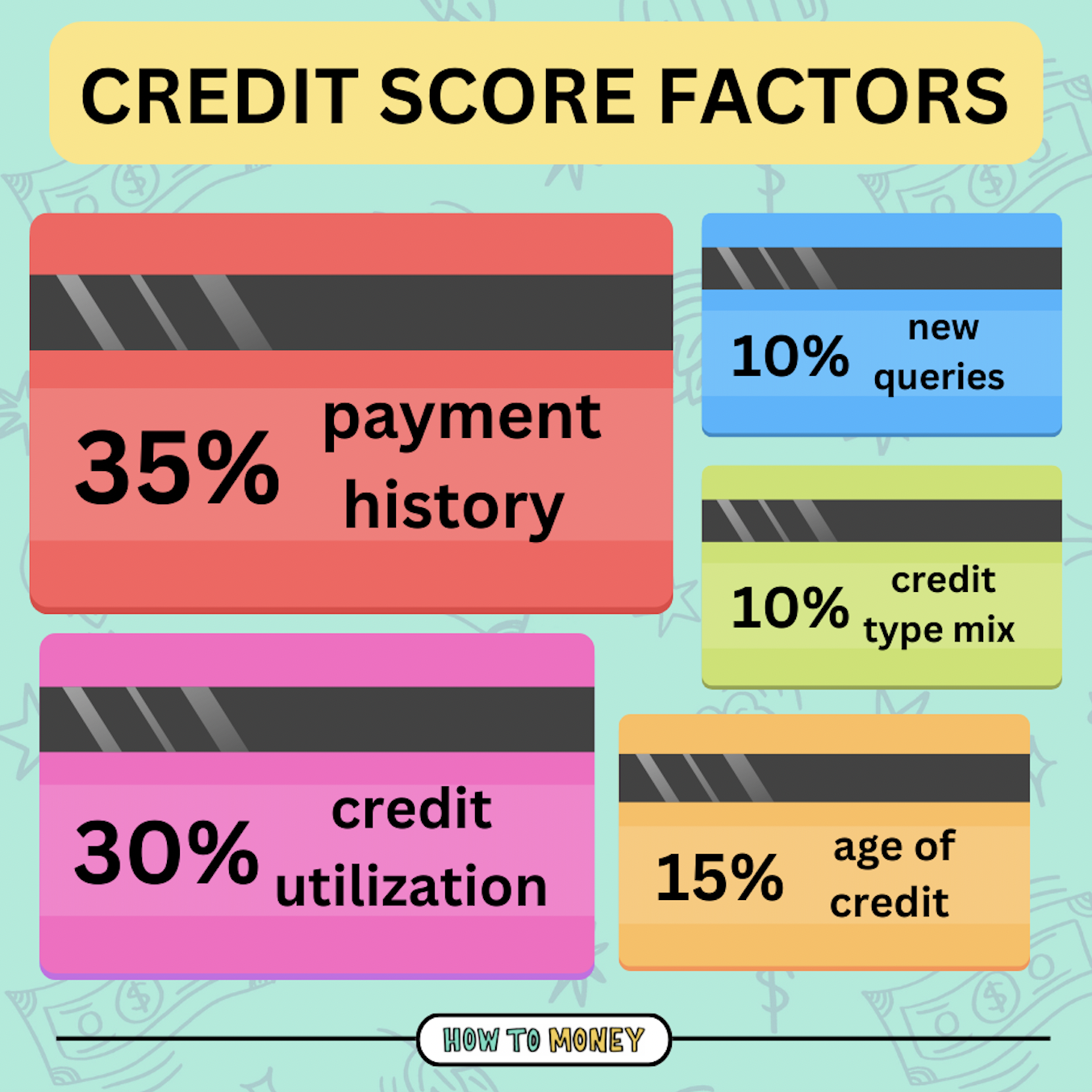

What influences your credit score?

Credit bureaus monitor and report on these 5 main factors to determine your credit score…

Payment History – 35%

Payment history is the single biggest factor impacting your credit score. Credit bureaus keep a very detailed track record of payments on all your accounts, and this is updated each and every month. A single missed payment (no matter the amount, no matter how late) can stay on your credit report for YEARS. It is absolutely paramount that you make all payments to credit cards, retail accounts, installment loans, and mortgages on time, every time.

Credit Utilization – 30%

Your credit utilization is how much credit you actively use in comparison to the amount of credit that is available to you. For example, if you have $10,000 of credit available to you, and you carry a balance of $2,000, your utilization would be 20%.

Credit utilization is calculated across all your loans, including credit cards, student loans, personal loans, car loans, and any other lines you have access to. Having more access to debt but using very little of it will keep your utilization low which boosts your credit score!

Credit Mix – 10%

Credit Mix is determined by the different types of credit you have open. The credit bureaus like to see you using different types of loan products. For example, if you have a personal loan, a student loan, and a few credit cards, it may reflect better in your credit score than only using one single credit card. So aim to accumulate a potpourri of different credit types that will enhance your mix.

Credit History – 15%

Credit history is the age of your active credit accounts. For example, if you opened your first credit card at the age of 18 and now you’re 38, your credit history would be twenty years for that particular credit line. Keeping older credit lines open for a longer period has a positive impact on your credit score. More on this later…

Recent Hard Inquiries – 10%

Hard inquiries occur when you’ve made a recent application for new credit. A common example of this is applying to open a new credit card. If you apply for five new cards over the course of two months, it will bring your score down. Too many hard inquiries in a short amount of time can be a drag on your credit score, so be sure not to overdo it!

Tips to Rebuild Your Credit Score

Rebuilding your credit requires dedication and long term consistency. Changes don’t happen overnight, which can feel discouraging! But if you stick to it, you should be able to see some small, positive changes within about 30-60 days.

As you work to rebuild your credit, make sure to keep track of your credit score. Nowadays, you can check your credit score as much as you want without hurting yourself in the process. You can use a website like Credit Karma to check your score easily and often. This does not negatively impact your score, since you’re not having your credit report pulled by a creditor.

Remember that perfection is not the goal here. You don’t have to shoot for an 850 credit score to enjoy the benefits that good credit can bring to your life! A good number to shoot for is 680, which is a solid mid-tier score. It can yield good rates and bring you to a place of credit decency. After that it’s smart to aim even higher. Having a credit score of around 740 will qualify you for the best rates from pretty much any lender out there.

So now that we know what we’re shooting for, here are some steps you can take to slowly improve your credit!

1. Pay ALL Your Existing Accounts on Time

The first step towards repairing your credit is to make sure you’re making ALL your debt payments on time. Check out both the debt snowball and debt avalanche methods – they both include making minimum payments on all credit lines each month.

If you struggle to remember to pay your bills on time, try putting your bills on autopay! Automating your finances allows you to frontload the time and energy of paying your bills each month, and avoid getting penalized for missing payments.

2. Lower Your Utilization

Utilization is the amount of your available credit you use each month. Credit agencies don’t like to see you using all of your available credit, because it makes it look like you are relying on credit cards to make ends meet or are spending irresponsibly. The less credit you’re actually using, the better it reflects on your credit score!

Experts suggest keeping your utilization at or under 30% of your available credit, but you can even shoot to keep it as low as 10% if you’re feeling like an overachiever who really wants to send that score soaring!

There are 2 ways you can lower your overall utilization:

- The first is to pay down your debts (or make more frequent payments). Paying your credit cards off twice a month will aid you in your quest to keep your utilization lower.

- The next way is to increase your available credit. You can call your credit card company and ask for a credit limit increase (just don’t *use* it!). This might sound intimidating but even just a small credit limit bump can do wonders for your credit score.

If you’re carrying around some credit card debt that’s keeping your utilization high, it may make sense to focus on paying down these cards. If this sounds like you, be sure to check out our podcast episode on building a foolproof plan to pay off debt!

3. Avoid Opening Too Many Credit Cards At Once

You might think that one way to lower your utilization is to apply for more credit cards. While opening more cards might help with utilization, it could also hurt you by having too many hard credit pulls. Applying too often makes it look like you need these cards to get by.

You might also run the risk of lowering your credit score even further as a result of getting denied for that new line of credit.

4. Get A Secured Credit Card

If a low credit score is making it difficult for you to get approved for a credit card, opt for a secured credit card! Secured cards require an upfront deposit which you then borrow against like a regular credit card. Think of it like a car or home loan- if you don’t pay your card off, they have collateral.

Eventually, if you prove your ability to use the secured card responsibly you’ll be given back your security deposit and graduate to a regular credit card. You could also ask your local credit union if they have a credit builder program available. Those can be massively helpful.

Related:

5. Don’t Close Your Credit Cards

If failing to pay your credit card bill is what damages your credit in the first place, you might be wondering why we aren’t suggesting that you close all your accounts, cut up your credit cards and toss them into an active volcano. First off, you’re not Bear Grylls. It’s just too dangerous. Also, it’s because your credit history makes up about 15% of your credit score!

Credit history takes into account how long all your credit lines have been active. So closing your older accounts can negatively impact your credit score. If your credit cards have a $0 annual fee, it’s in your best interest to keep them open. Just make sure to responsibly use them at least once a year so that the account doesn’t get closed without your knowledge.

Pro tip: If you have a credit card with annual fees, you can usually call the bank and request a downgrade. Ask to switch to a basic credit card (using the same line of credit) with no annual fee. This lets you keep the credit history active, without having to pay annually to keep the card around!

6. Diversify Your Credit Mix

Credit Bureaus like to see a mix of different credit cards and loan products, so opening a different type of credit line can help give your credit score a boost. A credit builder loan can help you to diversify your credit and grab back those precious points! Remember that taking out a credit builder loan can result in a small credit score drop in the short term, but ultimately it can help to strengthen your credit moving forward.

Where can you go to get a credit builder loan? A company called Self can help! There’s no hard pull on your credit, and they allow you to “pay off” your Self account over time and report the activity to all three credit bureaus on your behalf. At the end of the specified term, you unlock your savings and get the money you paid back minus interest and fees. You can even automate the monthly payments in order to ensure that you don’t end up shooting yourself in the foot.

7. Check Your Credit Report For Mistakes

Another important step to take is to make sure you aren’t being penalized for a mistake you didn’t even make!

Pull your credit report and check it for any inaccurate information that could be hurting your score. If you find anything, be sure to dispute it.

You’ll find lots of places on the web that will make you pay to see your credit report. Don’t do it. Thanks to federal law, you can get your full credit report for free from each bureau once each year online at AnnualCreditReport.com. Because of Covid-19 the bureaus have actually made all reports free on a weekly basis for the time being.

8. Become An Authorized User on Someone Else’s Card

If you have someone in your life who is kind enough to let you piggyback off of their good credit, then becoming an authorized user on someone’s credit card could help catapult you back into credit decency. Beware though, this one comes with risks…

If you end up with a piece of plastic attached to their account but don’t use it responsibly, you could hurt this person by being an authorized user. A way around this is for them to make you an authorized user without giving you access to their card. That way, you reap all the benefits of their good credit without putting them at risk!

9. Try Experian Boost

If you’re looking for an easy way to increase your credit score by about 8-10 points, consider trying Experian Boost. This product allows you to get a bonus boost for paying utility bills from your bank account by linking it. The best part is that it’s totally free!

10. Watch Out For Scams!

It takes time to rebuild your credit, and unfortunately there is no quick fix. So be sure to run swiftly in the opposite direction if someone promises you a short-term remedy. These are almost always scams. There is no way that they can remove accurate information from your credit report! And they often charge a lot of money for their “services.”

It often takes a while to dig yourself into a bad credit score hole and it’ll take a little bit of time to climb out too. If that pitch sounds too good to be true, it inevitably is.

The Bottom Line:

Repairing your credit can seem like a daunting task. It takes sustained intentionality and hard work, but it is absolutely worth it. The sooner you start, the sooner your financial life can get back on track.

Remember that the things in life worth doing often take time. YOU are capable of rebuilding your credit score, and if you need some added support, try posting in our HTM Facebook group! It’s full of people who are all on their own money journeys supporting and helping each other to crush their money goals!

Related:

- Credit Card Best Practices

- Top Credit Score Myths (learn what’s right and wrong!)

**Pic by Randy Fath on Unsplash

* Advertiser Disclosure: How to Money has partnered with CardRatings for our coverage of credit card products. How to Money and CardRatings may receive a commission from card issuers.

* User Generated Content Disclosure: Responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.