When someone tells you they’re in the market for a car these days, it seems like the appropriate response should be “I’m sorry,” or to wish them luck on their brave and perilous journey.

It’s true, car prices have been rising, making an already somewhat stressful situation even more harrowing. Between January 2022 and January 2023, car prices rose 4.2%, leaving the average cost of a new car at over $48,000. That’s an average monthly payment for a new car coming in at a whopping $716. That means that it costs about $9,000 each year just to own a car. Yikes!

Sure, $716 every month might seem manageable at surface level. But then there’s all the other “hidden costs” of car ownership that most people forget about.

Not to mention, transportation is just one part of your budget. You need to make sure that it doesn’t get too overgrown and take over the entire thing like the man eating plant in Little Shop of Horrors. So how do you go about finding reliable transportation without going broke?

Does it Really Make A Difference?

Okay, so $700 a month is a lot of money. But does it really make a difference in the long term?

The short answer is yes. Sure, if you’re a total car nerd, then maybe it does make sense for you to spend extra money on a vehicle you love. If that sounds like you, and that’s your craft beer equivalent, then go for it! But if cars for you are just a way to get from point A to point B, there are far better things you can do with that money instead.

If you can cut the yearly cost of owning a car even just in half, that’s an extra $4,500 that you could spend on your favorite hobbies, family vacations, or even to pad your emergency fund!

Plus, the savings can be amplified if you invest that monthly savings. Using the rule of 173, we know that if you cut the annual cost of car ownership in half and invested the difference, you’d have $64,875 in just ten years. That could be enough for a home down payment! This is the exact reason why you should work to keep your transportation costs lower than average if cars aren’t something you highly value.

How to Buy A Car Without Breaking the Bank

You don’t need to shell out all of your cash to get from point A to point B. In this post we’re going to break down the car buying process and offer some realistic tips to help you save some serious cash.

Step 1: Make a budget

The first step in any car buying strategy should be making a budget. It doesn’t need to be terribly complex or exact. It just needs to suit your needs, both financially and in terms of transportation. Your car budget should include both upfront costs, as well as ongoing costs.

Upfront costs: This will be the cost of the car (or down payment if you are planning to get a loan) as well as taxes and transfer/title fees.

Ongoing costs: Loan payments, registration, insurance, maintenance, gas, etc. All of these are recurring costs you’ll need to budget for.

If you have cash savings, that’s a huge head start. We almost always recommend paying cash for cars if you can afford to do so. It might even make sense delaying your purchase to save up more cash to buy a car outright. The more savings you can build up on the front end, the less your car will end up costing overall.

Getting a car loan should be a last resort, and we’ll talk about auto financing in more detail a little further down. Even if you get a loan to buy a car, you’ll still need some money for a down payment. And a healthy emergency fund as well.

As a rule of thumb, the ongoing budget for a new car should be no more than 10% of your after-tax income. For example, if you make $5,000 each month, shoot to keep your transportation costs under a $500 each month ceiling. If you can get it even lower than that, we would definitely recommend doing so!

Reframing how you think about transportation spending can help. Instead of thinking about the upper limit of what you can spend on your monthly transportation, think about how much you can shrink that number instead.

How much should you pay for a used car?

Your goal for buying a car should be to pay the least amount of money possible, while also getting a safe and reliable ride that will last you for a number of years, potentially even decades. Tough task? Yep! But is it impossible? Nope!

Most people think the cheaper a car is, the less reliable it is. But that’s not always the case! I know many people that have bought cars for under $10,000 and never had any issues. I also know people who have paid over $30,000 for vehicles and have nothing but troubles.

Don’t fall into the trap of thinking that the more you spend on a car, the better it will serve you. Expensive cars might be newer and have less visible wear and tear, but that doesn’t automatically equate to more safe and reliable. In fact, ordinary brands like Mazda and Toyota smash luxury brands like Audi and Mercedes when it comes to reliability.

While there’s no exact amount you should budget to pay for a car, we’d recommend shopping for cars within the $10,000 – $25,000 range. This range covers a TON of extremely reliable vehicles, different builds and a variety of conditions to suit your needs. Consumer Reports is a great place to turn to research the best vehicles in this price range.

Cars in the $5,000 – $10,000 range can still be great vehicles, but there’s a little more risk in the lower price ranges. Older cars have more history to uncover (some of which is hard to dig up – especially if there have been multiple owners over the years) so finding a gem in this price range can be tougher.

Should you buy new or used?

Part of making a budget is deciding whether it makes the most sense for you to buy a new or used car. In most cases, it’ll probably be best to purchase a pre-owned vehicle. However there are a few instances where purchasing a new car can make sense for some folks.

Why you probably should buy USED:

The biggest reason why most people should choose a used car is depreciation. New cars take a massive hit in value once you drive them off the lot. It’s estimated that cars lose about 20% of their value within the first year, then about 15% each year after for the next 4-5 years.

Why not let someone else take that massive hit for you!? A 5-6 year old vehicle is still relatively new! Sure, it doesn’t have that new car smell, but the features are likely just as modern as the newest models. And you can spend $3 to bring that smell back anyway.

Another big reason to buy used is that many of the secondary costs are cheaper. Taxes and insurance costs will be significantly lower, which makes a big difference in the ongoing cost of owning that vehicle. It’s the gift that keeps on giving.

When it might make sense to buy a new car:

If you’re planning to buy an EV, you’ll find that newer models have longer battery range and better battery technology. If you’ve got the means to purchase a new EV, and plan on owning it for 10+ years, splurging and taking that depreciation hit might be worth it for you. Plus, there are significant federal rebates that can reduce the price of that new EV purchase.

New cars, of course, also come with the newest safety features. If that’s really important to you and will make you feel safer transporting your family around around town, a new car might make sense.

In any case, the longer you plan on owning a new car, the more it begins to makes sense financially. If you can commit to owning that new car for at least a decade, it becomes far less of a devastating decision financially. Your ownership timeline matters.

Do you need a car right now?

You should also take some time to think about when purchasing a vehicle makes sense for you. If you don’t have the cash on hand for a new car, is it possible to repair your old car instead of replacing it? Could you live without a vehicle for a bit?

We talked about the average car costing $700 per month… Instead of jumping right into a car loan, could you delay your purchase by 10 months and save that money instead? If you saved for 10 months at that rate you’d have $7,000 to throw at a new car. You might even be able to buy one outright at that price!

As for replacing your old car, does it need to happen immediately? Sometimes, we may think our older cars are money pits when really we’re just feeling over our old hunks of steel and want to buy something bigger and better. We can let our emotions dictate our finances.

Before you jump into action and pick up that sweet new ride, actually do the math to find out how much you’ve spent on maintenance year over year. You may find that the average annual maintenance spend on your current car is much less than purchasing a “new to you” car.

Step 2: How will you pay for it?

The next step in purchasing a car is to decide how you will pay for it- with financing or with cash?

It is almost always better to pay for your ride in cash. With cash, you have more room to negotiate, and since you won’t be paying interest, you’ll pay less for that car overall. That’s even more true right now given how much interest rates have increased over the past couple of years.

Paying Cash: Saving for a car fund

Saving up enough cash to purchase a car outright can be a tall ask, especially when the average price of a used car is around $26,000. So how can you acquire a lump sum of money short of selling your organs on the black market?

One way you can start saving more money each month is by switching to a bare bones budget, which is a budget that contains only your needs. This is not by any means meant to be a permanent thing. But operating based off of your BBB for a few months can help you to create the margin you need to save up enough to get that car.

As you’re building up a new car fund, be sure to save all your money in a high yield savings account (HYSA). These accounts will make sure the cash pile is slightly out of reach (so you don’t get tempted to dip into those savings for other items) and also will make sure you’re earning a little bit of interest on your money.

Getting a Car Loan:

In certain situations, you may find yourself unable to pay in cash for a car. For example, if your current car breaks down and it would cost more to repair it than it would to purchase something new. Assuming you need it to get to work and have already explored other alternatives like walking, biking, and public transportation, you may find yourself needing to finance a car. If that’s the case, here are a few guidelines to help you finance a car without shooting yourself in the foot.

One of the best places you can turn to for financing a car is your local credit union. Not only do they offer low rates, but they are also known for their great customer service! We recommend shopping around with a few lenders before settling on financing. Definitely check with a couple of local credit unions. And don’t feel pressured to just go with the first place you meet!

When given the option, do not take the longest option that’s available to you. The maximum length you’ll want to agree to is a 4-year loan. If you can’t afford the monthly payment on that timeline, then the truth is that you should be looking at cars that are much less expensive.

Longer loans are becoming more and more normal. But they’re terrible for your finances. Those 7-year loans will leave you having paid way more money for a vehicle than it’s worth. You’ll also be underwater on your loan for a longer period of time. This is a risky financial move, because if you get into a crash or need to sell the car in a pinch, you’ll still be in debt and you’ll likely need to take on even more to finance that next ride.

The general rule of thumb for financing is 20/4/10. Be sure to put at least a 20% downpayment, get a 4-year loan term (at most!), and make sure your monthly payments are no more than 10% of your monthly expenses.

Step 3: Determine Your *Actual* Needs

Sure, that fancy two door sports car might seem like a need. But deep down we both know that it isn’t really necessary. When planning to buy a new car, it’s important to think about both your current and future needs so that you can find an affordable vehicle that works with your lifestyle.

Here are a few factors to consider when narrowing down your car search:

How big is your family?

It’s important to take the size of your family into account when deciding which car model you’re going to purchase. Do you plan on participating in that multi-family car pool? Do you plan on growing the size of your family within the next few years? If so, you may want to choose a car with more seating and safety features.

How much do you drive?

If your drive to work is 10 minutes, or if you work remotely, you may be able to get away with purchasing a cheaper, older vehicle. Whereas if you commute 45 minutes each way or more, you’ll likely want to focus on getting a super efficient vehicle that cuts sips fuel, lowering your gas bill in a meaningful way.

Should You Consider an EV?

In some cases, switching to an electric vehicle can be a total win. They can typically save you money not just on gas but on maintenance too. They’re kind of like glorified golf carts! And purchasing a new or used one can make you eligible for a federal tax credit.

However, it’s not all rainbows and sunshine. Insurance can also cost more for EVs, so it’s important to do your own research and crunch the numbers for yourself.

If you’re considering purchasing an EV just because you want to go green- think again. If it’s possible to stick with the car you already have, that’s always going to be the most sustainable option! Don’t replace something that works perfectly fine for that reason.

Make A List

Now you’ve gotten clear about what you need from a car, it’s time to compile a list of viable make and model options. Consumer Reports is great for researching the reliability of different types of vehicles you’re interested in.

Why? The more reliable of a car you get, the less you’ll be forced to spend on maintenance and repairs. Once you have a list of about five reliable cars that fit your budget and your needs, you’re ready to hit the ground running.

Step 4: Find the Best Place to Buy Your Car

When it comes to finding your next car, you have tons of options for where to buy. However, not all are created equal. Here’s what you need to know about each of these places…

Virtual Dealers

Have you ever wanted to get your car out of a giant vending machine?

Virtual dealers like Carvana and Carmax can make it super easy to find your next ride. They offer excellent return policies, make shopping simple, and offer convenient delivery options.

One of the only drawbacks of these virtual dealers is that it can be difficult to find older, cheaper models. Plus, you’ll likely pay more for your car compared to what you would have paid if you had purchased it from a private seller.

All that said, this is a great option if you have a lot of cash on hand and are looking for a gently used car. They make the process simple, and in some cases they offer return policies for a full month if you don’t end up liking the car your bought!

Private Party

While finding your car through a private seller is a great option, this one tends to require a little more time, patience, and energy on your part. However, if you do find one, the savings could be well worth that time investment. Places like Facebook Marketplace, Craigslist, and Autotrader are great places to look if you want to pursue this route.

Just be sure that before you make a purchase, you ALWAYS get the car checked out by a mechanic you trust. If you don’t have one, talk to your friends and family and ask for references. This is a super important step that you cannot skip, because it ensures you won’t be buying a total money pit.

Personal Networking

This way to buy a car just might be the best case scenario! Before purchasing a new car, put your feelers out within your network. Tell your friends and family that you’re looking to purchase a new car. Someone may know someone else who is looking to get rid of an old car, and if you know them well enough, they may be willing to give you a sweet discount.

Again, be sure to get the car checked out by a mechanic. Even if someone from your network has your best interest at heart, their car might have issues that even they aren’t aware of. Better to be safe than sorry!

Dealerships

Although this is probably the first place you’d think of when it comes to purchasing a car, dealerships are probably the last place you should go car shopping. Especially the smaller ‘Buy here, pay here’ lots. We really don’t recommend buying from dealerships at all if you can avoid it. Sales people put the pressure on, and chances are you’ll pay the most inflated prices here.

If you have to buy your car from a dealership, make sure you are well researched on price trends. Do this for the make and model of the car you’re interested in. And make sure that you are prepared to negotiate too. Remember that you can totally walk away if you feel like they aren’t giving you a fair price.

**Important note!: If you are financing, it is extremely important to have loan pre-approvals and options already in place BEFORE you walk into the dealership. This is because dealerships will offer you their financing, which is usually sub-par to terms you can get elsewhere. Don’t fall into the trap of walking into the dealership and getting sold on a loan you may regret later. Bringing in pre-approved loans and terms from other lenders will help you compare and negotiate from a position of strength.

And don’t be afraid to negotiate with dealers from the comfort of your own home. Emailing a few different dealerships in an attempt to score the best deal can be one of the best routes to take.

Step 5: Do Your “Due Diligence”

Now that you’ve found a car that you like, it’s time to do the work to make sure that you’re getting a good deal. Follow these steps to ensure that you’re ready to purchase that new car.

1. Price Comparison

Are you actually getting a good deal? Make sure you spend some time looking into what this make and model of car typically sells for with a similar number of miles on it. Again, Consumer Reports is a great place to look for this kind of information. Kelly Blue Book is also a great tool for researching car values.

2. Car History & Mechanic Verification

It would be a shame if you got rid of your old junker, only to discover that your newer car is giving you even more headaches!

It can be a good idea to get the car’s history to see if it’s been in any accidents using vehiclehistory.gov. Although it does cost money, it can save you from future expensive headaches if you purchase a car with ongoing issues.

You also need to make sure that you get the car looked at by a mechanic you trust. We cannot stress this enough. A few bucks spent on an inspection can save you thousands of dollars- no joke! Do. Not. Skip. This. Step!!!!!

3. Future Maintenance

You can afford the car, but can you afford the future maintenance? It’s important to take the average annual maintenance costs of your make and model into consideration. When shopping for cars, tons of people forget to consider the secondary costs of ownership, which can leave you feeling regret years after your purchase.

Instead, put some research into which brands are the most reliable and cost the least to own over time. Hint hint… Toyota, Mazda, and Honda!! Owning a more reliable vehicle will lower your car expenses throughout life!

4. Are You in the Best Place to Buy?

I’m not talking about where you are in your financial journey. I’m talking about your physical location.

You’ve heard of medical tourism, where people fly out of the United States to receive state of the art healthcare at a fraction of the price, but have you ever thought about hopping on a flight to a different state to buy a car?

It sounds crazy, but in some instances it may make sense! For example, if you can find the car that you would like to purchase in Florida for $5,000 less than you’ve seen it locally, but you live in New York, can you snag a cheap one way flight to go get it? The savings could be totally worth the trip!

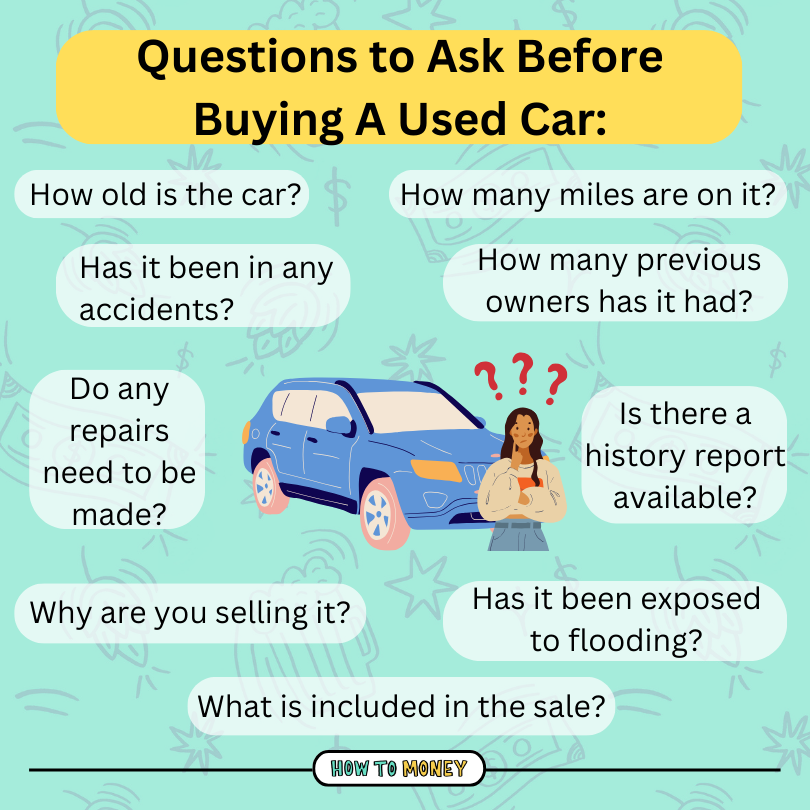

5. Ask the Seller Questions

Now, your interrogation of the seller begins. Bonus points if you can question them in a pitch black windowless room with only a single lightbulb.

Jokes aside, you’ll want to be thorough when asking the seller about the car’s history. Here are a few questions you should ask to be well informed about the car’s history.

It might seem awkward asking the seller so many questions about the car. But the fact is, YOU are going to be the one 100% responsible for this big hunk of metal after you buy it. You have every right to know the entire history of the vehicle.

The more information you know about the car, the better. Not only does this help with understanding the history, it can actually reveal advantages when it comes to negotiations!

6. Take It For a Test Drive

Lastly, make sure you take that baby to the road! Ask the seller if you can take it for a test drive, and be sure to take it on the highway. Open her up! That way you’ll know if you even enjoy the way it drives before you commit to purchasing it. Turn on the AC and the heat. Turn on the radio to make sure the speakers sound decent. Basically, kick the tires in a meaningful way.

Step 6: Negotiate the Price (and Fees)

So you’re feeling pretty good about this car, and you’re pretty sure you’d like to buy it. Now it’s time to make sure you are getting the best deal possible. Learning a few negotiation skills can help to save you money, and may even earn you some sweet additional perks. So here are a few tips to help you refine your negotiation skills.

Do Your Research

If you want to enter into negotiations feeling confident and empowered, it’s important to spend some time researching the market to understand what the car is actually worth.

Whether you’re buying a new or used car, focus on finding out the “fair market value,” which is the price that this car would reasonably sell for on the open market, instead of the MSRP or sticker price of the car. You can easily find this information on Kelley Blue Book.

Print these numbers out for your desired car’s make and model with a similar mileage and condition. Having these on hand can help the seller to understand that your counter offers are based on factual data as opposed to emotions.

Also, take notes about similar vehicles that are for sale, and bring those to the negotiation. You can usually peg sellers against each other, and remind them they are not the only options you are considering. Here’s an example of what you might say as a buyer… “This seems like a great car, but I did notice that 3 other Toyota Prius models are for sale right now with less mileage. They are the same year as yours, but yours is more expensive. Can you tell me why?”

Believe me, sellers do a LOT of research on the make/model/price before they list their cars for sale. You will have to do an equal amount of research to match their knowledge and get a fair price.

Be Realistic

If you want to be taken seriously in your negotiation, make sure your requests are reasonable and realistic. If the car you’re interested in goes for around $10,000 on average with the same number of miles on it and in a similar condition, don’t ask for it for $2,000. Negotiations are about getting to a win/win resolution, not ripping people off.

On the other hand, don’t accept a deal for something way higher than the typical price. Now that you’ve done your research, you’ll know if a seller is setting the price way above the fair market value.

Don’t Be Afraid to Take a Break

If you’re negotiating with a dealership, you need to be prepared for them to lay some serious sales tactics on you. These people are in sales for a reason- they are good at what they do!

Shopping for a car can be exhausting, and they know that. One tactic they will often use is to try and wear you down, or take advantage of the fact that you’re tired after spending the entire day test driving cars and schlepping from one dealership to the next.

If you feel yourself running on empty, don’t be afraid to take a break and leave the rest of the negotiation to another day. Tell them that you’d like to take a night to think about it, and will call them again in the morning. It is imperative that you do not make a rushed decision just because you want to put the car buying process to an end.

Ask for Extras

Now that you’ve gotten a great deal on the car you wanted, it’s time for the fun part. See if you can get a few extras tacked onto the deal, like free oil changes, or a new set of tires. The value of these extras can easily add up to a few hundred dollars of future savings.

If you are buying from a private seller, sometimes you can ask for discounts in exchange for missing items. For example, you could say something like “I notice there is only 1 key, which means I have to order another from the factory. Can you throw in $200 to cover some of that cost?”. Asking about accessories (even if they aren’t important to you) can give you leverage for a discount or throw-in to close the deal.

Dealership “Junk” Fees

If you are buying from a dealership, remember that many things are negotiable. Here are some common fees to look out for:

- Vehicle Preparation Fee: Some dealerships charge hundreds of dollars just to remove protective wrap, wash the car, take out floor mat liner paper, etc. before they hand you the keys. It’s nice of them to make the car ready, but most buyers don’t realize it comes at a high cost!

- VIN Etching: Some dealerships try to sneak in a “VIN etching” service which is when they etch the car’s VIN number into the windows. This isn’t a necessary service! You don’t need it..

- Aftermarket Parts: Make sure to review every single line item in your final paperwork to make sure you’re not being charged extra for parts you never agreed to. Sometimes car salesmen will charge for upgraded sound systems, extra installed accessories, or features you never asked for.

- Extended Warranty: You can absolutely shop around for extended warranties – don’t just blindly accept the dealer price! Remember if you’ve done proper research on typical maintenance costs for your vehicle type you might decide an extended warranty isn’t worth it.

- Advertising Fee: Some dealerships try to charge YOU for their advertising fees because they had to market the car in bigger ways to attract buyers.

Needless to say, you should thoroughly review every line item in your contract to make sure you agree to the fees. If you don’t, request that they be waived or reduced!

Stay Calm and Confident

No one wants to help someone who’s acting like a total jerk! That’s why it’s important to stay calm during negotiations, even if the seller is resistant to your offers. Make sure to always be polite, but firm. If you feel yourself losing your cool, it may be time to take a break and come back tomorrow.

Remember, as awkward as you feel, the seller feels just as weird. Make it easy on them by being nice, assertive, asking direct questions and being confident. Sellers respect that because the last thing they want is someone beating around the bush and wasting their time. They want to make a deal just as much as you do.

Be Willing to Walk Away

If you and the seller can’t agree on a price that you both think is fair, you need to be willing to walk away. There are tons of great cars out there, so you’ll be sure to find something else that fits your budget.

Hundreds of new cars get listed for sale every day. If you can wait a couple weeks, there might be a whole new inventory available for sale. Being patient will always help you to come out on top financially in the end.

Step 7: Final Steps

Hooray! You’ve followed these tips and gotten the perfect deal on a car that fits both your budget and your needs. Now it’s time to take care of a few final tasks so that you can get to enjoying your new car.

Get your hands on the title

If you bought your car from a private seller, you’ll need to have them transfer the title of the car to you. You’ll do this immediately at the time of sale. Never pay money to someone you don’t know without the title being transferred.

Sometimes, it’s a good idea to take a quick photo of the other person’s driver’s license. If tey are a legitimate seller with nothing to hide, there’s no reason they shouldn’t comply (and you can offer them a pic of yours in return). The reason this can come in handy is if you have any troubles at the DMV when transferring the title later. You’ll have their contact info and address to reach out to them.

If you bought it from a dealership, they should be able to transfer the title automatically. Follow their lead on the paperwork stuff. They know the process and do it every day.

Either way, make sure you get your hands on the car title. This *very important* document proves you own the vehicle.

Get insurance

You know when you drop your brand new phone in the one week you buy it before you put a case on it?

The same thing can happen with your new car, but on a much bigger scale. That’s why it’s important to get your car insured as soon as possible. Be sure to shop around and make sure you’re getting the best rate.

We’ve written a whole article about car insurance to help you get the best policy and rate. While it’s tempting to just call your existing insurance provider and add the new car onto your existing policy, put in the work to shop around and save money.

Register Your Car

While you do often have a 30 day grace period, it’s a good idea to get your car registered ASAP. You can check with your local DMV for what documentation you need in your specific state. Even if the dealer took care of the registration, it’s a good idea to double check and confirm that everything is in place.

Schedule Maintenance

Remember when you had that inspection with your trusted mechanic? Well, now is the time to schedule any maintenance tasks that were discovered during your inspection. Don’t wait on this. A little TLC now can prevent larger issues from arising over the time you own your car.

Mechanics and repair shops are always looking for new customers. Oftentimes they’ll offer oil change “packages” or new tire promotions to lure in business. Take advantage of this and shop around for a good value place to do your maintenance.

Step 8: Do A Happy Dance!

Now, it’s time to celebrate! You’ve done your due diligence and purchased a car. Reward yourself for all the hard work you’ve done by treating yourself without breaking the bank. Enjoy your favorite drink, cook a special day, or go on a walk (or joy ride!) with a friend or loved one.

The Bottom Line:

Buying a reliable, good value car isn’t difficult. But it does take time and effort. With hard work, determination and a little patience, you’ll be sure to get a good deal on a car that fits your lifestyle and your budget.

Cutting corners in the car buying process will come back to bite you. So as mundane and awkward as some of these steps are, we definitely encourage you to take them seriously. Putting in the hard work will be rewarded.

Be sure to check out these related posts for more tips on how to reduce transportation costs in your life!

Related Posts:

- Building Wealth with a Tiny Income

- The Pros & Cons of Living Without A Car

- The Hidden Costs of Car Ownership

Photo by Matthias Münning on Unsplash