The majority of people manage to scrape their wallets empty in order to splurge on the junk they think will make their life better. Ironically, the lack of emergency funds is likely to have the exact opposite effect.

Regardless of income levels, most people end each month with a minimal (or negative) dollar balance and no margin to weather future storms. When a storm does arrive, they’re bound to get financially pummeled, likely needing to accumulate debt or dip into retirement accounts to survive.

It’s time to proactively take the necessary steps to create more margin in your life. In this post we’re going to cover everything about emergency funds. What they are, why you need one, and how to build a war chest so that your finances are storm-proof.

What Is An Emergency Fund?

Emergency funds are accessible savings set aside for unexpected and unavoidable costs in life. It’s money that is only touched for expenses we can’t budget or plan for.

Here, at HTM, we consider saving for an emergency fund money gear #1. (If you haven’t already, visit our 7 Money Gears – a helpful guide to determining which stage of the personal finance journey you are on). The average person could likely define an emergency fund with accuracy and without our help. However, they’re used inappropriately more often than not.

How Much Should You Have in Your Emergency Fund?

We recommend saving up at least $2,467 in liquid savings for your emergency fund.

That’s a pretty specific number, right!? Well, we picked it because economists have found that having exactly $2,467 in your savings account is a helpful baseline that will allow you to cover most emergencies. We think that’s a pretty helpful starting goal to have.

That being said, what about larger emergencies? Like losing your job suddenly or heading to the emergency room and having to pay a $7,000 insurance deductible? After you’ve saved up the basic amount and are taking advantage of other low hanging financial tasks, we recommend beefing up your emergency fund so that you have about 3-6 months of living expenses on hand.

What Should Emergency Funds Cover?

As the name suggests, your emergency fund should be tapped into only for emergencies! The definition varies slightly from person to person, but in general these are financial surprises that pop up out of nowhere and things you can’t budget ahead for.

Examples of when it’s appropriate to use an emergency fund:

- Paying medical bills

- Unforeseeable home repairs

- Insurance deductibles

- Temporarily replacing income

- Pet emergency expenses

Real life example: My friend in Texas had a huge wind storm in his neighborhood recently and a big tree on his property fell over, ruining his yard and part of a fence. The mess wasn’t quite large enough for an insurance claim, but it cost him $600 (in cash!) to pay a fencing crew to come and clean up the mess.

Luckily, he had a healthy emergency fund and was able to hit the bank and withdraw 6 x $100 bills without impacting any of his other finances. His emergency fund did what it was supposed to do.

Misuse Of Emergency Funds

A frequent misconception of how emergency funds are intended to be used includes purchases that aren’t really emergencies. Instead, they’re often used for purchases that can be planned and budgeted for.

Some of the most noteworthy but unworthy uses of an emergency fund include:

- Down payments

- Capitalizing on “a deal”

- Paying routine bills

- Vacations

- Upgrading things that don’t actually need replacing

Real life example: One of my friends found an amazing vacation package online. Although it was a killer deal (it was only $1,700 when usually a travel package like that would cost $4,000!) he didn’t really need to buy it. My friend took from his emergency savings to pay for it, and completely wiped out his emergency fund. Kind of risky, as now he has no money left for actual emergencies!

Before Saving, Consider Tackling Debts First

Before you create a 3-6 month emergency fund, it’s important to assess your existing debt. We aren’t referring to your mortgage or student loans (we’d refer to those as good debt vs. bad debt). We’re talking about real, high-interest debts with a rate greater than 6%.

Removing these types of debts before building up an emergency fund beyond that $2,467 amount is an essential stepping stone in the wealth-building phase of life. By paying off your high-interest debts first, you’re essentially saving money you otherwise would have forfeited in interest. Holding onto high-interest debt is like being stuck in a really fast revolving door – it’s difficult to get out of.

Related: Debt Avalanche vs. Debt Snowball payoff methods explained

4 Ways To Build an Emergency Fund

Everybody has different income levels, expenses and savings potential. It’s important to build your emergency fund the way that works best for YOU. Here are a few different methods…

1. Incremental Savings

The most obvious and traditional way is to build the savings into your budget. Each month set aside $100 (or more) to stash away in your savings account that holds your emergency fund dollars. Set a realistic amount. The higher you aim, the better! If $100 per month sounds too difficult, chalk it up to $25 each week! Anyone should be able to find an extra $25 a week.

If you still aren’t able to reach your target goal, consider paying yourself first, then using what’s left to budget for your monthly expenses. Setting an automatic transfer as soon as your paycheck hits is a great way to move the money out of sight, out of mind.

If you can manage to save $100 every month you’ll have a solid $1,200 foundation in just a single year. (That’s a great start… but wait! What if you can do this, and implement some of these additional saving methods below…?)

Pro tip: Try using the Rule of 173 to estimate how much cutting out little monthly costs in your budget could save you over a decade. You’ll be surprised how quickly things add up!

2. Expedite Savings with a Lump Sum

Almost every middle-class American receives at least one check each year from the government in the form of a tax refund. In 2020 and 2021 combined there were three additional checks (stimulus money) on top of the typical tax refund. This was a major opportunity for the average American to get a head start (or fully fund) their emergency fund. If they were able to stash away a large chunk of those amounts into an emergency fund, we’d be willing to bet their stress levels in comparison to those who didn’t, is exponentially less. Overnight they were able to instantly reduce stress by creating margin in their life.

Luckily, there’s still plenty of opportunity for all of us to capitalize on. Whether it be a tax refund, gift, inheritance, or bonus from your employer, take full advantage when receiving a large sum of money and instantly create margin in your life by saving it in your emergency fund. You’ll be glad you did!

3. Increase Your Income

Fortunately, this option can be easier than it sounds. Increasing your income is completely realistic in just about every situation. The hardest part is figuring out a plan of attack. Increasing your income, even by a tiny amount, and saving the difference straight into your emergency fund is a tried and true way of creating additional margin in your life.

Ask for a raise – Being a solid employee at your job enables you to have open lines of communication with your boss about your salary expectations and requests. Attempt to start the conversations well in advance. Not only does this allow your employer time to consider, but then you have time to prove you are worthy of a raise while it’s fresh on their mind. When asking for a raise, avoid giving an ultimatum unless you’re truly ready to switch jobs. If that’s the case, it’s probably best to already have a job offer or two on the table. Most importantly, be honest with yourself. Ask yourself if you even deserve a raise. If not, (and that’s okay!) there are other options to increase your income!

Start a side hustle – Consider starting a side gig doing something you’re passionate about like flipping sports trading cards, selling baked goods/recipes, or refurbishing old furniture for a profit. The opportunities are endless – especially in this gig-economy! By choosing something you already enjoy doing, you’re more likely to make a sustainable stream of income. If you somehow don’t have any passions, take up gig work on the side like mowing a neighbor’s yard, or driving for a company like DoorDash or Uber. (Although, these are good options to increase your income, be cautious in your approach. Trading time for money may not always be worth it)

4. Decrease your spending

Decreasing your spending should be a constant effort that remains at the forefront of your mind. The concept is simple. The less you spend, the more you save. We aren’t implying you should deprive yourself of your craft beer equivalent – the line item in your budget that brings you tons of joy. However, making a couple of sacrifices so you can accelerate the accumulation of a healthy e-fund shouldn’t be off the table.

Reduce recurring expenses – First, look for recurring ways you can save in your monthly budget. Search for a new insurance policy. Explore switching phone plans. Consider if becoming a one-car family is feasible. Evaluate your monthly subscriptions, gas and electricity bills. All these options can be a great start to decreasing your recurring expenses. It’ll become an oddly satisfying challenge!

Make a sacrifice – After you’ve evaluated the recurring expenses, it’s time to ponder if cutting back on your craft beer equivalent is worth creating margin in your life by beefing up your emergency fund. This option doesn’t require you to completely rid yourself of every single ounce of joy. Always find a way to bring value to your life, but find cheaper alternatives. If you like drinking craft beer, for example, consider an inexpensive (but still delicious) IPA instead of the barrel-aged stout. Regardless, it’s still beer! This option of decreasing your expenses will solely rely on your priorities and the actions you choose to take.

Where to Keep Your Emergency Fund

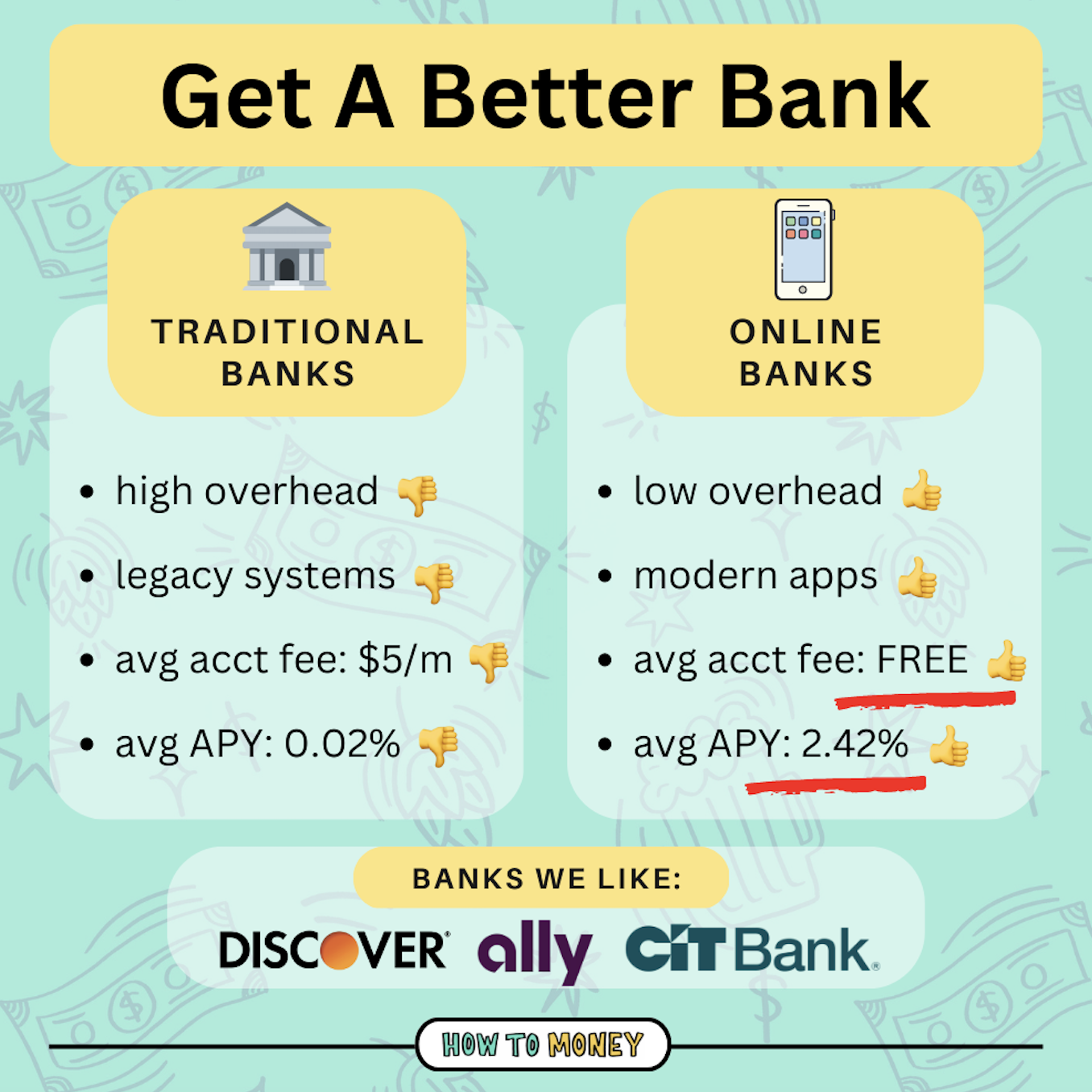

As you start smashing your savings goals, you need a vehicle for your emergency fund. We recommend ditching your traditional bank and replacing it with a high interest, online savings bank. We like accounts offered by Ally, CIT, or Discover. These types of banks have the same abilities as their traditional counterparts but come with fewer fees and more perks!

One of the greatest perks is that you can earn upward of 4% on any money tucked away in your emergency fund. You’d be lucky to find a traditional bank that pays anything more than .02% on any of their savings accounts!

Keeping emergency funds in a high interest, online savings account is a perfect choice. Not only do you have immediate access (penalty free) when an emergency does arrive, but you’re also allowing your contributions to work for you. It’s always a great feeling when your money is making money!

The Bottom Line:

Reading about emergency funds is simple. Taking action and implementing a plan requires a little more effort.

Start by creating a savings goal and outlining actions that you need to take each day to successfully help you to achieve the goal. If you put off creating a savings goal, there’s a likely chance you won’t have any margin in your life when you need it most.

Having an emergency fund lets you live life without a weight on your shoulder. It puts you in the driver’s seat. The idea of creating margin and reducing stress in your life doesn’t have to remain an idea. Get started ramping up your savings efforts today!

**Feature pic by Susan Holt Simpson on Unsplash

Related:

- How to calculate your savings rate (one of the most important numbers in personal finance!)

- Sinking funds – what they are and how to use them