Imagine if you had a crystal ball that could look into the future and tell you how rich you are going to be… Wouldn’t that be cool!? Well, believe it or not, there is such a tool available in real life right now – it’s called a personal savings rate, and today we’re gonna show you how to figure it out!

It’s super easy to calculate your savings rate using basic math. In fact, you can even do it after drinking a few Mind Haze IPAs (I will not confirm or deny whether I am drinking one right now while writing this 🤫)

The hard part, however, is facing reality after looking at your savings rate. You could learn that you’re not saving enough money and that you might be on track towards a subpar retirement. Or worse, you might not have enough money to retire at all!

But don’t worry, it’s never too late to change your financial trajectory. After showing you how to calculate your savings rate, we’ll cover the quickest ways to boost it to make sure you meet all your lofty financial goals.

OK, crack a beer, and let’s get started!

What is a savings rate?

Savings = money. Rate = speed. So a savings rate is basically how fast (or slow) you are saving money.

More specifically, a savings rate reveals the percentage of income that is allocated towards savings. Knowing this percentage is the single biggest indicator of how long it will take to save enough for retirement.

The cool thing about working with percentages (instead of dollar figures) is that it evens the playing field for low and high-income workers. You’ve probably heard the phrase “It’s not about how much you earn, it’s about how much you save”. Well, this is exactly why you need to learn to calculate your savings rate. You might have a big-baller salary, but if you have a low savings rate, it means you’re not holding on to much of your moolah at the end of the day!

How to calculate your savings rate

The math formula to calculate your savings rate is [savings / income x 100]. But for all you non-mathy folks, here’s a step-by-step breakdown:

First, grab these two numbers:

- Total amount you saved last month. (Money transferred to retirement accounts like 401k or Roth IRA, as well as any short-term savings accounts)

- Total income you earned in that month. (Paychecks, side hustle money, etc)

Next, you take the savings number and divide it by the income number. It should show as a decimal.

Lastly, multiply that figure by 100. This will turn the decimal into a percentage and that figure is your annual savings rate!

Savings rate examples

John made $70,000 last year at his day job. He also hustled a bit on the weekends which brought in an extra $5k, so his total income for the year was $75,000.

John saved a lot last year, maxing out his Roth IRA with $6,500 and socking away $8,500 into his 401k retirement account. His total savings amount was $15,000.

Savings of $15,000 divided by income of $75,000 equals 0.20. And turning that into a percentage means John’s savings rate for last year was 20%. 🥳 Awesome!

Here’s another example:

Heather made $285,000 last year. Whoa!!! But she bought a fancy new car, took lavish vacations, and didn’t focus on savings much at all. Her total money saved at the end of the year was $15,000.

Savings of $15,000 divided by income of $285,000 equals 0.052, which is a savings rate of 5.2%. 😬

As you can see, although Heather’s income eclipsed John’s income by a significant amount, her savings rate was much lower. If they both repeated these scenarios every single year, Jon would be on track for a healthy retirement, and Heather would not.

Monthly savings rate vs. Annual savings rate

Sometimes, you might want to calculate a particular month’s savings rate, instead of the full year. This comes in handy when you’re knuckling down on savings and want to check in on short-term progress.

To calculate your monthly savings rate, it’s the same math formula, but you use monthly savings and monthly earned income. (Eg. $1,000 saved of a $4,000 income equals a 25% savings rate)

In some months you might have an awesome savings rate, other months you might not. If you have variable income, or even unexpected large expenses one month it can throw your savings rate out of whack.

That’s why calculating your annual savings rate each year is more accurate for long-term projections.

Savings rate variations

Now you know how to calculate your savings rate at a very high level. But as a personal finance enthusiast, you might have some nuanced questions about what to include as income and what to include as savings in the calculations.

Here are a few things to consider that might affect your method of calculation.

Gross income vs. Net income

Should you use your pre-tax income or after-tax income to calculate your savings rate?

For the simplest method, just use your gross income. This is your total income for the year before any deductions or taxes are taken out.

The reason we like this calculation method best is because it’s the most conservative. Meaning, it treats your income tax like an ongoing expense, even though (hopefully) you’ll be in a much lower tax bracket in retirement.

If you do remove the taxes and calculate based on take-home pay only, this will artificially inflate your savings rate. Overestimating your savings could lead to a more lax approach to savings. That could screw you up later when it’s time to retire. So we recommend taking the conservative approach and using gross income.

Or, why not calculate both scenarios and see how you feel? Math is math – just remember not to overestimate your savings.

Including mortgage principal & debt payments?

Another common question is, “should you include mortgage principal when calculating your savings rate?”

Technically, loan payments are “savings” because they reduce the amount of debt you owe and increase your overall net worth. So, if you want to include mortgage principal payments in your savings rate calculation, that’s OK.

But, it’s really important not to glorify mortgage payments. Too many folks fall into the trap of thinking that their house is the best investment they have. Yes, a home is an investment of sorts, but it’s actually not a very good one!

Long story short, you can include loan principal payments as a form of savings, but make sure you have PLENTY of other investments and savings outside of your primary home. You don’t want to become house-poor!

Why savings rates are important

Savings rates are both an indicator of current financial health, as well as a person’s long-term financial trajectory.

Suppose someone has a very low savings rate (let’s say, under 5%), then they’re probably not in a great financial situation right now as they’re living paycheck to paycheck, in real financial danger. Over the long term, having a repeated low savings rate for years on end means not accumulating enough to retire comfortably.

On the flip side, someone with a very healthy savings rate (say 20% or higher) has a lot of wiggle room. They’re actively saving for retirement and living within their means. They’re accruing more options with every paycheck. Socking away 20% of income into retirement accounts can grow into millions over a few decades.

All in all, it’s important to calculate your savings rate regularly. Doing so will make sure you’re on track to retire comfortably, or even have the option of early retirement!

What’s the ideal savings rate for retirement?

Soooo, how much should you be saving from each paycheck towards retirement? What is the ideal savings rate?

Well, this mostly depends on how long you envision yourself working. If you want to retire as soon as possible, you should shoot for the highest savings rate possible. Here’s an awesome calculator if you’re planning for early retirement.

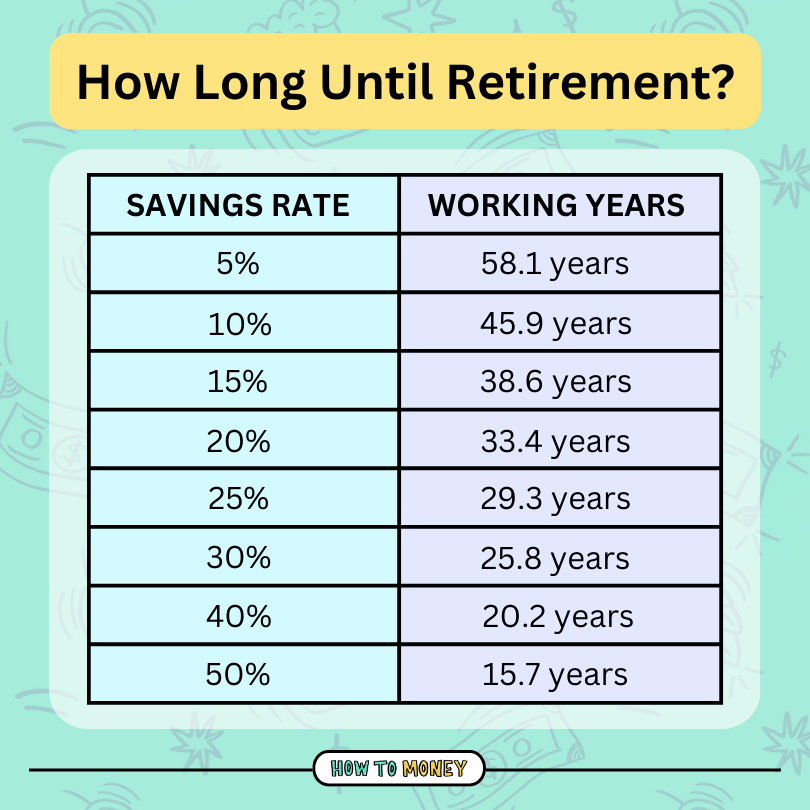

Also here’s a quick table showing how many years you’ll have to work, based on a particular savings rate.

**There are a few assumptions made here, so don’t take all these numbers literally. We assumed starting with $0 savings, earning 6% consistent investment growth, and assuming a 4% withdrawal rate in retirement.**

As you can see, saving 15-20% of your income should be standard practice for most folks shooting for a 35-year career. A higher savings rate means fewer work years (or more retirement money) and a lower savings rate means the opposite.

Keep in mind, personal finance and investing are never linear. Life has its ups and downs! Income can rise or fall significantly throughout your career. People have big years of savings, and years when they might financially struggle, depending on life circumstances. It’s very rare to maintain the same savings rate for decades on end.

But it’s really important to have a goal to shoot for. And the higher the goal, the better. Shoot for the moon, and if you miss, you’ll still end up among the stars.

Average Savings Rates in the USA

You’re probably already aware, but Americans have a big savings problem. Actually, it’s a spending problem! The Bureau of Economic Analysis monitors the savings rates across all US households and publishes the data monthly.

Here is a graph of the average personal savings rate in the USA, going back over 60 years…

Aside from a spike in the Covid years, these savings rates are pretty dismal. And they’ve only gotten worse over time. There’s a noticeable downward trend and our collective savings rate is sub-5% these days. That’s pretty awful!

But, don’t let this chart get you down. You can’t control what average Americans do and how much they save. You can only control what YOU save and spend your money on. That’s why it’s important to calculate and focus on your personal savings rate, not copy what other people around you are doing.

Tips to improve your savings rate

OK, let’s say you’ve just calculated your savings rate and are not pleased with the number you’re looking at. What can you do to turn things around and boost that rate upwards?

Here are a few tips, from better money management to increasing the gap between income and expenses…

Start Budgeting and Expense Tracking

It’s hard to make improvements if you have no idea where your money is going. That’s where tracking your spending and proper budgeting comes in.

If you’re new to budgeting, read this guide on how to start. It’s way simpler than you think.

We always recommend folks start with a basic 50/30/20 budget. This means spending 50% of your income on Needs (rent, food, utilities), 30% on Wants (travel, shopping, subscriptions), and the last 20% for Savings. This is a fantastic recipe for beginner budgeters.

Tracking your spending is also really important. Not only will this keep tabs on where your money goes,but it’ll reveal weak spots and low-hanging fruit you can work on! There’s also a free app called Empower (used to be Personal Capital) That automatically tracks your expenses for you. Try it!

The more you pay attention and tighten the screws on your personal money management, the more your savings rate will improve naturally.

Cut down some expenses

To increase your savings, you’ll need to find areas where you can spend less and pocket that money instead.

The quickest and biggest savings usually come from the biggest expense areas. These are usually housing, cars, food and utilities. Here are some ideas to cut back:

- For housing: Try negotiating your rent. Or, moving to a cheaper place for a while. Another idea is to rent out a room or house hack to lower your living costs.

- For cars: Can you live car-free!? Or downsize the number of cars you have in your household? Here are a handful of ways to reduce auto costs.

- For food costs: Try a no-eating-out challenge! This is when you stop going to restaurants and save all that money instead.

- Cheaper utilities: We’ve written guides on how to save money on gas, electricity, and water.

Once you pare down big expenses, start tackling all the little ways to save money. Remember, it’s not about cutting out all of the fun from your life. It’s about redirecting your dollars to make sure your money gets spent on the most important things!

Increase your income

Cutting expenses can only go so far. So to increase your savings rate even further, you’ll need to look for additional income opportunities.

Most people are afraid to ask for a raise, but it’s the single quickest way to boost your pay. We’ve written a guide on how to negotiate a pay raise here. Check it out! The worst that can happen is they say “no.” But even if that’s the response you haven’t lost anything. Try it!

Switching jobs is also a great way to lock in a higher salary. Consider getting additional training or education, making yourself valuable, and searching carefully so you can land a new more lucrative job within months. Start networking on platforms like LinkedIn and see what opportunities are out there.

Side hustles can also boost your income. Just be careful because it’s not a great long-term solution. Trading time for money doesn’t scale!

Lastly, remember that increasing your income is only helpful if you SAVE that money. If you spend all the extra money you earn, your savings rate actually goes down, not up!

The Bottom Line:

Your personal savings rate is one of the biggest indicators of financial health, so it’s important to know where you stand. The percentage of income you save determines if you’re on track for a healthy retirement, and how many working years you might have left before you reach financial freedom!

If you are not happy with your current savings rate, don’t fret. It’s never too late to change your financial trajectory. Just roll up your sleeves, find a better budgeting system, and look for ways to decrease spending while increasing income. I realize that’s easier said than done, but I promise that all the hard work will pay off. You’ll experience increased margin now and a growing net worth for your future too!

Related posts: