Have you ever gone months without exercising, then suddenly decided that today is the day you are going to get your workout routine together? You head over to that gym you’ve been donating to for the last year, jog 6 miles on the treadmill, attempt to squat your body weight, try out every single machine in the place, and cool down within an hour on the elliptical. Then, you wake up the next morning feeling like you got hit by a double decker bus and don’t return to the gym for another year. Wash, rinse and repeat annually. 🤪

Sometimes, we need to start new habits out slowly simply to ensure that we will be able to sustain them. It turns out, this applies to the act of budgeting, too! If you make it complex from the start, you could struggle to keep up with it. That’s why we recommend the 50/30/20 budget for folks who are new to budgeting. It’s the perfect gateway drug.

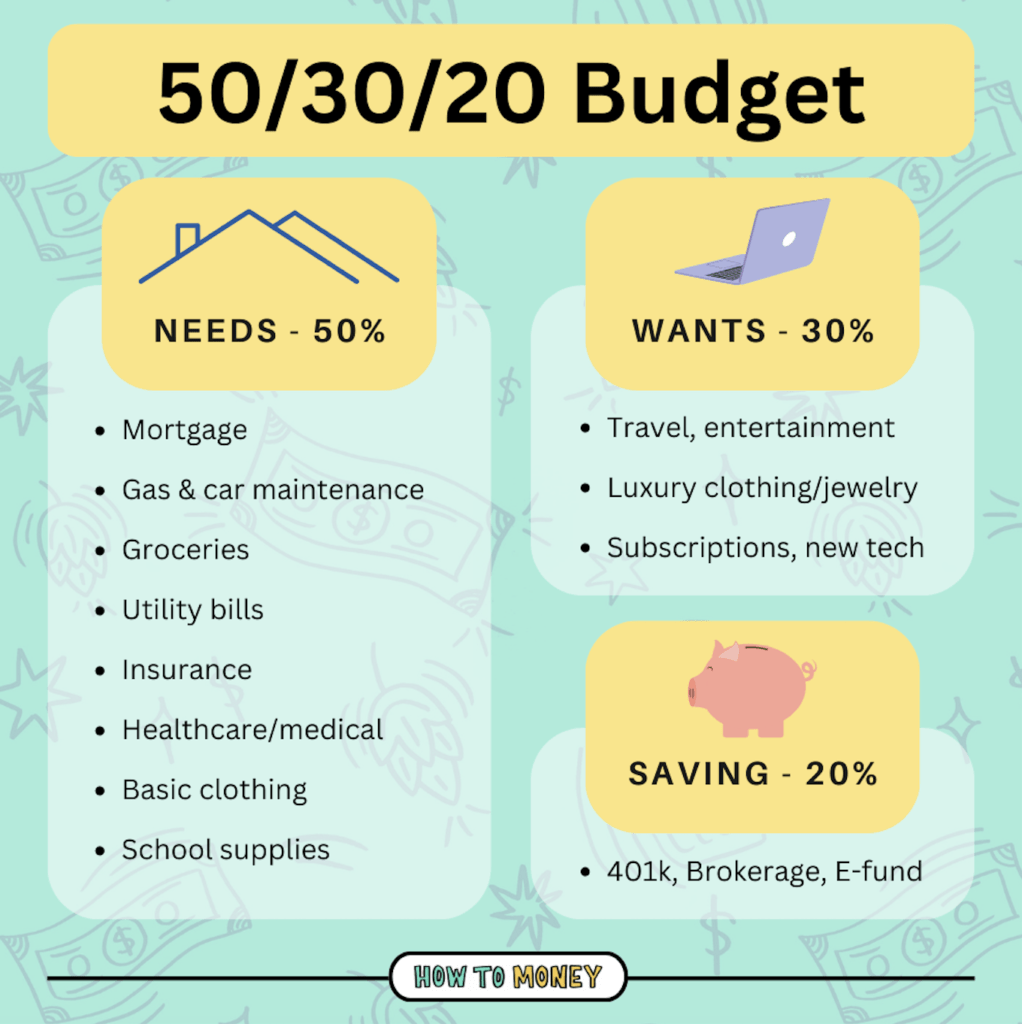

What is the 50/30/20 Budget?

The 50/30/20 budget simplifies the process of budgeting by allowing you to split up your monthly income into three categories; needs, wants and savings. This provides you with helpful guidelines for how much of your money should be spent on each aspect of your life, without needing to get into the nitty gritty of individual categories.

Simply put, the 50/30/20 budget allocates 50% of your post-tax income to needs, 30% to wants, and 20% to savings.

Why we love the 50/30/20 Budget:

There’s a few reasons why we recommend beginners manage their money using the 50/30/20 budget system.

It’s simple

A 50/30/20 budget removes the complexity of splitting expenses into a million different categories. By simply bucketing everything into 3 main categories, it’s much easier and more sustainable for folks who are just getting started managing their finances.

Works with any income

The best thing about budgeting with “percentages” is that the same 50/30/20 budget can be used by anyone, at any income level. Whether you’re a recent college grad making $40k a year, or a CEO making $2 million, the 50/30/20 budget works.

Better yet, as your income grows over time, each budget category gets larger automatically. This means lifestyle inflation is built into the system, and you can spend more on needs, wants, and savings as income changes.

Reminds you that it’s okay to spend on wants

While it’s important to always set aside money for your future, it’s equally as important to spend a little bit of money in the present to brighten your days. A 50/30/20 budget can help to encourage even the most frugal among us to find joy in spending money on the nonessentials that enrich their lives.

It also gives you flexibility to spend on your wants – however you want! I have some friends that allocate their entire ‘wants’ budget to travel, because that’s what they value most.

Makes saving a priority

Another benefit of the 50/30/20 budget is that it ensures that those who stick to it will save 20% of their post-tax income. It’s no secret that most Americans have paltry savings habits. A 50/30/20 budget helps make sure that you don’t become a part of the 53% of Americans who feel like they are significantly behind on saving for retirement.

How to Make a 50/30/20 Budget

So now that we’ve sold you on the magic of the 50/30/20 budget, it’s time to put rubber to the road and create your very own. Here are the simple steps you can follow to create your first 50/30/20 budget.

Step 1: Add up all of your income

In order to make a plan for your money, you need to understand exactly how much cash you have coming in. Start by adding up all your post income paychecks, and be sure to include any extra money coming in from any side hustles.

If you’re managing finances as a couple, you should include both incomes. And if you have variable income month to month, try making an annual budget to start, totalling up all your earnings for the previous 12 months.

Step 2: Look over your expenses

Probably the most important key to successful budgeting is understanding spending habits. Nothing is more discouraging than busting your budget month after month, and that’s exactly what will happen if you budget without tracking your expenses closely.

Start by rounding up all of your credit card and bank statements from the past three or so months. Go month by month and write down each of your transactions under the category of needs, wants, and savings (more on this later). Don’t make any sudden judgments. This exercise is just to see what you’re already spending on each category every month. Once you’ve got this down, you’re ready to create your own 50/30/20 budget.

Step 3: Budget 50% for Needs

First, let’s tackle the needs section of the 50/30/20 budget. It’s as easy as dividing your income in half. That’s how much you’re going to budget for your biggest essentials.

Here are a few examples of things that fall into the needs category:

- Food

- Shelter

- Utilities (gas, water, electric and BASIC internet & phone service)

- Insurance

- Transportation

- Minimum debt payments

Basically, if you can’t live a healthy existence without it, it should be in the needs category.

Next, compare that list of your current expenses to see how it stacks up against 50% of your monthly income.

What if my expenses are higher than 50% of my income?

If your expenses are higher than 50% of your income, you’ll need to make some life adjustments. You can either lower your living expenses, increase your income, or work towards doing BOTH.

First, take a look at your monthly bills. You’d be surprised at how many of our monthly expenses are actually negotiable Call up your insurance, phone, and internet providers and ask them if they have any new customer promotions you can take advantage of. Negotiating your bills is the easiest step you can take to start getting your expenses down.

In the same vein, it’s a good idea to take measures on your own end to reduce the amount of money you shell out on bills. Taking simple steps towards reducing your water, electricity, gas, and grocery bills can save you hundreds, if not thousands, of dollars every year!

You can also help bridge that gap by looking for ways to increase your income. Consider asking for a raise, or creating a side hustle to bring in extra cash each month.

Consider taking drastic measures

If a few tweaks won’t get your living expenses below 50%, you might be living beyond your means. You might even want to consider making a major change to get those expenses below the 50% mark. Trust me, it will make your money life easier going forward if you set yourself up to live below your means.

Sometimes getting the big stuff right means you don’t need to sweat the small purchases as much. Here are a few drastic changes to consider making in order to reduce those needs to be less than 50% of your budget.

- Downsizing your home or apartment

- Moving to a cheaper area

- House hacking

- Getting roommates

- Ditching your car

- Switching jobs

- Switching career industries altogether

What if my expenses are below 50% of my income?

If your spending on essentials is less than 50% of your income, that’s a great problem to have! This means any money left in that category can be reallocated at the end of the month towards your savings and/or your wants. You might want extra craft beers, a fancy family vacation, or perhaps opt for a higher savings rate. If you save fast enough, you might even be able to retire early!

I recommend using some of that extra money to bolster emergency savings and any sinking funds for irregular expenses. Setting aside some extra cash for things like car maintenance, new tires, and holiday gifts can help you to avoid dipping into your long-term savings.

Step 4: Budget 30% for Wants

Now that you’ve gotten the boring necessities out of the way, it’s time to have some fun with your budget. Let’s talk about your wants…

Your wants should include things you don’t need to survive, but that enrich your life. Under the 50/30/20 budget, you can allocate 30% of your monthly income to your wants. Things that fall into this category can include, but are not limited to the following:

- Entertainment

- Takeout/restaurants

- Travel/vacations

- Gifts

- Beauty/clothes

- Hobbies

- New technology

- Newer cars/luxury transportation

How to make the most out of this 30%

If you spend your 30% mindlessly, you may feel like it’s never enough. To really make the most of your discretionary budget, get in touch with your values. It’s easy to let your budget trickle out by spending throughout the month on little treats and takeout (and if that’s important to you, more power to you!), but it takes a little more intentionality to spend in a way that will actually make you happy.

For example, if you’re obsessed with your knitting hobby, you’ll probably find it more fulfilling to spend your money on sick new yarn than grabbing takeout on the way home because you didn’t prepare for your late night at work. Work on developing mindful spending habits to fully enjoy what that 30% can bring to your life!

Remember that if you have certain wants that you need to save up for, for example saving up for a vacation, or a pricey new instrument, you can set aside some of your “want money” and create short-term savings buckets. That way you can save up ahead of time for those purchases. You don’t need to fully spend your 30% each and every month.

What if my wants add up to more than 30%?

If you’re spending more than 30% of your budget on luxuries, you’ll need to reel it quickly. Try implementing mindful spending techniques, like creating a 24-hour waitlist, or preparing ahead of time for emotional spending triggers.

You can also work to find free or cheap alternatives to your favorite activities. For example, if going out weekly with your friends is killing your entertainment budget, consider getting together at each other’s homes and chatting over a couple of beers. Instead of going out for coffee, make coffee at home and go out on your local walking path. Swap your weekly dinner reservation with one of these 30 cheap date ideas, and consider even picking up one of these 15 frugal hobbies!

What if my wants are less than 30%?

If you feel fulfilled and you’re spending less than 30% of your income on wants, that’s awesome! Feel free to find ways to splurge a little more, and usher some of that extra money towards your biggest savings goals.

Step 5: Budget 20% for Savings

Arguably, this is the most important section of the 50/30/20 budget. In fact, if you subscribe to the pay yourself first mentality, you should begin with this section and prioritize it!

Saving 20% of your income is non-negotiable. This is essential in ensuring you’ll have enough money to weather emergencies, achieve your biggest savings goals, and be able to retire comfortably. Your savings category can include:

- Long-term savings for assets that will appreciate or earn you money (ex. Real estate, higher education, saving to start a business)

- Retirement investing (401ks, IRAs, HSAs, TSPs, etc)

- Debt payoff

The best way to make sure you’re consistently saving 20% of your monthly income is to automate it! Automating your finances is a great way to meet your money goals without needing to physically go and transfer those savings to your various accounts each and every month. If you have a workplace 401k, this is a great way to sock money away each paycheck without even thinking about it.

We also recommend setting up an automatic transfer to other retirement accounts, like your Traditional or Roth IRA, as well as a transfer to your high yield savings account. You can also set up automatic debt payments to ensure you’re attacking your most nefarious debts every month.

What if I’m saving more than 20%?

That’s absolutely badass. Have you ever considered whether or not early retirement might be for you? The higher your savings rate, the less work years are needed to reach your retirement number. You’re radically reducing the time it’ll take to reach financial independence.

Another thought: If you have a high savings rate, perhaps you want to explore the world of charitable giving, like through a donor advised fund?

Step 6: Make it as simple or complex as you want

When it comes to the 50/30/20 budget, it’s totally up to you on managing it. So you can take it as relaxed or as serious as you want. For simplicity, you can operate your budget off the three categories alone. Or to drill down a bit further and focus on specific spending patterns, you might want to create subcategories.

For example, you might break up your needs category into rent, utilities, transportation, insurance and food. This can help you to get a better idea of where you want your money to go each month. Here is an example of how you might choose to further break down your 50/30/20 budget:

Needs (50%):

- Rent

- Utilities

- Transportation

- Insurance

- Food

Wants (30%):

- Restaurants

- Clothes

- Vacation

- Hobbies

- Gifts

Savings (20%):

- Home savings

- Roth IRA

- Credit Card Payoff

Step 7: Check in regularly

Now that you’ve created your 50/30/20 budget, it’s time to use it and create a sustainable system. This means checking in with your budget regularly (at least once a month) as you earn and spend money. Monthly maintenance lets you course correct and catch any errors before they derail your finances completely.

I recommend checking in with your budget at the end of each week at first as you adjust your spending habits. Scroll through your credit card purchases, look through any receipts, and subtract the money you’ve spent to see what you’re left with for the rest of the month.

Related: How to fix a failing budget

Step 8: Reset it at the end of the month

Once you reach the end of the month, it’s time to “reset” your budget. Think about what went well the previous month, and what needed a little bit of work. Feel free to make small adjustments to your amounts, and try to anticipate any upcoming expenses. Then, work these into your budget and repeat month over month!

Pro tip- Make your budget night fun by ordering takeout from your favorite place, or by enjoying your favorite drink while you go over it. Instead of dreading it as a boring task, make it something to look forward to!

50/30/20 Example With Numbers:

Here’s an example of what two real 50/30/20 budgets might look like:

50/30/20 Budget: Level 1

Ariel works as a teacher and makes $6,500 every month after tax. She divides up her income and builds her 50/30/20 budget as such:

Needs (50%): $3,250

Wants (30%): $1,950

Savings (20%): $1,300

Each month, she subtracts expenses from each of these categories, and decides what she would like to do with her savings.

50/30/20 Budget: Level 2

Gina makes $4,000 each month after tax. She calculates her budget to be as such:

Needs (50%): $2,000

Wants (30%): $1,200

Savings (20%): $800

She decides to take it a step further by estimating how much she will spend on certain expenses within these categories.

Needs (50%): $2,000

- Rent: $800

- Food: $400

- Transportation: $200

- Insurance: $250

- Internet: $70

- Phone: $25

- Utilities: $100

- Car maintenance sinking fund: $50

- Emergency fund: $105 (plus anything left over from her needs category)

Wants (30%): $1,200

- Travel: $400

- Restaurants: $200

- Gifts: $100

- Hobbies: $250

- Misc: $250

Savings (20%): $800

- Home down payment savings: $400

- Roth IRA: $400

50/30/20 Budget FAQ

When trying a new budgeting method, there’s sure to be a learning curve. Here are a few of the most frequently asked questions about the 50/30/20 budget.

Are there any downsides of the 50/30/20 budget?

While there are tons of benefits to utilizing a 50/30/20 budget, there are certainly downsides as well. Its lack of specificity comes to mind as something that could potentially hurt you in the short term. You may find that you’re spending money on things that don’t align with your values, or that you’re lacking the proper planning to really attack those big ticket money goals. This is why we recommend this method for those just starting to get their money game together.

Another possible downside is that it can be quite rigid. Its strict rules can be tricky to adhere to if you live in a high cost of living area. If that’s the case, and you can’t get your needs to be under 50%, you can feel free to adjust the rule to suit your individual situation. Just make sure you continue to save 20% of your income each and every month.

How should I actually make my budget?

You can make your 50/30/20 budget however you like! Whether you prefer to go old school with pencil and paper, use spreadsheets, or fancy software like YNAB, you can manage your budget in whatever way you prefer.

What if your income varies?

Budgeting with variable income can be more difficult than if you get paid on a regular basis. For example, if you are a freelancer, you may have dry spells and then high-earning months. That can make it more difficult to budget effectively.

What we would recommend is to try and build up enough savings that you can keep your budget relatively the same each month. That way you don’t need to make massive changes to your budget constantly. Find your average monthly income and budget based on that. Whenever you make more money than your average, stash it away for those months when you make less – like a squirrel storing up acorns for Winter. Remember that it’s even more important to have a well funded emergency fund for freelancers as well.

In the meantime, as you save up a cash cushion, consider budgeting for the coming month with the money you made last month. This can help you to avoid budgeting with money you haven’t earned yet.

Bonus– make sure to check out these 11 Money Tips for Freelancers and Gig Workers!

What other budgeting methods are there?

If the 50/30/20 budget doesn’t sound like your cup of tea, don’t worry! There are plenty of other budgeting methods you can try. Here are just a few:

The Zero Based Budget:

Under this budgeting method, every dollar is given a specific job. This is great for money nerds, those with smaller incomes, or anyone who wants to accomplish major money goals.

Cash Envelopes:

Using this budgeting method, you’ll put cash for each line item in your budget into an envelope. Then, wherever you go shopping, you’ll bring the physical envelope with you. This is a great budgeting method for those who struggle with overspending, because once the money in the envelope is gone, that’s it!

Mix & Match Budget:

If no particular budgeting method is speaking to you, not all is lost. You can pick and choose elements you like from each budgeting method to create something that works best for you. Just make sure you continue to save at least 20% of your income each month.

Is the 50/30/20 budget before or after taxes?

When you make your 50/30/20 budget, you’ll do so with your after tax income.

I’m super frugal… Do I still need a budget?

Even if you’re super frugal, budgeting is still important. Sometimes, it can even help ultra frugalites to loosen up and spend a little bit more. Remember, no day is promised, so it’s important to also spend some money in the present in ways that will enrich your life.

The Bottom Line:

The 50/30/20 budget is a great method for beginners just starting to take control of their finances. Its simplicity makes it easy to maintain, and it allows folks everywhere along the socioeconomic spectrum to save for retirement, no matter the income level.

Budgeting with the 50/30/20 method is also super flexible, and can be modified to include sub categories as needed. Overall, we would recommend it to anyone who wants to stop living paycheck to paycheck and start building wealth for the future.

Related Posts: