There are tons of different ways to make money, and people choose different career paths in order to suit their particular interests and lifestyles. Whether you work a traditional full-time job, own your own business, or are self employed, you can live an enriching life and crush your money game.

Most traditional money advice caters to those working a 9-5, or to folks with consistent income. However, a recent study shows that 34% of workers in the U.S. are freelancing in some capacity. So today, we’re going to dive into some of the best money tips for freelancers to help you thrive financially.

Benefits of Self Employment

Being your own boss certainly comes with some perks! Perhaps the greatest benefit to freelance work is having more of a say over when you’re working. If you hate working in the afternoons, you can wake up early and end your day early. If you do your best problem solving during the night shift, hey, why not go full nocturnal?

You also have the ability to set how much you charge for your services, and can increase your rates as you see fit throughout your freelancing journey. Being your own boss can allow you more control over what projects you pursue, and in some cases can give you more of an ability to follow your passions.

Drawbacks of Self Employment

Like anything else, working for yourself also has some considerable drawbacks.

Remember that time freedom I mentioned earlier? Well, some people find it increasingly difficult to separate their work lives and personal lives when they take the plunge into self employment. Because you’re the boss, the responsibility to find and keep work falls directly on you. Some folks find themselves working all day, rarely able to disconnect from their jobs.

Freelancing also comes with some financial repercussions as well. While you have the ability to charge what you like, your income can be less predictable. And, you’re on your own when it comes to saving for your retirement. Plus, you’ll have to pay your own “employer taxes.” More on that later…

11 Money Tips for Freelancers and Gig Workers

While freelancing may not be for everyone, there are some steps you can take to make it easier and more profitable. Here are 10 important money tips to live by if you’re self employed!

1. Open Your Own Retirement Accounts

If you don’t have a traditional employer, saving for retirement falls entirely in your hands. That’s why you’re going to want to open up your own retirement funds with a low cost provider like Vanguard or Fidelity.

A good place to start is to open either a Traditional or a Roth IRA. Each year, you can contribute up to $6,500. Both have their own unique tax advantages that you can take advantage of.

A Traditional IRA allows you to contribute pre-tax dollars, which can help you to lower this year’s adjusted gross income. Then, you pay taxes when you withdraw your contributions in retirement.

For a Roth IRA, you pay tax on those dollars now, and in retirement you can withdraw your money tax free!

A Solo 401k is another awesome option for folks with freelance income. And because you act as the administrator of your own 401k, you get to set the contribution and matching benefits, etc. Here’s a guide to various Solo 401k options – many of the big brokers offer them with no fees!

There are a couple other options for retirement accounts if you want to contribute more in a single year. For more information, you can check out these Retirement Plans for Self-Employed People.

Whatever accounts you settle on, what’s important is that you commit to contributing a certain amount or percentage of your income each month and stick to it!

2. Get One Month Ahead

Budgeting can present some challenges when your income varies, so a good way around that is to get one month ahead. That way, you’re budgeting for the coming month with money earned last month.

If you’re living paycheck to paycheck, we understand that this is a difficult task. However, with some clever budgeting and a little patience, this is totally something that you can accomplish over time.

When you’re trying to get ahead, focusing on cutting a few of your expenses could provide some margin in your budget. Try shopping around for your utilities and insurance, or negotiating your bills.

Then, figure out which budgeting method you would like to use. There are a bunch to choose from, and they all come with their own unique benefit for different budgeting personalities. You can also try using budgeting apps like Credit Karma or You Need A Budget. These can cut down on a lot of the manual work needed to keep track of your spending.

Related: How to budget with irregular income & 5 Best Mint Alternatives to Try

3. Beef Up Your Emergency Fund

When you’re self employed, some months are better financially than others. If you want to avoid having to survive on rice, beans and ramen during your leaner months, it’s important to build up a pretty sizable cash cushion to keep you covered.

An emergency fund is a stash of money that you reserve for those occasions you can’t really plan for like surprise medical expenses, a hefty car repair or loss of income. Having a good amount of cash in your e-fund prevents you from having to rely on credit cards or other forms of debt when you’re struck with some poor luck.

Typically, most advice recommends that you save up about 3-6 months worth of living expenses. But if your income varies, you might want to consider saving up even more. Amassing 6-12 months worth of expenses can help if you have an unpredictable income. This can allow you to get by without too much difficulty should you lose a client or struggle to find more work.

Pro tip: Try one of these fun money saving challenges to kick start your emergency fund!

4. Pay Yourself First

We’ve all had months where we intended to save a hefty chunk of change, but find ourselves with very little left over at the end of the month. That’s why it’s so important to pay yourself first. It’s one of the best financial habits wealthy people practice.

Transferring money to your savings and investment accounts can make you more aware of your spending. If you’re left to get through the rest of the month with only enough to cover the expenses you budgeted for, you’re less likely to overspend and dip into those savings! You’re also likely to make an effort to lower your variable expenses.

Commit to putting a certain percent of your income into your savings and retirement accounts before you spend on anything non-essential. No one else is going to do it for you.

Related: Easy ways to automate your savings

5. Open Up A High Yield Savings Account

So now that you’ve sacked away all your cash, you might be wondering where you should stash it. One of the best places to keep your cash cushion is in a High Yield Savings Account.

A High Yield Savings Account can help you save on some of the ridiculous fees that the big banks still charge, while earning between 10-12 times the national average in interest!

Earning 3-4% on your savings is nothing to scoff at. In a single year, if you left $20,000 in a high yield savings account with a 4% APY, you could earn an extra $800 in interest. Leave that balance for ten years, and that’s $9,604 you didn’t have to trade your time for.

Putting your money in an HYSA is a great way to hedge against inflation, and keep more of your money. Here’s a post all about switching banks and how to do it.

6. Get Your Own Health Insurance

In the U.S., often our health insurance is tied to our employment. One of the benefits of getting a 9-5 job is that it typically comes with benefits, like employer sponsored retirement funds and you guessed it, health insurance.

Health insurance can be pricey, and having to supply your own can be one of the things that makes it more difficult to pursue freelancing. However, even though the options out there for self employed individuals aren’t great, it’s so important that you don’t skip out on it. The number one reason for personal bankruptcy is medical bills. So it’s important that you find a way to have a healthcare plan.

The best case scenario is that your spouse or partner has health insurance through an employer that you can join. But if not, there are still a few options for affordable healthcare.

Likely, the cheapest option could be to get insurance through healthcare.gov. Many people qualify for tax credits which come in the form of a monthly discount. Another option is to look into a healthcare sharing plan.

Health sharing plans are not insurance, but they do function similarly. Health sharing plans are typically made up of a group who share ethical or religious beliefs. They band together to facilitate the sharing of healthcare costs. These organizations won’t be for everyone, as they don’t cover all things (like maternity leave). There are also some limits for pre-existing conditions. So be sure to do your own research. You can read Matt’s Medi-Share review here.

7. Plan Ahead For Tax Season

An unfortunate truth about freelancing is that filing your taxes can be more complicated. Since you don’t have an employer withholding taxes for you, you could be on the hook for lots of money at the end of the year if you aren’t careful. That’s why it’s so important that you prepare for tax season all year round.

There’s a lot to cover here, so make sure you do your own research and consult with a tax professional if necessary.

Plan for Self Employment Tax:

Now that you’re your own boss, you’ll have to pay self employment tax, which is 15.3% of your net earnings. 12.4% goes to social security and 2.9% goes to medicare. The good news is that you can use up to half of it as a deduction for your income taxes!

Make Quarterly Estimated Tax Payments

To avoid having to pay a hefty lump sum of taxes at the end of the year (and to avoid penalties) it’s a good idea to make four quarterly estimated tax payments throughout the year.

Estimated taxes are due every on the following dates for 2023:

April 18th, 2023 (Taxes for January-March)

June 15th, 2023 (Taxes for April-May)

September 15th, 2023 (Taxes for June-August)

January 16th, 2024 (Taxes for September-December)

Predicting your estimated taxes isn’t always difficult. If you predict that your income for this year will be similar to your income from last year, just divide your tax liability from last year by 4 to come up with the amount for your quarterly payments.

However, if you expect to have a particularly good or bad year, you’ll have to make these payments by crunching the numbers on how much money you predict you will make. It’s a good idea to err on the side of caution. If you end up overpaying, you’ll get money back when you file your tax return. But when in doubt, it’s a good idea to speak to a tax professional.

As a general rule of thumb, I like to set aside at least 30% of my income for tax season. At worst, you’ll be prepared. And at best, you’ll have an extra lump sum saved up that you would have spent!

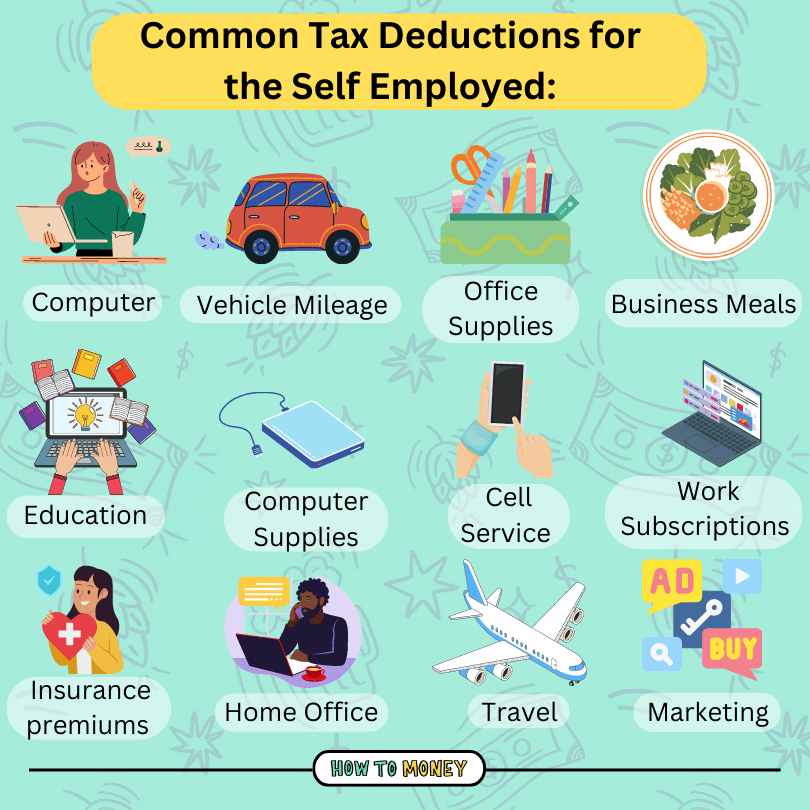

8. Actually Understand “Write Offs”

One of the biggest mistakes that self employed workers make is not understanding tax write-offs.

No, the government doesn’t pay for your business expenses. And you probably can’t write off your vacation to Tahiti because you answered a work email while you were away…

Write offs are qualifying business expenses that can lower your taxable income.

For example, if you spend $50 on office supplies, you wouldn’t just pay $50 less in taxes. Instead, the $50 would be subtracted from your income. So if you make $50,000 in a year, you would only be taxed on $49,950.

As a self-employed person or independent contractor, you can deduct a ton of expenses if they’re used for work, including your internet, your laptop, office supplies and mileage. Just make sure to save your receipts and keep good records.

If you have a lot of deductions, it may be worth it to hire a tax professional. Or, do some extensive research about what you can and cannot deduct. Certain expenses, like laptops or printers might need to be treated as depreciating assets. This might mean that you cannot deduct the full price at once.

Not all deductions are available for all freelancers. It’s extremely important to only claim the expenses you are eligible for. The IRS doesn’t take kindly to those who fluff their tax filings!

9. Get a Business Credit Card

Speaking of business expenses, a cool perk of being a freelancer is that you’re eligible for business credit cards. These cards might offer you better rewards or cash back opportunities (as long as you follow the best practices for responsible usage!)

Also, having all your business expenses on a separate credit card from your personal card makes it much easier for accounting and tax records. While there’s no law against putting your business expenses on a personal card (and vice versa), it’s definitely a more organized ways to run your business.

Don’t have an EIN? No problem! When you fill out a business credit card application, just input your personal name in the business name section, and your SSN in the EIN section. Here’s a full post we wrote about the best credit cards for side hustles and freelancers.

10. Choose A Gig You Can Scale

If freelancing is going to be your main source of income, it’s a good idea to choose a field that is going to be sustainable, and even scalable.

Unfortunately, while driving for Uber and Lyft can be a great way to make some cash for short term goals, putting extra mileage on your car could cause problems down the road. Another downside is that you don’t have a say in how much you charge. This can make it impossible to scale over time.

Instead, try opting for a field where your pay will correlate to your experience. For example, if you become a freelance photographer, you can increase your rates over time as demand for your services increases.

If you’re wondering what freelancing skills are in high demand in today’s market, be sure to check out our post, “These Freelance Skills Are In High Demand.”

11. Come Up With Your Hourly Rate

Have you ever accepted a project for a fixed amount, then crunched the numbers on the hours you worked to realize you made less than minimum wage? 🤯

The truth is, not all gigs are worth saying yes to. And part of working smart as a freelancer is learning when to say no to a project.

A great way to make sure that a jobs are worth your time is to come up with your hourly rate. An easy way to calculate this is to take the amount of money you typically make in a year, and divide it by the number of hours you plan to work (2,000 hours if you plan to work about 40 hours each week and take two weeks off).

For example, if you make about $60,000 each year and work about 2,000 hours, your hourly rate would be $30 per hour.

Then, if you’re presented with an opportunity to work on a project, you divide the pay up by the amount of hours you predict it will take you and see how that stacks up against your hourly rate.

Now I get it, sometimes when you’re starting out you have to take lower paying jobs. It might be the only way to build your clientele or a portfolio. Or, you might want to say yes to a passion product even if the rate is a little bit lower. However, knowing your hourly rate can help you to make an informed decision as to whether or not a gig is worth it.

The Bottom Line:

Whether you freelance or work as an independent contractor, being self employed means paying special attention to your money management. However, many people find it to be a fulfilling way to enjoy life now while saving and investing for the future.

We hope you find these money tips for freelancers helpful! Be sure to check out these related posts and podcast episodes for even more money advice for the self employed.

Related Posts: