Advertiser Disclosure

* Advertiser Disclosure: How to Money has partnered with CardRatings for our coverage of credit card products. How to Money and CardRatings may receive a commission from card issuers. Some or all of the card offers that appear on the website are from advertisers. Compensation may impact on how and where card products appear on the site. Lastly, the site does not include all card companies or all available card offers.

Credit cards… Everyone in the personal finance space has a different opinion of them.

While certain finance gurus loathe them, and have even gone as far as to label them “I love debt cards” (not naming names 😅), we like to take a more nuanced approach to credit cards.

Overlooked Credit Card Benefits

The truth is, credit cards are a tool. And like any tool, credit cards can be used in a way that can have both a positive or negative impact on your life. However, when used correctly, credit cards can provide you with a ton of benefits and help you to get ahead in your finances. That’s why in this post, we’re going to discuss the amazing credit card benefits you aren’t using!

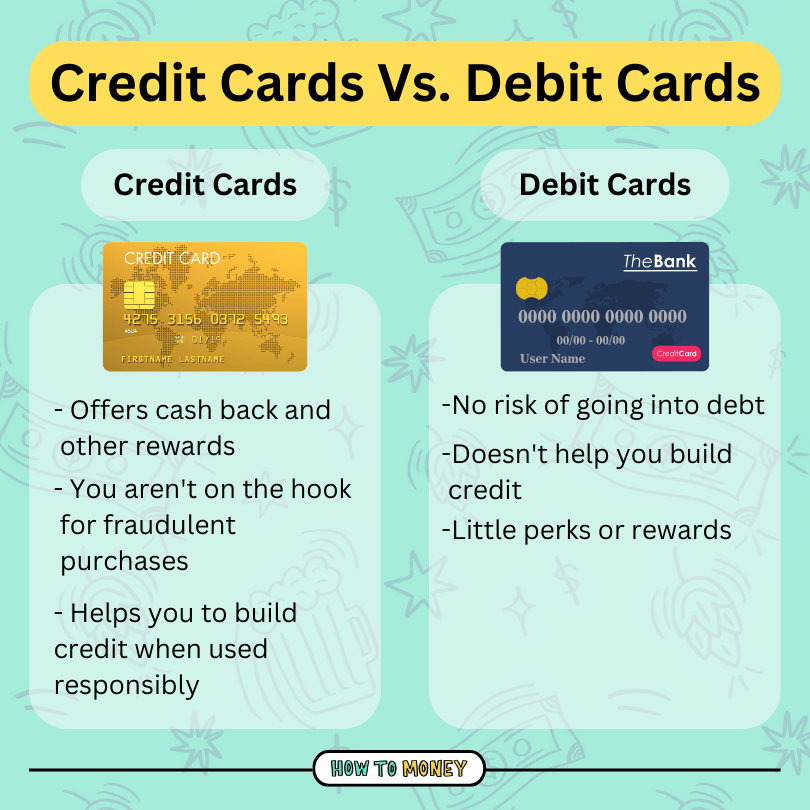

Credit Cards vs. Debit Cards

Credit cards and debit cards might look the same. But only one of them can provide you with fraud protection, help you to build credit, and shower you in cash back and rewards…

If you struggle with overspending, it may be best to stick to a debit card. The biggest benefit is that you’re generally prevented from spending more than you have in your bank account (unless your bank allows for overdraft- which can leave you hit you with tons of punitive fees!).

Since the money exits your accounts when you make a purchase, you’re also prevented from being faced with the interest that comes when you don’t pay off a credit card in full each month. If you’re someone who has had issues with overspending, or getting into credit card debt in the past, feel free to stick to debit cards if you feel like that’s what you need to do! Remember- you know yourself best, and personal finance is personal.

However, if you feel confident and have good financial habits, credit cards can bring a ton of value to your life. On top of the extra cash that can come from credit card rewards, they often offer you protections from fraud, travel perks and extended warranties.

But remember that these perks are only worth it if you’re able to use credit cards responsibly. That means paying them off in full every. single. month. If you’re hit with interest, it more than negates all the value of those rewards you’re earning along the way.

Debit cards are sort of like credit cards’ less cool cousin. They just don’t do much. Yes, you can use them to make purchases, but you’re likely missing out on some amazing credit card benefits. Why leave them on the table?

Common Credit Card Benefits:

Having a credit card and only using it to make purchases is like having a smartphone and only using it to make calls. You’d be missing out on other awesome features and not be getting as much value from your device as you could be.

That’s why it’s definitely worth it to take a bit of time to read up on all of the benefits that your credit cards have to offer. You can even call the company to ask if they offer any of the following benefits for your specific card.

1. Fraud Protection

One of the biggest reasons we recommend using a credit card to make purchases over a debit card is because the fraud protection offered for debit cards is dismal at best.

If someone else uses your debit card to make purchases, that money is already out of your account. Which means that you have to fight with the bank for them to give you that money back. But if that purchase was done on a credit card, you’re only working to get a charge reversed, which can be much easier.

If fraudulent charges are made with your debit card, you had better hope you catch it early. Caught within two days, the most you could be on the hook for is up to $50. Which kind of sucks considering you were the victim of a crime. If you report it after two days, but before 60 days have passed, you could be liable for $500 in charges. After that, you could be on the hook for the entire amount! 🤯

Credit cards offer much better fraud protection. Thanks to the Fair Credit Billing Act, in the event your information is stolen, you won’t be liable for any purchases you didn’t make.

2. Help You Build Credit

Another great benefit of credit cards is that when used properly, they can help to improve your credit score.

Though some may think it’s a trivial number, our credit scores can have a tremendous impact on our lives. Your credit score can influence whether or not you get a good rate on a car or home loan, whether you’re approved to rent an apartment, and even whether or not you get a job!

When used responsibly, credit cards can give your credit score a big boost. Paying your credit cards on time and in full each month, keeping them open for a longer time, and utilizing only a small percentage of the credit available to you can help to improve your credit score over time.

Related: Learn and know these common credit score myths!

3. Welcome Rewards

Welcome rewards from credit cards can be a great way to earn some extra cash or travel perks just for spending like you typically would.

Credit card companies typically offer a lump sum of bonus points for spending a certain amount of money within the first few months of opening your card. These points can usually be redeemed for cash. Or sometimes they can be transferred to other rewards programs for your favorite airlines or hotels.

Bonus offers change all the time. So if you have your eyes on a certain card, it may make sense to check back and keep an eye out for an especially good offer of around 80,000 points/miles or higher. Luckily, we have a nifty credit card tool on our site that can help you to compare signup offers from tons of different cards.

Just make sure to take a good look at your spending to ensure that you can meet the minimum spend in the allotted time without making unnecessary purchases. If you have to spend an extra $1,000 you wouldn’t have spent otherwise to snag an $800 bonus, it completely defeats the purpose of nabbing those points.

4. Consistent Cash Back or Travel Rewards

Whenever you spend money on your credit cards, you can get a percentage of that money back in the form of cash-back or miles.

Different cards yield you different amounts. But the very least you can get with a rewards program is usually 1 point per dollar spent.

The redemption value of these points varies from card to card, but these rewards are nothing to scoff at. If you earn two points per dollar spent on every purchase, and each point is worth one cent, you could earn $200 for every $10,000 spent. While that might not sound like much, if you’re spending the money either way, why not enjoy the extra cash?

Here are some of the top rewards categories:

- Best Travel Rewards credit cards

- Best Cash Back credit cards

- Airline Miles & Rewards cards

- Hotel Points credit cards

5. Secondary Rewards

These are the rewards that most people probably forget about that could save you a ton of time, money, and heartache!

Some credit card companies offer extra benefits like extended warranties, rental car insurance, free checked bags and cell phone insurance. Some even offer credits for travel services like TSA Precheck and Global Entry which can save you hours at airports. If you utilize them, these can easily add up to hundreds (or even thousands) of dollars worth of value.

Secondary credit card benefit examples:

- The BILT Mastercard has cell phone protection

- The card_name includes primary rental car insurance

6. Accepted Almost Everywhere

It used to be that cash was accepted everywhere, and credit cards were only accepted at most places. Now, it seems like the tables have turned! Almost all stores accept credit cards these days, and doing all of your spending on a credit card can help you to more easily track your expenses!

The Downsides of Credit Cards

In the words of the great Hannah Montana, nobody’s perfect, and that includes credit cards. Even though there are tons of benefits to using credit cards for your everyday spending, be sure to watch out for these downsides.

1. You Could Be Paying More

One of the biggest drawbacks to paying with credit cards is that some merchants or restaurants will charge you more simply for paying with a credit card. That’s because when you use a card, the merchant typically has to pay fees to the credit card companies. While some places absorb that cost, others will charge you a 2-5% fee if you use your card. In this situation, it may be best to opt to use cash. Earning 2% back in rewards isn’t worth it if you’re being charged a 5% fee.

2. Potential Overconsumption

Another downside to using plastic for your everyday purchases is that it could subconsciously lead to you spending more money. MIT found that swiping or tapping your credit card lights up the reward center of our brains. Other researchers suggest that credit cards remove some of the “purchasing pain” we feel when we part with cash.

This is why budgeting and tracking your expenses is huge. Taking the time to input all the money you’ve spent each month is a great way to bring some more of that helpful pain back into your life.

3. Risk of Debt

Unfortunately, just because you use credit cards responsibly today doesn’t mean that it’s always going to be the case. Having access to credit does mean that you are at an increased risk of falling into credit card debt. This is absolutely one of the worst kinds of debt out there.

High interest rates can make it difficult to get out from under credit card debt,. So it’s best to avoid getting into it at all by being vigilant in paying off your credit cards in full and on time every month, pretty much forever and ever. That’s where automation can come into play.

Taking a few minutes to put all of your credit cards on autopay can help you to never miss a payment. You’ll never have to take that interest hit. Just make sure to still take the time to look over your credit card statements to monitor for fraud and track your spending.

However, if you do find yourself with some credit card debt, be sure to check out our post on creating a debt payoff plan.

4. Annual Fees

Now if you know anything about How To Money, you know that typically, we HATE fees.

Especially the kinds of fees that you don’t get any value from. Like pesky bank fees that charge you just to keep your account open, or hidden fees on concert tickets. However, our opinion of credit card fees is a little more nuanced than you might expect.

While some cards carry hefty fees of up to $695 dollars, others have smaller fees of around $100 each year. While that does seem like a bummer, usually you can get way more value than the annual fee back if you take full advantage of benefits and rewards.

For example, if your annual fee is $95, and you get a signup bonus which equates to around $800 worth of free travel, you would still come out on top that year with $705 worth of value you didn’t have before.

Add in the extra benefits, like bonus points earned in certain spending categories, free global entry or TSA precheck, and cell phone insurance, and you’ll find that each year you probably come out on top even if you don’t take the signup bonus into consideration.

For the cards with larger fees, you will likely have to travel or spend a lot for them to make sense for you. There are tons of people who travel frequently who feel that these bring them value. At the end of the day, it’s all about your spending habits. And also deciding whether or not you’ll be able to take full advantage of the benefits a card has to offer.

Psst: Here are the best $0 Annual Fee credit cards!

5. Devalued & Unused Benefits

Lastly, one of the most egregious downsides of credit cards is that sometimes people forget to redeem their points or miles! According to a Bankrate study, 31% of people don’t cash in on their rewards.

Be sure not to hoard all your points for the perfect trip years from now. Because credit card companies tend to devalue their points over time. That’s another great reason why it’s important to stay organized, keep track of your rewards, and actually cash them in.

Credit Card Benefits FAQs!

Getting together the perfect credit card strategy can be a little confusing. So here are answers to some of the most frequently asked questions about credit cards.

How many credit cards should you have?

If you can handle them responsibly, you can have as many credit cards as you want! However, about 3 seems to be a great number for a lot of folks. If you’re just starting out, it might be a good idea to try “Our ‘Super Chill’ Credit Card Strategy.”

What is the best credit card?

There are tons of great credit cards out there. The best one for you will totally depend on your spending habits. For example, if you commute to work it could be a good idea to find a card that offers you extra cash back at the pump. If you spend a ton on travel, then a travel rewards card might be best for you. Luckily, we have a few lists that can help you decide which card is the best for you!

- 5 Best Credit Cards for Students

- 7 Best Credit Cards for Stay at Home Parents

- Best Travel Rewards Credit Cards for Beginner

- 8 Best Credit Cards for Side Hustlers

Does having more credit cards build credit faster?

While having more than one credit card could indirectly help to boost your credit by lowering your utilization, it won’t necessarily help you to build credit more quickly.

If you have more credit available and spend the same way you typically do, you’ll end up with a lower utilization rate which could provide a small boost. However, the best way to boost your credit score is to pay your debts on time, all the time. Rebuilding your credit takes time and patience, but is a totally worthwhile pursuit!

The Bottom Line:

Credit cards are a great money tool which can allow you to build credit and earn tons of awesome rewards. However, if you neglect to take advantage of all the perks your cards have to offer, you could be missing out.

Be sure to take a look at what special credit card benefits you have available. Also check out our credit card tool if you’re looking to find the cards with the best signup bonuses!

Beer tasting notes:

While talking about common credit card benefits we enjoyed a Chief of Chiefs by Bearded Iris! And please help us to spread the word by letting friends and family know about How to Money! Hit the share button, subscribe if you’re not already a regular listener. And give us a quick review in Apple Podcasts. Help us to change the conversation around personal finance and get more people doing smart things with their money!

Best friends out!

*Advertiser Disclosure: How to Money has partnered with CardRatings for our coverage of credit card products. How to Money and CardRatings may receive a commission from card issuers. Some or all of the card offers that appear on the website are from advertisers. Compensation may impact on how and where card products appear on the site. Lastly, the site does not include all card companies or all available card offers.

*Editorial Disclosure: Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

*User Generated Content Disclosure: Responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.