Consumer debt is way more common than you might think. In fact, about 3 in 5 Americans have credit card debt. When you include mortgages, student loans, auto loans and personal loans, the average American is carrying about $59,580 worth of debt! With a burden this large, you might be wondering, “how can I possibly become debt-free?”

Maybe you spent a few months without employment and used credit cards to keep yourself afloat. Or maybe you an overpriced degree given the career you ended up with. Either way, in most situations, people accumulate debt over a time period of a months or years. Getting rid of that debt doesn’t happen overnight.

However, as impossible as it may seem, we promise that after reading this post, you’ll not only discover that it is possible to get out of debt, but you’ll have the basis of a solid action plan to help you achieve debt freedom.

Yes, it takes time. Yes, it’s hard work. But with dedication and persistence, YOU can (and will!) pay off that debt and live a healthier financial life!

Why You Need to Get Out Of Debt:

Being in debt is expensive. Certain debts, like credit cards and personal loans, carry high interest rates, sometimes even as high as 30%! That compound interest works against you, causing your debt to balloon when left unchecked.

Compound interest works both ways. It’s a wonderful thing when you’re investing money and building wealth. But when you’re in debt, it really hurts and that same compounding effect works in the opposite direction. That means that getting out of debt ASAP is really important – you want that powerful force of compound interest working for you for as many years as possible!

Folks constantly underestimate the total interest paid when taking on debt to make purchases. Buy now, pay later programs, credit cards, or even splitting purchases into monthly payment options really adds up. Even if you’re buying something on sale, you could easily end up paying MORE than the original purchase price.

For example, let’s say you buy that fancy new Playstation VR Headset for $550 and put it on your credit card with a 22% interest rate. You decide to pay it off slowly over time, just making the minimum payment of $15.58. At that rate, it will take you over 5 years to pay it off. When all is said and done, that headset will have cost you a whopping $893. Talk about a rip off!

Even if the retailer was to offer you $100 off the purchase price, you’d still pay significantly more than the original retail price if you paid for it with that credit card!

Debt is bad for your health

There’s another downside of debt that rarely gets mentioned. Debt doesn’t only have a monetary cost. In addition to straining your finances, it can seriously impact your physical and mental health. 87% of us suffer from financial stress, according to the American Psychological Association. High debt loads are linked to prolonged stress, depression and anxiety.

So it’s not just that the math doesn’t work in your favor. Too much debt weighs us down psychologically. That’s another massively important reason why it’s important to work towards paying off your debt as quickly as possible!

Not all debt is bad debt

It’s important to mention that not all debt is created equal. Lingering credit card debt at an interest rate of 23% is clearly far worse than the remnant of your 0% auto loan. The conversation around lower interest debt needs to be more clearly articulated and better understood.

The two main reasons debt can be good is a) using debt to purchase appreciating assets, and b) having a very low, fixed interest rate.

Sometimes debt allows you to buy something you would never be able to save up for with cash, like a home. Mortgage debt is generally considered good debt, because it’s both fixed at a low rate AND it’s used to purchase something that appreciates in value over time.

Another example might be financing a meaningful education that leads to a higher salary and increased job satisfaction for decades to come.

However, even taking out that “good debt” should be done within reason. While a little student loan debt could lead to an ultimately positive outcome, a lot of it could do harm to your financial future. The same goes for purchasing a home. Buying something outside of your means could put a serious strain on your monthly finances.

The “good debt” versus “bad debt” debate comes into play because there are certain debts that should be your priority for debt payoff. Mortgage debt you took out a few years ago at a low interest rate, for instance, should be considered far less important than an outstanding HELOC balance when that rate has risen substantially.

This is because if you have a mortgage at something like 3.5%, you can likely earn enough money in a high yield savings account to cover the costs associated with that interest rate. For example, if you snag a HYSA with a 4.35% APY, you’re actually making out financially with an extra .85% on your money by placing your funds in your savings account versus paying additional money towards your mortgage. That’s why that mortgage should be seen as a lower priority debt. If savings rates decline in the future, you can always push those dollars towards mortgage debt payoff then!

How to Get Out of Debt

OK, now let’s talk about how exactly you can get out of debt. The best way to tackle debt is to make and stick to a debt payoff plan. Here’s a step by step guide on how to make your own!

Step 1: List Out All Your Debts

First, we need to look the debt monster in the face, as ugly as it can be. You can’t pay off your debt if you don’t know exactly what you owe. You need to face the numbers in black and white.

Begin by logging into all of your accounts and listing out each debt you owe. Include the balances, as well as their interest rates. Don’t forget to list any after-pay amounts owned, as well as negative assets. This means all of your credit cards, any personal loans, car loans, and student debt. Even your mortgage can be listed out here if you’re looking to pay it off early.

Here’s an example of what your list might look like:

- Credit Card 1: $1,343 at 18% interest

- Credit Card 2: $3,603 at 22% interest

- Car loan: $8,200 at 6.5% interest

- Student loan: $10,350 at 5% interest

- Mortgage: $280,000 at 7% interest

A lot of people underestimate just how much they owe, which is why this step is crucial. You’ll never be able to get out of debt if you don’t confront the numbers head on.

Remember: Shame has no place in personal finance. Don’t beat yourself up over past mistakes and purchases. You can’t go back in time (unless you’ve invented a time a la Dr. Emmett Brown), so there’s no point in harping on it. What’s important is that you’re taking the steps now to improve your finances, so give yourself a pat on the back!

Are any debts negotiable?

If your interest rates are so high that you are unable to take down your balance, it could be worth calling your debtors to negotiate. They are used to getting calls like this, and might have special programs available for you. While it’s unlikely that they will immediately forgive outstanding amounts, they could potentially offer you a lower interest rate, which will make it significantly easier to climb out of that debt hole.

Medical debts are usually negotiable, and the earlier you jump on negotiation opportunities, the better it will be for your credit profile. Even if your debts are now with a debt collecting agency, many of them are able to offer significant discounts too.

By the way, there are several no-profit agencies that help people with extremely overwhelming debt situations. We’ll cover those a little later on in the tips for success section!

Step 2: Choose a Debt Payoff Method

Now that you’ve listed out each of your debts, it’s time to make a custom debt payoff plan. Grab your hooded cloak and get ready to adopt a debt-slaying identity! Fully commit to spending the next few months (or years) of your life prioritizing this single goal. Slashing debt out of your life will be completely worth it.

There are two popular methods of paying off debt within the personal finance community: the debt snowball method and the debt avalanche method. Each comes with its own unique benefits. You can choose which dogma to follow according to which will best suit your personality and specific situation. They work as follows:

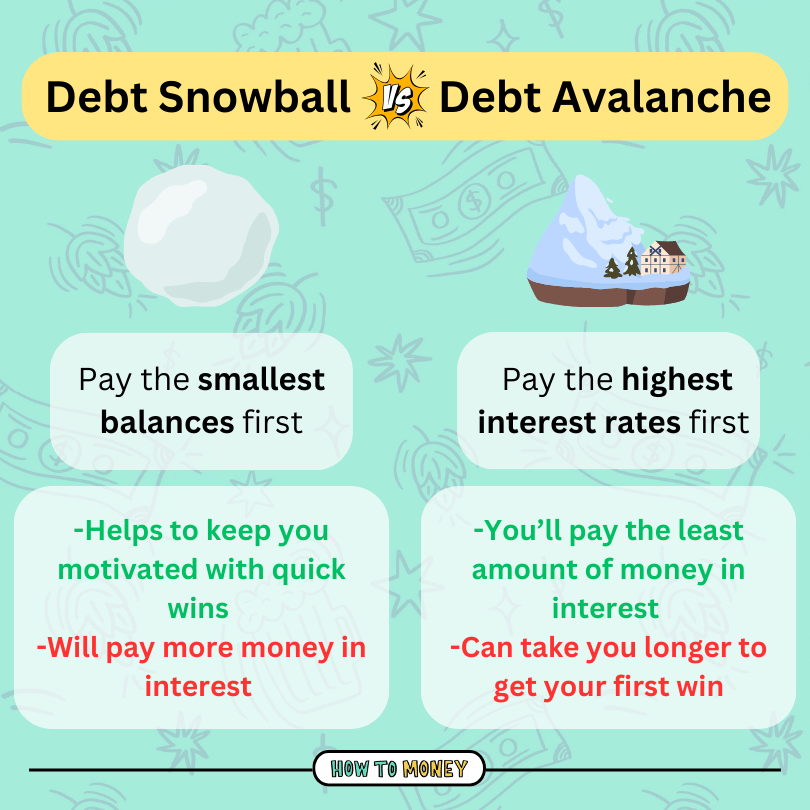

The Debt Snowball:

The debt snowball method places a higher emphasis on working with our human psychology to get out of debt. With the debt snowball, you’ll start to rack up some wins more quickly – which is a really important factor in starting your debt journey.

How it works: You will make the minimum payments towards all of your debts. You’ll then use any additional money you have to pay off the smallest debt first!

Once you pay off that first debt, you’ll take the monthly payment you were putting towards that first debt, and snowball it into your second smallest debt. Think of those cartoons where a snowball rolls down a hill and grows in size until it looks like a rolling boulder from Indiana Jones. With each debt you pay off, you can attack your next one with an even bigger snowball (aka more money), giving you tons of momentum!

Sticking with our example list of debts from earlier, the two lowest balance debts are the credit cards. Using the debt snowball method, you would pay off credit card 1 first, before moving on to credit card 2. Then you’d tackle the car loan, student loans, and finally your mortgage.

Let’s say you make the minimum payments on all of your debts, and allocate an extra $300 each month to pay off your debt. Once you pay off credit card one, you’ll be able to throw that extra $300 plus the monthly payment amount from credit card one towards credit card 2!

The reason behind paying off the smaller debts first is psychological. Taking this route can get a few wins under your belt in a relatively quick time. This can provide you with the motivation you need to keep going until you’ve completely erased debt from your life.

However, the debt snowball does take some flak from some people within the personal finance space. That’s because technically it’s not the “financially smartest” way to pay off debt. You could end up paying more when all is said than done when compared to the debt avalanche method.

The Debt Avalanche:

If you are a numbers person and have a lot of motivation to get out of debt on your own, you may want to take the debt avalanche approach instead of the debt snowball one. This method of debt payoff prioritizes paying the least amount of money in interest overall.

Here’s how it works: You still make the minimum payments on all your debts like before… But you apply any additional money towards the debt with the highest interest rate first. Once you pay that debt off, you then allocate those funds towards the debt with the second highest interest rate, and so on and so forth.

Back to our example debts, the avalanche method would have you paying off credit card 2 first, because it has an interest rate of 22%. After that debt is gone, you’d next prioritize credit card 1, which has an interest rate of 18%.

While you will pay less in the long run, it will only save you money if you actually stick to it. (Actually, no payoff plan works if you quit.) Letting that debt linger for longer if you get burnt out will eat away at any monetary difference between the debt snowball and debt avalanche.

Which method should you choose?

Different ways of getting out of debt will appeal to different people. If you are gung ho about saving as much as possible, the debt avalanche will likely make more sense for you. If you struggle to find the motivation to pay off debt, the debt snowball can provide you with the wins to keep you going.

However, you don’t have to pick just one method and shun all others who disagree. Feel free to take a hybrid approach if that resonates more with you.

Let’s say you have a credit card with a larger balance and a 23% interest rate and a 6% car loan with very little left on it. Because there is a massive difference between the interest rates, you might opt to tackle that sky high credit card debt before switching to the debt snowball for the rest of your accounts.

Step 3: Make a debt payoff plan

Now that you’ve chosen a payoff method and know which order to tackle your debts, it’s time to commit to an action plan.

Pro tip- take your commitment one step further by writing everything down. It’s been shown that people who write down their goals are 42% more likely to achieve them!

First, list your debts in order of priority. If you’ve chosen the debt snowball, your top priority will be your debt with the lowest balance. If you’re sticking with the avalanche, this means prioritizing the debt with the largest interest rate.

Then, it’s time to set some SMART goals for yourself. Give yourself a timeline by which you think you can realistically get out of debt based on the numbers you’ve run. Having an end date in mind can make it feel more real. It’ll keep you motivated to keep going, even when you feel like giving up, because you’ll see the light at the end of the tunnel!

Create a tracking system

It’s really important to track your progress as you begin to pay down debts. Watching the needle move will motivate you even more with each payment you make.

For visual people, make a simple poster where you can color in progress blocks every time you make a payment. It sounds a bit juvenile, but it works!

A simple spreadsheet will also work great. You can find a plethora of them online, but our advice is to keep it extremely simple. No need for all the bells and whistles – you just need something to track your progress and date stamp your payments.

It’s also important to give yourself some milestones to celebrate along your payoff journey! Treat yourself each time you eradicate a debt from your life. Have some friends over and celebrate when you reach the 50% payoff mark on your student loans, or when you hit a new net worth milestone. And when you reach the goal post of finally becoming debt free, you deserve to throw yourself a little party!

Should you consider a balance transfer card?

If you’re certain that your days of overspending on plastic are behind you, you could consider opening a 0% balance transfer card to consolidate and tackle your credit card debt. This will essentially help to “stop the bleeding,” because it will give you a specified period of time (typically 12 – 18 months) to pay off your cards with 0% interest.

However, this can be a little bit risky. If opening a new line of credit tempts you to repeat past mistakes, you could end up with an even bigger balance at the end. So proceed with caution!

Only pursue this option if you are absolutely certain you will pay off all that debt within the 0% interest time frame.

Also, balance transfer cards come with a transfer fee, usually 3-5% of the total debt transferred. Definitely do the math to make sure this will work out in your favor. There might also be a temporary dip in your credit score.

Here’s a quick example of how you can save money on interest:

All in all, balance transfer cards are a great tool. But you need to be extremely savvy and have a solid payoff plan for them to work out well.

Here are the top 0% APR balance transfer cards available right now.

Step 4: Accelerate Your Progress

Now it’s time to accelerate your progress towards becoming debt free. Although there is no quick fix for getting out of debt, there are a number of steps you can take to speed up your journey.

Adjust your budget

Take a look at your budget and see if there is any additional money you can funnel towards paying off that debt. Even if it means cutting some comforts from your life temporarily. Can you drop down to just one streaming service? Start walking to work or riding your bike more to cut down on car trips? Switch your cell phone bill to a more affordable plan?

Even finding an extra $100 in your budget each month will make a huge difference when it comes to your payoff timeline. For example, if you are paying down a $2,000 credit card balance, contributing $300 towards that debt each month instead of $200 translates to paying off that debt in 8 months instead of 12! Plus, you’ll save $79 in interest. Every dollar really does count when it comes to debt payoff!

However, you’ll need to sustain your lifestyle for a few months or years to get out of debt. Make sure not to commit to a plan that’s so extreme you give up in a matter of weeks. Find a balance that you can live with long term, and remember that it is okay to spend a little money on yourself while getting out of debt as long as you don’t overdo it!

Increase Your Income

A great way to accelerate your debt slaying progress is to work on increasing your income. As long as you avoid lifestyle creep, you’ll have more money available to throw towards your debt!

Consider setting up a meeting with your current employer to negotiate a pay raise. Alternatively, investigate whether or not you could earn more by switching companies to snag an even larger pay increase. It could even be worth it in some cases to switch industries to something more lucrative for the duration of your debt payoff journey. Leave no stone unturned.

If you want to stick with your current employer, you could also work towards starting a side hustle. This could bring in hundreds of extra dollars each month, or even eventually become your main source of income.

Related: How to build wealth with a small income

Spend Less

If you want to see the biggest change in your balances, it’s important to attack your finances from both ends- earning more and spending less.

Try and make an effort to spend less money each and every month. Remember that each dollar you don’t spend on things that don’t move the needle for you means having an extra dollar to funnel towards debt payoff. Future you will be very grateful.

Ask yourself if it might be worth switching to a bare bones budget, which contains only your needs, for a specified period of time. While it might not be sustainable over the long term, this can help you make more significant progress in a short period of time.

If you’re in HEAVY debt, it might even make sense to move back in with your parents if possible and do a complete reset of your financial life. Desperate times call for desperate measures!

Tips for Success

Getting out of debt can be a loooong and sometimes frustrating process. However, there are plenty of ways that you can make it easier, and dare I say it… even a little bit fun?

Automate your payments

Automating your payments can be a super easy way to make sure you stick to your debt payoff plan. By setting up an automatic payment, you’re essentially paying yourself first. It removes the need to make a decision each month as to how much money you’re going to put towards that debt.

Instead of just putting whatever money you have left at the end of the month, you’ll be making your payments first. Then, for the rest of the month, you’ll be forced to work with the remaining money in your accounts. This will encourage you to really get creative with living off whatever is left!

Start by scheduling a recurring payment of $xxx directly to your debt account every pay day. Out of sight, out of mind! Automation > self-discipline.

Get accountability partners

There’s a reason the HTM podcast is hosted by a pair of real-life besties. That’s because they know that everything is better with a friend!

If I’m being honest, I rarely go to the gym on my own. But you best believe that if I made a date to go work out with a friend, I’ll be there no matter how tired or unmotivated I feel. The same holds true for you and your money.

If you want to make yourself even more likely to stick to your debt payoff plan, get someone you love involved. Whether it’s your partner, or a friend or family member in a similar situation, teamwork makes the dreamwork! Plus, in getting a friend involved, you could be helping them to take control of their own finances.

Can’t find someone to take on a debt slaying journey with you? You could also join the How To Money Facebook group! It’s full of tons of folks who love to help each other out and support each other on their financial journeys.

Get some help from software

If you’re new to managing your money, it could be helpful to get some additional support from a budgeting program. Our favorite budgeting software to use is YNAB! Although there is a small subscription cost, the average user saves more than $6,000 in their first year using the software. That’s a lot of money. Plus, sometimes getting a little skin in the game by paying a small subscription can encourage you to really stick with your money plan.

However, if you’re looking for a free alternative to YNAB, you can check out Mint. It does have fewer features but it also a great start if you’re looking to track your spending.

Don’t neglect emergency savings

You might be tempted to throw ALL of your cash at your debt in order to pay it off sooner. But it’s really important that you keep some cash on hand for emergencies. You’ll need it for surprise expenses over the course of your debt payoff journey. Otherwise, you’ll end up using credit cards to stay afloat and just end up back where you were before.

Work on creating a basic emergency fund of $2,467 in liquid cash. Economists have found that having this amount of money in the bank can typically cover most emergency expenses. Stick this emergency cash in a separate savings account so you’re not tempted to dip into it.

Bonus- It can be difficult to know which area of your finances to prioritize at what times. If you’re not sure where to start, check out the money gears! They can serve as a helpful guide if you aren’t sure where to start your money journey.

Gamify Your Debt Payoff

If you’ve ever seen your parents get absolutely addicted to Candy Crush, you know that games are designed to leave you wanting more. Bringing in some of the elements of gaming. Using competition, rewards, and having an overarching objective can make paying off debt significantly more enjoyable.

Think through some ways that you can work these elements into your debt payoff goal. Can you plan some kind of cheap reward for yourself each time you pay off a balance? What about creating a friendly competition between you and your friends to see who can come up with the best cheap day out to save money together?

Putting a fun twist on these day to day money-saving tasks can make getting out of debt seem less daunting, and maybe even a little fun. So much of the way we handle finances is tied into our money mindset, so taking a more positive approach to debt payoff can make a huge difference. By gamifying our biggest money goals, we can stay even more motivated to win!

Seek professional help

If you’re feeling overwhelmed by your debt load, it could be time to bring out the big guns. If you need extra support, seek it out from professionals at a reputable non-profit organization, like the NFCC or Money Management international!

These organizations can typically offer you free or extremely affordable appointments with debt counselors. They can help you to manage your debt, as well as sometimes advocate on your behalf. However, it’s important to go through one of these reputable non-profits and watch out for scammers who claim they can get your debt forgiven. Those promises are too good to be true and will push you into further financial pain.

Step 4: Stay out of Debt

Congratulations! You’ve made your final payment, and now you get to enjoy life debt free! At least, if you manage to keep yourself from going back into debt.

Perhaps the most important step in getting out of debt is staying out of debt once you’ve paid it all off. Hopefully you’ve learned from your mistakes and will do everything in your power to avoid taking on bad debt in the future. Use these tips to make sure you stay out of debt for good!

Develop mindful spending habits

If you’ve ever found yourself in bad consumer debt, you may need to spend some time developing mindful spending habits. Simply put, mindful spending is just being intentional about how you spend your money. It’s thinking through our purchases to make sure that we actually care about the things we are buying.

Here are a few simple mindful spending habits to start incorporating into your life!

- Put items on a 24 hour wait list and only buy them after that time has passed.

- Try and get ahead of your spending triggers. For example, if you know that you tend to splurge on takeout when you’re tired, find some easy no-cook recipes you can use instead on those low energy days.

- Cancel any subscriptions you no longer use on a regular basis.

- Start thinking about costs in terms of hours worked.

Even without a goal in mind, healthy money habits can carry us far. By healing your relationship with emotional spending, you’ll be setting yourself up for future success.

Fully fund your emergency fund

Having sufficient cash in the bank can help you to avoid taking on debt should emergency expenses arise. Now that you’ve got your $2,467 basic emergency fund, it’s time to work towards fully funding that bad boy. That means amassing 3-6 months worth of expenses and socking it away into your high yield savings account.

Having 3-6 months of expenses saved up will likely mean that you’re covered should you face any larger emergencies. Things like losing your job, dealing with pesky (and costly) car troubles, or an unexpected dentist bill. Not only will you be at a far lower risk of needing to take on debt to stay afloat- you’ll enjoy more peace of mind knowing that your finances are covered!

Continue your personal finance education

Another great way to stay motivated to stay out of debt is to continue your personal finance education. Now I’m not saying to drop what you’re doing and head to the nearest ivy league college to get a new degree. You can learn tons right from the comfort of your own home!

Consuming the right kind of content can leave you feeling motivated to attack your biggest money goals. Instead of scrolling through pictures of the newest, cleanest looking kitchens on instagram, personal finance podcasts are a great way to learn about money and provide yourself with gentle reminders to be grateful for what you do have!

Plus, cracking into some of our favorite personal finance books can be a fun and enriching cheap activity. You’ll learn a little bit about the way our brains work, read about interesting and inspiring stories from others, and walk away from it feeling a little bit smarter.

Debt Payoff Example with the Numbers:

Julia is $49,750 in debt, and she wants to pay it off as soon as possible! She creates a list of all her debts and their interest rates. It looks like this:

- Discover Card: $5,400 at 20%

- Chase Card: $4,350 at 18%

- Car loan (4 year): $10,000 at 7%

- Student Loan: $30,000 at 4%

And here is what their minimum payments look like:

- Discover card: $108

- Chase card: $87

- Car loan: $239.46

- Student loan: $222

Julia decides to go with the debt snowball method, and pay off her debts according to their size. This means, Julia will attack them starting with her Chase card, then her Discover card, her car loan, and lastly her student loan.

Luckily, Julia is able to put both of her credit cards on a balance transfer card. Meaning, she has 0% interest for 12 months. Now, her credit card debt looks like this:

- Balance Transfer Card: $9,750

In addition to the money needed to make the minimum payments on all of her debts, Julia works on her budget to find an extra $400 each month to put towards her debt. She also starts doing some freelance writing work and pulls in an extra $500 each month. This means she can allocate an extra $900 each month to pay down debt.

While making the minimum payments on her other debts, Julia pays $1,095 towards her credit cards each month, and pays them off in 9 months. Now, her debts look like this:

- Balance transfer card: $0

- Car loan: $8,521

- Student loan: $28,888

Now, she’s going after that car loan. She rolls the payments she was making towards her credit card into the car loan. Each month, she’s putting $1,334.46 towards her car loan. She pays it completely off in just another 6 months, 15 months into her debt payoff journey! Now her debts look like this:

- Balance transfer card: $0

- Car loan: $0

- Student loan: $27,999

Now it’s time for the kicker. Julia’s about to tackle the biggest debt of all- her student loans. Luckily, she’s got a ton of money to throw at it each month as her “snowball” has grown with each debt paid off. Now, she has $1,556 each month to use to demolish her student loan.

It takes her longer than the others to pay off, but Julia manages to absolutely slash that student loan out of her life in just 18 months. That’s a total of 33 months from when she began her debt payoff journey. In under 3 years, Julia has eradicated nearly $50,000 of debt from her life.

Now, Julia uses tools like her emergency and sinking funds to be prepared for both planned and unexpected expenses. She practices mindful spending every time she’s feeling a little spendy. And best of all, her salary stretches so much further without having to make any payments towards debt. She’s finally able to save up a down payment for that house she’s always wanted. Plus, she doesn’t get a stomach ache every time she opens her credit card statement. Even though it was a difficult journey, Julia is happy she made the choice to prioritize paying off her debt!

The Bottom Line:

Debt is sort of like that little leak we notice one day under the sink. When it’s just a few drops of water, it can be tempting to just look away and pretend you didn’t see it. But left unattended to, it can burst out of control, costing you thousands of more dollars than if you had dealt with it sooner.

That’s why it’s important to face the ugly monster that is debt head-on. Because of the nature of high interest rates, the best day to start paying down your debt will always be today.

If you need support throughout your debt payoff journey, make sure to join our HTM facebook group. Also, submit questions to our “Ask HTM” segment on the podcast. Stay diligent, stay patient, and you will wake up one day completely debt free.