Whether you decide to strike it out on your own right after finishing school, or live with your parents until you’re 50, the move out of your parents’ house is a huge milestone. Ok, the latter might represent a case of ‘failure to launch.’ But moving out on your own represents you taking a huge step towards independence and adulthood, and it can be tremendously rewarding if done right.

However, moving out can come with lots of new challenges, both financial and emotional. That’s why we’ve created this ultimate guide to help you transition to greener pastures with the least amount of pain possible. Bye bye, Mom and Dad!

How to Move Out of Your Parents’ House

It’s both an exciting and intimidating time. But fully thinking through the transition and steps required will reduce your stress and make sure nasty surprises don’t pop up. Here is an overview of the steps we’re going to discuss in this post.

Step 1: Assess Your Readiness

The more planning you do upfront, the more headaches you’ll avoid later. If you jump the gun and move out before you’re truly ready, this can really hurt you emotionally and financially.

If things don’t go smoothly, you might end up moving back into your parents house, which can set you back a pretty penny. It can potentially strain your relationship with your family too.

That’s why it’s important to assess your readiness before you start taking steps towards moving out. So curb your excitement, and think through these areas of your life first. 👇👇👇

Are your finances ready?

Let’s talk about your money situation. You’ll need a thorough plan to survive out on your own financially. Or else you might slip into debt and handicap yourself for years to come.

Do you have the funds to move out? Do you have good money management skills to live independently? If unexpected expenses pop up, do you have the skills and grit to tackle those issues without taking on debt?

Here are a few personal finance to-do items that we suggest you check off before you strike it out on your own…

Become a master budgeter

Now that you’ll be managing your own expenses, and likely take on more financial responsibilities, it’s time to get well acquainted with budgeting. Budgeting is a great way to keep track of your spending, manage your finances, and even give yourself the freedom to spend on things that bring you joy. We’ll talk more about budgeting in Step 3!

Build an emergency fund

Did you know that around two thirds of Americans can’t afford to cover a $400 emergency expense? When you’re living on your own, it’s likely that you’ll be faced with the occasional emergency expense. Cars break down, people get sick, and sometimes you spill an entire bowl of soup onto your work laptop (totally not speaking from experience here 😅).

I would suggest waiting to move out until you’re built up a basic emergency fund of $2,467. Pointy-headed economists have found that socking away this amount of money can help you to cover most unexpected expenses.

Check in with your credit score

Whether you’re planning on renting or buying a home, your credit score will have a big impact on the options available to you.

Depending on where you are along your personal finance journey, you may have made some poor decisions in the past when it comes to credit. Or maybe you’re just starting out and have never even opened a credit card. Either way, maintaining good credit means getting approved to rent the apartment you want. And it also means getting the best rates on loans. That’s why you should take some time before moving out of your parents’ house to work on building your credit score.

Save up the actual money it costs to move out. Lastly, it’s important to make sure you have enough money saved up to cover the cost of moving out. If you’re moving out for the first time, chances are you’ll need to purchase a lot of stuff. Like furniture, kitchen utensils, and some decor. Also you’ll need to save for a realtor fee and security deposit for an apartment.

Facebook Marketplace and local Buy Nothing groups will help you save a ton. But you’re unlikely to get everything you need for free!

Do some research on the cost of living for the area you want to move to. Typically, you’ll need to pay the first and last month’s rent when you move in, along with a security deposit. This cash pile needs to be in your bank account before you can begin the actual process of moving out.

Are you emotionally ready?

It can be really stressful to think about an upcoming move out of your parents’ house. It’s a big life transition! Are you ready to emotionally tackle more of life’s challenges on your own? Be honest with yourself.

Maybe you’ve already lived in a dorm during your college years and are well acquainted with living semi-independently. But if you’ve never lived on your own, making these changes can be difficult. It’s OK to admit to feeling a bit scared – you are not alone!

A great compromise is to move in with roommates. Roommates can massively alleviate the financial burden of moving out by splitting expenses with you and helping you navigate any issues that arise. Plus, if you’re able to move in with one of your friends, you can enjoy the benefit of living with someone you can rely on for some emotional support.

Before you move out, practice developing some good stress and anxiety management habits. Some of our favorite ways to manage stress and anxiety is with regular exercise, by talking to close friends and family, and reminding yourself to break down overwhelming tasks into manageable baby steps. Remember, you can also reach out to a therapist if you find you need help developing healthy coping skills.

It’s also important to make sure you build up a solid support system while you’re moving. You might be one of those people that hate asking for help… But trust me, tackling everything on your own puts unnecessary stress and pressure on yourself. Do your best to let your parents, family and friends help you. (They probably want to!). Knowing you have a solid foundation of people who can help you will make you feel more confident in this new stage of life.

Step 2: Start Planning Your Move

Next, it’s time to start actively planning the move out of your parents house and into your new pad. We’re talking about researching places, making dates and deadlines, as well as telling your folks and being realistic about what your new life will look like.

If you’re 22 years old and moving out for the first time, it’s unlikely you’ll be able to afford that 6-bedroom penthouse apartment in midtown Manhattan. Unless you bought loads of Apple stock in elementary school that is. Instead, do some research on what you can afford and plan accordingly.

Create a timeline

The earlier you begin planning your move, the more time you will have to prepare. Decide when you want to move and come up with a plan to save up the money. Crunch the numbers and figure out when you could realistically move out.

For example, let’s say your plan is to move out in 6 months. And let’s say you’ll need $4,000 to make it happen. For the next 4 months you’ll need to figure out a way to set $1000/m aside, building up the cash you need. Then for the following 2 months, you can spend that time finding a suitable place, and making the move!

Pro tip: Creating a sinking fund can help you save for your moving costs!

Research neighborhoods

In order to move out of your parents’ house, you’ll need to figure out where you want to live!

If you are hoping to move within an hour or two of where your parents live, I would highly suggest researching online a few different neighborhoods you’re interested in living in. Then, start spending some time there while you’re saving up a moving nest egg. Hit up the local coffee shops, bars, and other cultural centers and spend some time talking to the people who already live there. The goal is to get a better understanding of the vibe of the neighborhood.

If you want to move across the country however, it may be more difficult to start spending time there before you move out. Be sure to thoroughly research neighborhoods online before you get there. And if at all possible, try and visit before your move. Sometimes you’ll know if a place is right for you just by exploring for a weekend.

It’s also important to make sure that you can afford to live in your prospective area. You can use this fair rent calculator to determine the average rent of an area you’re looking to live in. If you’re looking to buy, make sure to come up with a proper home buying strategy.

Secure a Job/Income in Your New Area

Hopefully you’ve already got a solid job and enough income to support yourself. Or maybe you’re looking to move out to be closer to a job you already have. If you’re working and happy with your income level, congrats! You can skip this step.

But unless you have a fully funded emergency fund (I’m talking 6 months worth of expenses on hand), you’ll want to do your best to line up some kind of income or employment before you get to your new crib. This will help ensure you can cover your monthly expenses once you move.

Step 3: Budgeting for Independence

Next comes the more logistical part. It’s time to figure out exactly how you’re going to manage day to day expenses living on your own.

While it’s possible to just wing it, we highly recommend coming up with a money plan before your move to avoid any unpleasant surprises. Too many people don’t take finances seriously, which leads most of them to live paycheck to paycheck.

Here are just a few tips to help you budget for independence.

Choose a budgeting method:

Before you move out of your parents place, it’s a good idea to learn the basics of budgeting. This means tracking your income, managing your expenses, and making sure you’re socking money away for retirement too.

Don’t worry, budgeting can actually be FUN! Because it’s not about restricting your ability to enjoy your life and spend in the way you see fit, budgets actually give you the freedom to spend more on the things you love instead of frittering money away haphazardly.

There are 3 budgeting methods we typically recommend for those getting started: The 50/30/20 method, the cash envelope method, and the zero based budgeting method.

The 50/30/20 method

For the 50/30/20 method, you’ll allocate 50% of your income towards your needs, including expenses like housing, food, transportation, and insurance.

Next, 30% goes towards your wants. This money is for non-essentials, and things that bring you joy. Here’s a guide to differentiating between needs and wants so you know how much to spend on each.

Lastly, 20% of your income should go towards savings and retirement investing. This money can also be allocated towards debt payoff if you have outstanding loans or credit card debt. If you’re new to retirement investing, check out this beginners guide.

The Cash Envelopes Method

If you struggle with overspending, the cash envelope system could be the best budgeting method for you. Essentially, you label an envelope for each category in your budget. Then, whatever amount you allocate towards that line item, you place the same amount of cash into the corresponding envelope.

When you go out to shop, take the shopping envelope with you. For groceries, pay out of your grocery envelope. Since there’s a finite amount of cash in each envelope, it helps you be more aware of your spending. It places hard boundaries that can help you stay the course.

Zero Based Budgeting

With a zero based budget, your goal is to have $0 unaccounted for at the end of each month. Utilizing this budgeting method, you give every dollar a job. This is perfect for the money nerds, number crunchers, and more advanced budgeters.

A budgeting software can help you do this really easily. We love and recommend You Need A Budget, which is a crowd favorite for those just starting to budget seriously.

Remember, budgeting is all about finding what works best for you, so feel free to get creative and combine some or all of these budgeting methods for a more hybrid approach.

Add up all your income

Next, it’s important to add up all of your income, and track it throughout the year. This should be pretty simple! Remember to include any bonuses from work, side hustles, or things like tax refunds.

If you’ll be starting a new job after your move, it’s okay to budget with your anticipated income as well. Just be sure to make adjustments to your budget after you get your first few paychecks to account for any differences.

Calculate Your Living Expenses

Now, list out all of your living expenses and monthly costs for your new independent life. Again, you may have to budget using the average expenses for your area and adjust as you go.

Even though some costs are unknown, do your best to guess. And use higher numbers just to make sure there’s some wiggle room. Here are a few expenses you may need to account for each month depending on your living arrangement:

Watch Out for Hidden Costs!

When you first move out of your parents house, you might feel like little surprise costs are popping up out of the woodworks to ruin your budget. You’ll start to question your sanity as you discover new things you had at your parents house that you never thought you’d need to buy. Like potholders? Younger me did not foresee a future where I would need to spend my own money on potholders. But #adulting comes for us all at some point.

The truth is, furniture and household items can really add up and make a dent in your bottom line. While you can definitely reduce this cost by scouring Facebook Marketplace or local thrift shops, it’s a good idea to budget extra for those first few weeks living on your own.

Eating out is a slippery slope

One of the biggest budget busters out there is constantly eating out. When you move out of your parents house, it’s important to get into the habit of cooking at home as much as possible. If eating out is something you value, it’s totally okay to treat yourself on occasion. But be sure not to let it spiral out of control because the consequences to your budget are real.

Pro tip: If you want to save a little extra money during your move, try this no eating out challenge!

Step 4: Finding and Securing Housing

The next step in moving out is to find the perfect place and nail down a lease to rent it! This part can take some time, so remember to be patient with yourself. It’s often better to wait a little longer for a good deal on a place you really like, rather than to rush into the first apartment you tour.

You’ll have a few options when it comes to finding a place. You can choose to strike it out on your own and look for an apartment or home to rent for just yourself. You could also choose to look for a bigger apartment or shared home with some roommates. Both have pros and cons, but living with roommates is a great way to save more money on housing because it allows you to split more expenses.

Actually, house hacking is a great option if you’re the entrepreneurial type and have enough cash to buy a place. Your roomates can pay you rent, and this subsidizes your living costs, while building wealth through real estate at the same time. We’re big fans of this approach!

Finding the Perfect Place

Once your budget is sorted, you can start to tour apartments within that price range. Many rentals may even allow you to take a virtual tour, but in person is a better route to take if you can.

You can use websites like Zillow and Apartments.com to find available places in your area. These websites allow you to filter by your maximum price, as well as other features like the number of bedrooms. You could even put out feelers to your friends and family that you’re looking for a place. If you get your apartment through someone you know, you may be able to snag a great discount on rent.

Understanding Lease Agreements

If you’re renting your first apartment, chances are you’ll need to sign a lease agreement with your landlord. Even if you’re renting from someone you know, it’s still important to create a lease agreement that works for both parties.

The application process should be fairly straightforward. Follow the landlord’s lead and fill out whatever paperwork they ask for. Make sure you’re honest and upfront with everything, as you want this relationship to start out on the best foot possible.

Once you get approved, make sure you review the entire lease agreement thoroughly. If you have trouble understanding the language, ask a parent or friend for some help. If you feel you’re being bullied into a contract or they are asking for unreasonable things, walk away. Rental leases are supposed to be win/win arrangements that protect both parties. Don’t sign anything you’re uncomfortable with!

Many renters think that leases are non-negotiable. But that’s not the case! While some terms can’t be changed (like state laws), there are a lot of things in a lease that can be altered. Don’t feel bad for negotiating or asking for things that are important to you.

A great guide you might want to check out is a book called, Rental Secrets, by Justin Pogue.

Know your rights

As a tenant, you have certain rights and responsibilities that differ by state. For example, in certain states it may be legal to withhold rent until your landlord makes necessary repairs to ensure your apartment is habitable.

It’s important to spend some time reading about your tenants rights before you move in to make sure you don’t neglect any essential responsibilities and remain safe. Most states have a landlord-tenant handbook that can walk you through the basics! You can find more information on tenants rights for your specific state here.

Get Renters Insurance

Accidents happen. It’s smart to protect yourself, your belongings, and have some liability coverage just in case. Some leases require you to carry renters insurance (and require the landlord to have landlord insurance). It just protects everyone beyond the lease agreement.

The good news is, renters insurance is quite cheap! A policy averages around $12 per month, and depending on your insurance carrier you might be able to bundle with your car policy for a small discount.

PolicyGenius is a good place to start searching for a policy or getting quotes!

Step 5. Setting Up Your New Home

This part is probably the enjoyable part of moving out – setting up your new place!!! It can be an amazing way to express yourself as you decorate and arrange it in a way that fits your specific needs and lifestyle.

You’ll likely need to bring quite a few items to your new place, and these items can certainly add up in cost. Here’s a list of some essential items you’ll want to purchase (or take from home) before, or soon after you move in.

Decorating on a budget

Decorating your apartment is a crucial step in making it feel like home. Luckily, there are a ton of ways that you can decorate on the cheap. Here are a few tips for saving money while giving your apartment your own personal touch.

- DIY Decor: If you’ve been known to get a little crafty, you can save some serious cash by making your own decor. Grab a few poster boards and go to town with some paint!

- Bring in some plants: Head to your local hardware store and pick up a few hard to kill plants. They’re known for improving your mood, and will bring some much needed life to your new place! You might even be able to propagate plans from your friends – for free!

- Flip Thrift Store furniture: If you have a good eye for finding furniture that just needs a little love, be sure to hit up your local thrift stores. Often, items like rugs, couches or chairs might just need a good clean to make them look brand new.

- Hang up your record collection- If you have any aesthetic belongings, why not let them double as room decor. Things like records, decorative plates, or fancy wine bottles can all become decorations with the right placement. I have a surfer friend who hangs his boards in the living room, using them as art.

- Add some personality to items you need to buy anyway: You need things like shower curtains, rugs, and lamps anyway. Why not get them in your favorite color or print to add some style to your apartment without any unnecessary purchasing.

It can take a while to make a house feel like a home. There’s no rush, so take your time and furnish your place with things you know you’ll enjoy over the long term.

Step 6: Navigating the Emotional Aspect

Don’t get me wrong. Moving into your own space is super exciting, and a major milestone. However, it can be scary sometimes, or even lonely. That’s why it’s important to work on building a strong foundation both at home and in your new community!

Maintain relationships with your family

When I first moved out of my Dad’s house to my first apartment, I’m not gonna lie… I missed seeing him every day! But luckily, we live in the age of Facetime and cell phones, so you won’t need to rely on a horse and cart to deliver your letters.

Whatever your preferred method of connection is, maintaining your relationship with your family is definitely an art. Here are a few of my favorite tips for keeping in touch with your loved ones.

- Have a weekly phone date. When my brother went off to college, he established a set time for calling my family each week, and it helped us to stay in touch despite the distance!

- Make plans ahead of time. If you’re worried about not seeing your family as much, try and make an effort to pencil things on the calendar. You may not feel as far from your family if you know you have a family vacation planned for one month after you move in!

- Give each other grace. You may not talk with your family as much as when you lived with them, and that’s okay. Sometimes, life gets busy and you might hear from them a little less for a while. Make sure to give each other grace, and don’t take it personally. Remember, the phone works both ways.

- Split the distance. If there’s a good amount of distance between your new place and where your family lives, you don’t need to make the long trip home every single time you want to see them. You can always meet somewhere in the middle!

As you continue to live on your own, you’ll find your own groove. It’s only natural that your relationships need to adapt to match how you change as a person.

Develop a Sense of Belonging in Your New Community

It’s important to develop a few relationships in your new community and rub shoulders a little with your neighbors. It’ll make you feel more at home, safe, and give you an opportunity to contribute to something other than yourself. While it isn’t always easy, with a little effort you’ll make friends in your new area and find a sense of belonging.

In my experience, one of the best ways to make friends in a new environment is to look for clubs or social groups that engage in activities that interest you. For example, if you love sports, you could join a club softball team. When you meet people there, you’ll already have a shared interest you can engage in conversation about. Meetup.com is a great site to find in-person group hangs near where you live.

You could also try to “become a regular” at a few places in town. Pick a favorite coffee shop or bar, and hang out in the same place a few times each month. Chances are, you’ll get to know the staff, as well as some of the other regulars. If you’re super frugal, you can even try this at the local library or community parks!

Walking and biking are also great ways to show your face around the neighborhood and meet locals. Not to mention, biking saves you soooo much money vs. driving a car!

Step 7: Perfect Your Frugal Living Skills

In order to make your move sustainable, you’ll need to develop frugal living skills. If you aren’t mindful of your spending, you may not have enough money at the end of the month left to keep living on your own long term.

The good news is, there are a ton of frugal hacks that you can learn easily and implement immediately after moving out of your parents house. Here are a few major ones that will save you a lot of money while living independently…

Cooking and meal planning

Not only is cooking at home great for your wallet – it’s great for your body too! Eating at home is typically associated with having a better overall diet, even if eating healthy isn’t necessarily your goal. You have more power over what exactly you’re eating, and you’ll likely save some serious money in the process.

Even with the rise of grocery costs, you can still use these tips to completely slash your grocery bill!

Eating out isn’t always bad, and there are ways to do it on the cheap!. But learning to cook on the cheap means you can save more money and funnel that into things you enjoy more!

Cheap entertainment

When you move out, you’ll also want to find a few ways to entertain yourself on the cheap. Luckily, with a little creativity, you can pare back your entertainment budget while still having fun and getting together with friends on the regular.

A great way to stay entertained is to start hosting. You spend money on rent every month, why not get the most out of it by turning it into a space that you can enjoy with friends. Instead of going out to a cafe, invite your friend over for a freshly brewed cup of coffee and snacks at your place. Board game nights are always a hit too. Instead of meeting a bunch of friends out at the bar, make some inexpensive cocktails at home!

You can also take advantage of a ton of free activities around your new home. Activities like hiking, going to the library, visiting national parks, and traveling using credit card points are great ways to stay entertained for less.

Bonus- 11 Free Services and Stuff to Take Advantage Of

Enjoying the Great Outdoors

You don’t have to be Bear Grylls to reap the benefits of spending more time in fresh air. Being outside in nature can help to improve our mental health by reducing anxiety and stress. It can even improve your sleep, as you’ll be exposed to more natural light which can help to regulate your sleep cycles. Even better, spending time outside can help you to save some serious cash!

If you can, we highly recommend moving to a part of town that is walkable or bikeable. The average person spends $10,728 each year to own a car, according to AAA. You can significantly reduce these costs by going car-free, or even just by making walking and biking a more significant part of your life. Best of all, you won’t have to deal with as many major inconveniences that come with having car difficulties.

If you’d like to evaluate the walk/bikeability of prospective areas before you move, be sure to check out Walk Score. They rate each town or city on a scale of 1-100 for walkability and bikeability.

Related: Other ways to cut down on car costs

Remember, Less is More

If you’re moving into a smaller space, chances are you’ll learn very quickly that less is actually more. Not only is it often frugal to just own less stuff- it can help to simplify your life and keep your space from becoming a cluttered mess.

My greatest small apartment hack is to try and find pieces that have multiple different functions that can help to reduce clutter and solve a few different problems. A couch with a storage chaise or a storage ottoman can serve multiple purposes, and prevent you from needing to purchase additional chests or storage pieces.

Owning less doesn’t always have to mean cheaping out. For example, you could opt to purchase a good blender that can replace the need for multiple items, like a food processor and a juicer. Or maybe it means purchasing a toaster oven with an air fryer setting so that you don’t need to buy one separately. Keeping your space tidy and not over crowded can help you to keep from misplacing things and needing to purchase them a second time. Plus, the less you buy for your new place, the easier it will be to get organized once you move in.

Step 8: Advancing your career/education

You might love your first apartment, but chances are you won’t want to live there for the rest of your life! If you want to eventually upgrade your space, you’ll likely need to work on advancing your career and education.

You don’t need to go back to school to further your career education. You can seek opportunities for growth at work by asking to shadow people in other departments. Or by asking your boss if your employer will cover any additional courses or job training. You could also consider starting a side hustle to get experience in other industries.

Working towards advancing your career \will ensure that you’re where you want to be by the time you’re considering your next move!

Pro tip: Negotiating pay raises is a great way to advocate for yourself, and continually keep your salary up where it should be.

Step 9: Begin Your Wealth Building Journey

Hurrah! You’re living independently now and being your cool grown-up self. Now what?

It’s time to go from good → to great. Once you’re settled into your new apartment, start thinking about your financial future. What are your goals moving forward? Do you want to buy a house someday? Retire early and travel the world? Move to your dream city? Or maybe you just want to live a humble life and ensure that you’ll have enough money to retire when you’re older.

The more frugal you are while you’re young, the larger the gap between your income and expenses, the easier it will be to retire comfortably later in life.

Prioritize saving for retirement

I know what you’re probably thinking. “I have tons of time before retirement! Why should I start saving now?”

Because of the way compound interest works, you’ll have to save far less now vs. waiting to start until you’re older. Even if you’re really young and only have a few dollars to contribute each month, it can have a tremendous impact on how much money you’ll have when you reach retirement age.

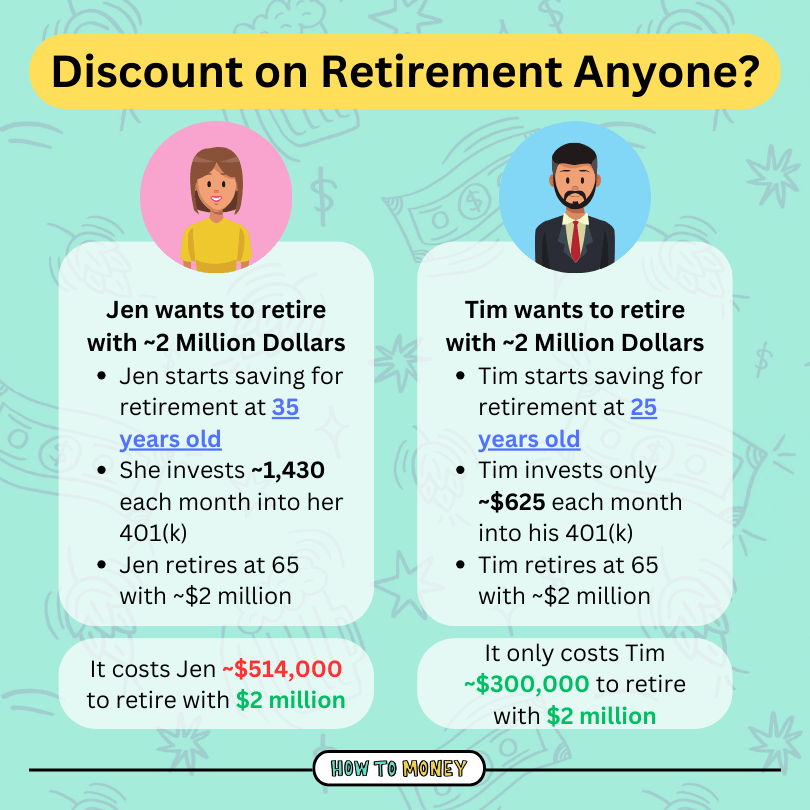

For example, if you start saving for retirement at 25 years old, and contribute $625 each month, you’ll end up with around $2,013,000 dollars at retirement assuming an 8% return. But if you wait to start investing at 35, you’ll need to contribute about $1,430 each month to get near that same amount ($2,014,000).

If starting at 25, you’ll only need to actually save $300,000 to build up that 2 million dollar nest egg. But if you wait until 35, you’ll end up paying $514,800 for that 2 million dollar retirement!

If you start saving now, you’ll actually have to save less in the long run.

Simply put, your dollars are worth way more NOW than they will be in 10, 20 or definitely 30 years time. If you start saving early, you don’t need to save as much!

Becoming Debt Free

It’s also a great idea to focus on slashing any high interest rate debt from your life! In the same way that compound interest can work for you in retirement investing, it can also work against you. Things like credit cards, certain car loans and personal loans have very high interest rates attached to them. You can, and should, learn to use credit cards wisely. But if you don’t pay the balance off on time and in full every month, you’re digging yourself a horrendous debt hole.

If you have any high interest rate debt, now is a great time to come up with a debt payoff plan. With some hard work and persistence, you’ll be able to slash that debt from your life, and enjoy having fewer financial obligations each month.

Start Saving For a Home Down Payment

If you think you might want to buy a home at some point in the future, now is also a great time to start prioritizing saving up that down payment. With the cost of home ownerhsip increasing over the past few years, getting a head start is never a bad thing!

We always recommend saving up a down payment of between 10-20% of the cost of the home if you’re planning on purchasing a single family home without house hacking. That means, if you’d like to purchase a $500,000 home, you would need to save between $50,000-100,000 to buy that home.

When you have a free night, sit down with your favorite drink and start familiarizing yourself with the cost of homes in areas you like. Then, make a plan to save some money after every paycheck towards this goal. If you change your mind and decide you aren’t interested in purchasing a home down the line, you can always use this money for retirement investing, starting a business, or other exciting purchases down the line.

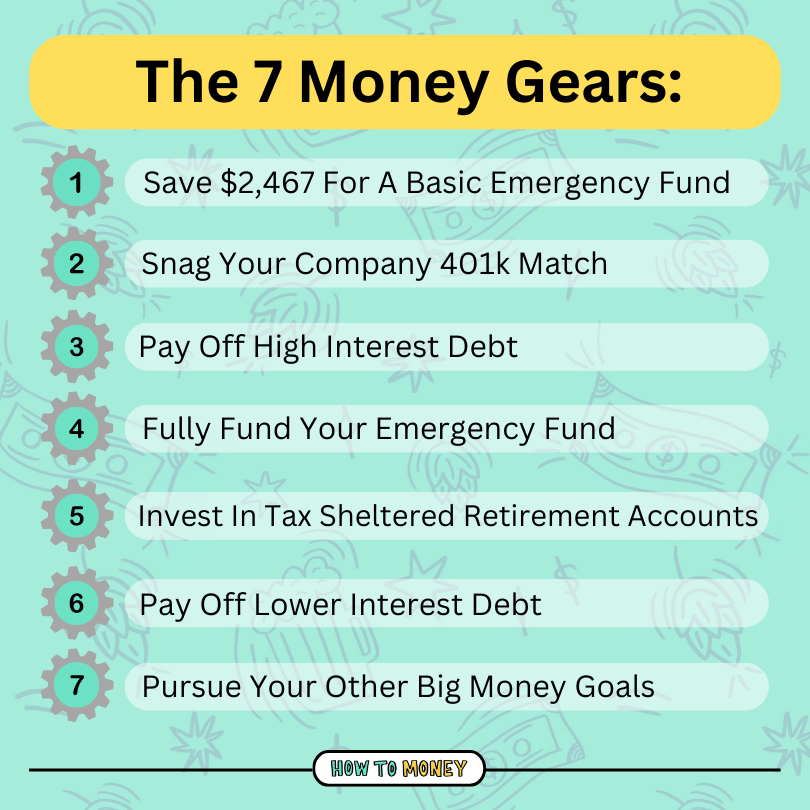

If you feel overwhelmed about which aspects of your finances you should prioritize now that you’re living independently, we’ve created a helpful guide called “The Money Gears.” This helpful article lays out the best order for tackling financial milestones.

Don’t be afraid to move back home if you need to…

I think a lot of people are under the impression that once they move out, they need to keep living independently for the rest of their lives or else they’re a failure. I’m here to tell you that if you need to move back in with your parents at any point, it’s okay (assuming they are cool with is). At different points in your life, it may be the best financial move.

If you need to move back to your parents house, try to make it for a specified time and reason. For example, you can ask them if you can move back in for a year to save up a down payment for a house. Or, if you’ve been laid off and need to move home, give them a time frame of when you’re hoping to get back out there.

Tons of people move back home for different reasons, so if you need to, you’re not alone. Be grateful that you have family that can help support you and enjoy the gift of extra time spent with them.

How Can I Save Money on Moving Out?

When you move out of your parents’ house, things can get pricey. But it doesn’t need to break the bank! With a little creativity, you can save money all throughout the moving out process. Here are 9 tips for saving money while moving out of your parents’ house!

1. Try to get a deal on rent

One of the best ways to save money on a move is by negotiating for cheaper rent. Ask yourself if there is any additional value you can offer your landlord in exchange for giving you a break with rent. Would you be willing to sign a 2 year lease? Help out with some of the yard work? By helping out your landlord, they are more likely to be open to the idea of giving you a good deal.

While this might work best with mom and pop landlords, you may still be able to negotiate with bigger management companies. Maybe they can’t give you a break on the rent, but you could still ask for other things, like free parking or for a pet fee to be waived.

2. Save on utilities

Once you get your first electric bill, you’ll finally understand why your parents were so adamant about turning off the lights whenever you leave a room. 😅

Utilities, like electric, gas and water can certainly add up every month. Luckily, with a little mindfulness, you can save on utility costs. Be sure to check out these posts filled with tips for whittling down your bill.

- 11 Ways to Save Money on Your Water Bill

- 13 Ways to Save Money on Electricity

- 9 Ways to Reduce Your Monthly Gas Bill

3. Skip the moving truck

Is it a little cliche if you ask your friends to help you move in exchange for pizza and beer? Maybe a little bit. But it can still save you a ton of money on moving out. Plus, it’ll probably be a ton of fun anyway!

4. Don’t buy more stuff than you need

You don’t need to fully furnish your new place just to make it look “lived in”. And you definitely don’t need to have it as packed as your parents’ house. When getting started, it’s okay to buy as you go. The longer you live in a space, the more you’ll realize what everyday items you miss, and which things you can go without.

5. Practice paying your rent ahead of time

To get in the swing of managing your finances before you move out, you can practice paying rent in the months beforehand! Just transfer your estimated rent to a high yield savings account each month. When the time comes for you to move, you’ll have a sizable emergency fund saved up as well as be in the rhythm of making monthly payments.

6. Look to local “Buy Nothing” groups

Like they say, one man’s trash is another man’s treasure! There are entire communities of people who are looking to give stuff away for free to people who will use it. Typically, you can find these groups on Facebook by searching “buy nothing” and your area.

7. Skip out on bubble wrap

This one is super simple, but can still save you some meaningful money. You do not have to spend money on bubble wrap to transport your glassware, or more fragile belongings. Just wrap them in soft fabrics you already were planning on moving over there, like towels, linens, or sweatshirts.

8. Ask for Hand-Me-Downs

Before you move, you can also put it out there that you’re open to receiving any hand-me-downs for your new place. Mention to your friends and family that you’re furnishing your home on a budget. Next time they’re looking to toss something, they’ll be more likely to offer it to you first!

9. Consider opening a new credit card

If you have experience with using credit cards, and know how to manage them responsibly, your move could be the perfect time to open up a new credit card and get a sweet signup offer. Most credit cards with sizable rewards will require you meet a minimum spend in order to earn your bonus. That’s why it can be a good idea to time signing up for new credit cards with big purchases.

Choosing the credit card with the best signup bonus and perks for you can be time consuming. That’s why we created a credit card tool that allows you to compare signup bonuses in real time!

It’s worth noting that this life hack is only worth pursuing if you know you can pay off your cards on time and in full each month. If you get hit with interest, it will totally undo any of the benefits of owning these cards. So stay away from credit cards if you have spending problems!

The Bottom Line

Moving out of your parents’ house can be one of the most exciting times of your life! Whether you’re moving to be closer to work or friends, or just looking for a little more independence, living on your own will help you to build valuable life skills.

That being said, it’s so important to plan ahead before your move to ensure things go smoothly. With a little mindfulness and help from your friends and family, you can move out from your parents’ house for the first time without any major hiccups and enjoy your new home.

Related posts: