If you’re living paycheck to paycheck, you’re not alone. In fact, 62% of Americans report living paycheck to paycheck. Some are even high earners, making over $100,000 a year!

Good news though… Anyone, anywhere, at any age, has the power to break away from the exhausting treadmill of living paycheck to paycheck. And in this post we’re going to explain a few ways to do this so that you can start to build wealth and eventually retire more comfortably.

Yes, it’s hard work. Yes, it requires sacrifices and changing your lifestyle a little bit. But I promise you, all of the effort you put in will absolutely be worth it.

What is living “paycheck to paycheck?”

Living paycheck to paycheck means that you depend on each check from your job to meet your monthly expenses. It’s when you’re spending everything you earn, every pay day, never building up savings or accumulating money that you can spare. It means having a 0% savings rate.

For a lot of people, living paycheck to paycheck means that if they lost their job unexpectedly, they wouldn’t be able to pay their rent or buy food. As a result, many folks continue working at jobs they hate because they can’t afford to change employers. This can feel like the opposite of freedom, and has serious detrimental effects on the ability to enjoy life and prepare for the future.

If you continue living paycheck to paycheck for long enough, you’ll almost certainly face challenges when it comes to funding retirement.

On the flip side, getting even just one month ahead financially and building a basic emergency fund can offer you much more freedom and flexibility. And it’ll allow you to feel less stressed, enjoying increased peace of mind. Even though it is difficult, with enough determination and patience it is entirely doable to escape living paycheck to paycheck.

What causes folks to live paycheck to paycheck?

There are a number of different situations that cause people to live paycheck to paycheck. Often it is the result of low wages. A decent chunk of Americans are hard pressed to make enough money to keep up with the increasing cost of living.

But sometimes it can be caused by spending too much. Having expenses that are too high, or failing to live within your means. We live in a world that promotes consumerism and lifestyle creep. As soon as folks get a raise at work or have a financial windfall, they find a way to spend that money and keep none of it.

Combine all this with a lack of financial education in schools and we’ve got the magic formula for living paycheck to paycheck.

How to Stop Living Paycheck to Paycheck

OK, now let’s get to the steps you can take to break the cycle and create more margin in your life. You don’t need to tackle all of these things at once… the key is to take your time and remain consistent.

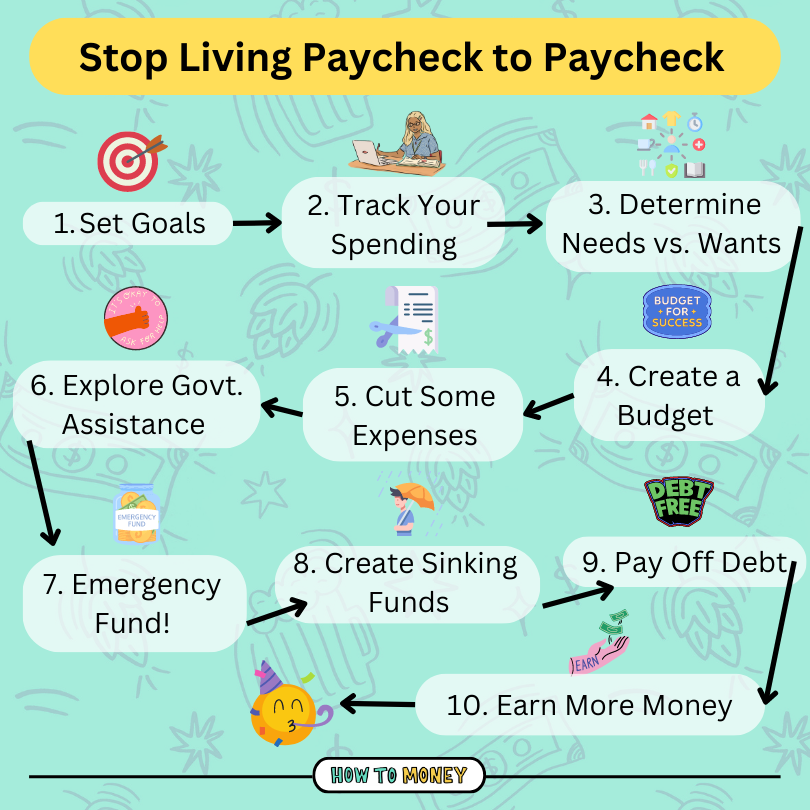

1. Set Goals

The first step towards breaking the paycheck to paycheck cycle is to get clear about your money and life goals. Having an idea of what you want your life to look like in a few weeks or months can help motivate you to stay diligent with your money. Without these crystallized goals it’s too easy to fritter away money on less meaningful things.

A good first goal to shoot for can be to save up a basic emergency fund. Economists have found that having $2,467 in savings can help you cover most surprise expenses. Just knowing that you have enough to pay for small emergencies that might pop up can help to significantly lower your financial stress levels.

Another good goal to have is to save up one month’s worth of expenses so that you can pay this month’s bills with last month’s money. That’s known as ‘aging your money.’ Like a fine wine, your money gets better with age. Or, look into the Pay Yourself First strategy. And once you’ve done that – voila! You’re no longer living paycheck to paycheck.

After that, the next big goal you can shoot for is to have an emergency fund that will cover 3-6 months worth of expenses. That way you’ll be protected from larger surprises, like job loss or medical emergencies.

Not sure where you should start? Be sure to check out these money gears for some advice on which steps you should tackle next on your journey to financial independence!

2. Track Your Spending

Next, it’s time to figure out exactly where your money is going each month!

It’s a good idea to gather roughly three months of bank and credit card statements and start to look at how much you’ve been spending and on what. Actually taking the time to crunch the numbers can give you a lot of valuable information and insight moving forward. Expense tracking will also give you quick ideas on where cutting back will make the most impact!

Warning- what you find might shock you! Personally, I was bewildered to find once that I spent over $400 on eating out for multiple months in a row! 😳 Needless to say, this shock went a long way in motivating me to cut back my spending on takeout.

Try to identify a few categories of spending that could be reigned in, and a few categories where you’re crushing it. Seeing your good habits in action can be motivating also.

Pro tip: Free apps like Credit Karma and Empower can automatically track and categorize all your spending. This truly doesn’t have to be a dreary mundane task every month.

3. Determine Needs Vs. Wants

Now, go through the purchases you made and break them into the categories of needs vs. wants. Needs are things like housing costs, utilities, food, insurance and transportation. Wants are for pretty much anything else.

In order to create a savings cushion as fast as possible, it can be helpful to switch to a bare bones budget temporarily, which consists of only your needs. Getting disciplined and cutting all discretionary spending is not sustainable over the long-term, but it can help you to create some margin fast.

You can always start to incorporate those wants back into your budget over time as you continue to make progress. But this is a ‘no pain, no gain’ scenario we’re dealing with here.

4. Create a Budget

Next up, it’s time to create a realistic budget you can stick to long term to create some serious savings over time.

Lots of people think that budgeting = zero fun. But that’s truly not the case. Budgeting gives you the freedom to spend on the things you’ve said are important to you without feeling guilty. It also ensures that you’re living your life in an intentional way, spending on things that bring you joy.

Creating and sticking to a budget will ensure you aren’t spending more than you earn. Over time, this will accrue into savings that can completely change your life.

One of the simplest budget types is called the 50/30/20 budget. This is when you split up your wants, needs, and savings goals, assigning a percentage of money to each one.

Is saving 20% enough to reach your financial goals? That really depends on your age. Here’s a guide to figuring out how much of your paycheck you should invest.

5. Cut Expenses

Every year it seems our cost of living gets more and more expensive. Thanks, inflation! That’s true even when we aren’t actively upgrading our lifestyles. But you don’t have to just lie down and take it!

It’s time to call all your service providers, like your utility companies, internet and phone companies, and also insurance companies and ask them for a discount. Find out if they have any introductory offers they can give you. Sometimes, it can be helpful to ask for the “customer retention department.” The folks in that department often have more leeway.

And if they won’t lower your costs, it’s time to shop around for better rates. A lot of the time we avoid these things because we think it’s going to be more trouble than it’s worth, but we promise you it is worth the time and effort.

For example, if you switch your $70 phone bill to a $30 unlimited plan from Mint Mobile, you will save $40 per month. While this doesn’t seem like much, given the rule of 173, this all adds up to a whopping $6,920 in 10 years if you invested the difference. Small amounts really do add up!

Taking the time to lower your monthly expenses by slashing your bills can give you the money you need to start your emergency fund.

Related ways to save money:

- 14 Fun Money Challenges to Jumpstart Your Progress!

- The best cheap cell phone plans

- How to negotiate your bills

6. Get Some Help

Another way to temporarily lower your expenses is to get some help from nonprofits and government resources. There is absolutely no shame in taking advantage of these. If you qualify for them, they were made to help you. And once you’re in a better position, you can help to pay it forward by donating time or money in the future.

If you’re struggling to pay your student loans, you can apply for an income driven repayment plan to help lower your payments, or apply for forbearance. Just call your student loan provider and ask them to talk you through your options.

There are also plenty of government programs that can provide you with assistance when you are struggling. Programs like SNAP, Medicaid, subsidized housing, low income home energy assistance, and Welfare can help you to cut your expenses temporarily so that you can build up your savings.

Make sure to watch out for scams if you’re looking for help paying off debt. Anyone who promises they can get your credit card debt forgiven or obliterated is lying. Run away! If you’re struggling with debt, you can also get free credit counseling from Money Management International or the National Foundation for Credit Counseling. These non-profits serve people who have credit and debt issues. They can also help you to come up with a plan to repay your debt.

7. Start an Emergency Fund

Now that you have some extra cash each month because you cut some of those recurring expenses, it’s time to sock away that extra money for emergencies… But where should you keep this money?

A great place to keep your emergency fund is in an HYSA, or “high yield savings account.” These bank accounts typically give you 10x the national average interest rate. And they don’t charge you any of the weird fees that the big banks do.

This extra interest earned can help to hedge your savings against inflation, which would otherwise chip away at those dollars!

Here is our full post on how to build an emergency fund and ways to boost your savings.

8. Start Sinking Funds

Now that you’ve built up some margin, we want to set up your life to ensure that you won’t fall back into the cyle of living paycheck to paycheck. An important way to protect yourself against needing to take on debt for irregular expenses is to create sinking funds.

Sinking funds are stashes of money you save for expenses that don’t fall on a monthly, or even annual schedule. They are a way to plan for those things you know you’ll have to pay for, but you don’t know exactly when you’ll have to pay for them.

Sinking funds are great for things like home and car maintenance, holiday gifts, and health expenses. You can even use them to save up for fun stuff, like vacations, a wedding, or clothing.

Creating sinking funds is really easy. Just take your goal savings amount for each category, and divide it by the time in which you want to have the funds saved up. For example, if you want to save up $1,200 for a family trip in a year, you’ll budget $100 towards this sinking fund every month.

And where should you keep these funds? Also in a high yield savings account. Higher interest paid, fewer fees. Need I say more?

Having sinking funds ensures that you won’t dip into your savings account or go into credit card debt just to cover an irregular expense. That’s what we want you to avoid.

9. Prioritize Paying off Debt

Another way to free up more of your money is to prioritize paying off high interest debt. The sooner you are able to pay off this debt, the less money you will pay on it overall.

Take some time to get together a debt payoff plan. Two tried and true ways of kicking that debt in the butt are the debt snowball and the debt avalanche methods.

The debt snowball has you tackling the smallest debts first, to get some quick wins under your belt. The debt avalanche route has you paying off the debt with the highest interest rate to save you the most money over time.

You’ll be amazed at how much more you can save with less monthly payments siphoning from your bank account.

10. Earn More (And Save the Excess!)

Lastly, it can be helpful to look for ways to increase your income.

We put this last on the list, intentionally. Because earning more won’t stop you from living paycheck to paycheck if your expenses increase simultaneously with it. So, it’s important that you master the other tips in addition to increasing your income.

There are a lot of different ways you can work to make more money. The fastest way to make more is to consider asking your current employer for a raise. However, if a raise at your job is out of the question, it’s worth considering switching employers to earn more money.

If finding a better paying job isn’t possible for you at the moment, you can spend some time working towards improving your skills. There are tons of free classes and certification courses you can take online. You can also see if your current employer offers any educational benefits.

Lastly, you could consider starting a side hustle to earn extra money on your terms! If you’re in a relationship, you could even work on starting up one of these 15 side hustles for couples.

The most important thing is that you don’t let lifestyle creep steal your extra income. Make sure to stash that extra cash and put it towards your savings goals.

It’s Time to Break the Cycle

If you’re living paycheck to paycheck, your financial situation won’t likely change overnight. But with hard work, determination, and a little patience, you can break the cycle. You’ll no longer be stressed when unexpected expenses pop up, have more money to spend on the things you love, and enjoy more peace of mind.

Building wealth isn’t about how much money you make. It’s about how much you KEEP. By slowly lowering your expenses, increasing your income, and investing the difference, you will escape living paycheck to paycheck and be well on your way to building a solid financial future.

Well, that’s all we have to stay about that! And remember, if you’re ever in need of some help, you can always submit a listener question to HTM here!

Related Posts:

- 27 Ways to Save Money- In All Walks of Life!

- How to Stay Out of Debt, Forever

- 8 Things to Consider before Investing

Advertiser Disclosure

* Advertiser Disclosure: How to Money has partnered with CardRatings for our coverage of credit card products. How to Money and CardRatings may receive a commission from card issuers. Some or all of the card offers that appear on the website are from advertisers. Compensation may impact on how and where card products appear on the site. Lastly, the site does not include all card companies or all available card offers.