There are numerous ways you can pay off your mortgage early. And all of them fall under three main strategies…

- Making extra payments to your loan principal

- Restructuring your loan to allow faster pay off

- Investing elsewhere, then paying off the mortgage in a lump sum

In this post we’ll dive into each of these concepts, and talk about the multiple ways you could execute each strategy.

We’ll also cover other things you should consider before paying off your mortgage early, because it may or may not be the right move for you!

OK, let’s dig in…

Ways to Pay Off Your Mortgage Early

All of these strategies require hard work and perseverance. But here’s the good news: Compound interest is on your side!

Even the smallest changes can really add up over long periods of time. You can shave YEARS off your mortgage by making just a few adjustments to your payment strategy.

1. Make Extra Loan Payments

It’s no secret that additional payments to your principal balance will allow you to pay off your mortgage quicker. By reducing how much you owe, it lowers the interest charged, which creates a snowball effect, shortening the payoff schedule.

Here are common strategies and examples that result in paying your mortgage off early:

Make biweekly payments instead of monthly:

Most mortgages are set up on a monthly payment schedule, usually deducted from your bank account on the same date every month.

But instead, if you set up a recurring transfer every two weeks (for half the monthly mortgage payment amount) you’ll end up making 26 x ½ payments each year instead of 12 full payments. At the end of 12 months, you’ll have actually made 13 monthly payments, resulting in 1 full extra mortgage payment per year!

This may seem small, but that extra payment each year is applied directly to your principal balance. And so it gives you a huge advantage in paying off your mortgage early.

For example: Given a $500,000 mortgage for 30 years, and a 6.5% interest rate, bi-weekly payments would mean shaving 5 years & 11 months off your payment timeline!!! That mortgage will be paid off almost 6 years early!

The beauty of this strategy is if you can set up the bi-weekly payments on the same day as you get your work paychecks, you’ll likely feel no difference in your monthly budget.

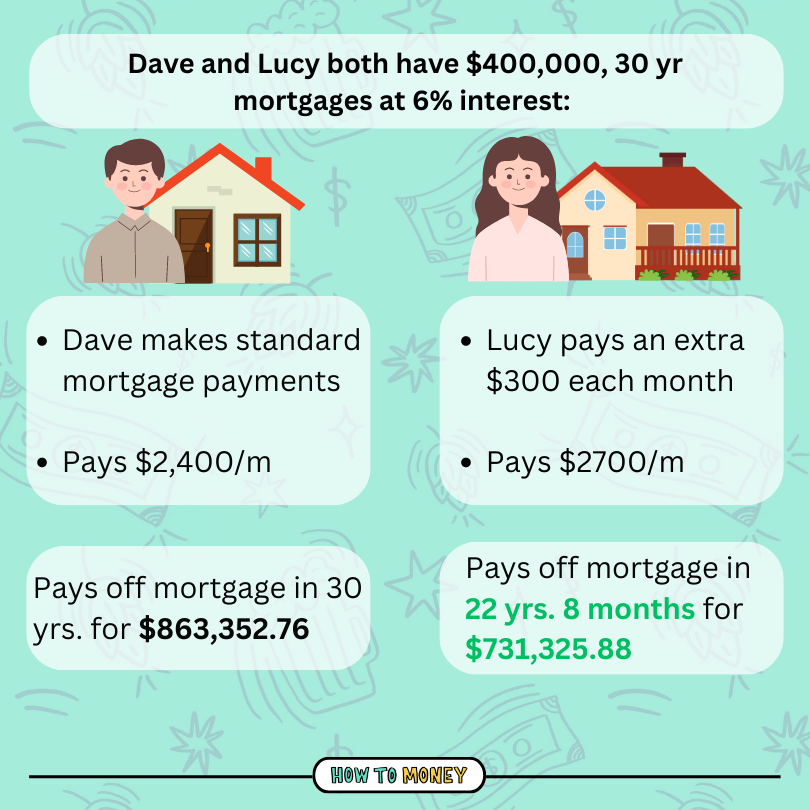

Round Up Your Payments:

Another strategy you can take is to round up your monthly mortgage payments each month. For example, if your mortgage payment is $1700 per month, could you round it up to 2,000? That extra $300 each month put towards your mortgage means an extra $3,600 paid off each year.

For a $275,000, 30 year mortgage, those extra payments can result in you shaving nearly TEN YEARS off your mortgage. That’s literally an extra decade of your life that you get to live mortgage free!

Need to find the extra cash to put towards repayment each month? Check out these 7 Ways to Save More Money This Week!

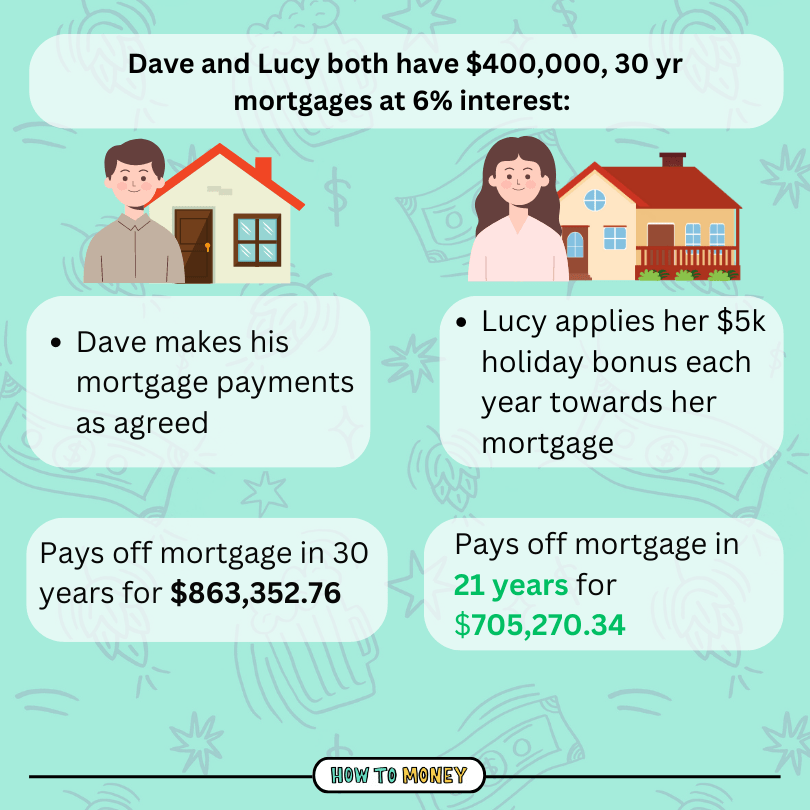

Apply Lump Sums and Annual Bonuses:

Not sure what to do with your annual bonus? An unexpected tax refund? Inheritance or other windfall? Why not throw it at your mortgage to cut back on meaningful time paying it down?

Applying a $2,000 bonus every year could cut down a 30 year, $300,000 mortgage by 5 years and 11 months. Even applying a one time inheritance of $5,000 would save an entire year and 5 months!

OK, you get the point! Throwing any extra money into your mortgage whether it be monthly, annually, or even just once will help you pay off your mortgage early.

Pro tip: Ownwell is a company that helps negotiate a lower property taxes for homeowners. They can save you hundreds or even thousands in property taxes — then you can put all those savings into more mortgage pay off. Check out Ownwell!

2. Refinance Your Mortgage

The main goal of refinancing a loan is usually to reduce your monthly mortgage payments. This can be done by taking advantage of a lower rate vs the one you currently have, or extending the loan term to result in much smaller payments.

You might be wondering, “Why would I start a new 30 year term if I’m trying to pay off the mortgage early? Wouldn’t refinancing make it longer to pay off?

Well, the secret to this strategy is actually keeping your original payment amount going, despite having a new lower monthly payment.

For example: Let’s say your current monthly mortgage payment is $3,000 per month. And let’s say there’s a new mortgage plan available that will drop your monthly payment to $2,500 per month. By refinancing, you’ve effectively freed up $500 in monthly expenses that you can re-apply directly to your mortgage principal.

By keeping your original payment, all the additional money will be applied to the mortgage principal and potentially shave years off of the timeline.

Refinancing your mortgage is a big decision, because you can’t “undo” it later if you decide it wasn’t a good move. So you’ll need to really work the math to make sure it will help in paying off your mortgage early. Current market dynamics, a quick ascent in mortgage interest rates, means that refinancing makes sense for very few folks right now though.

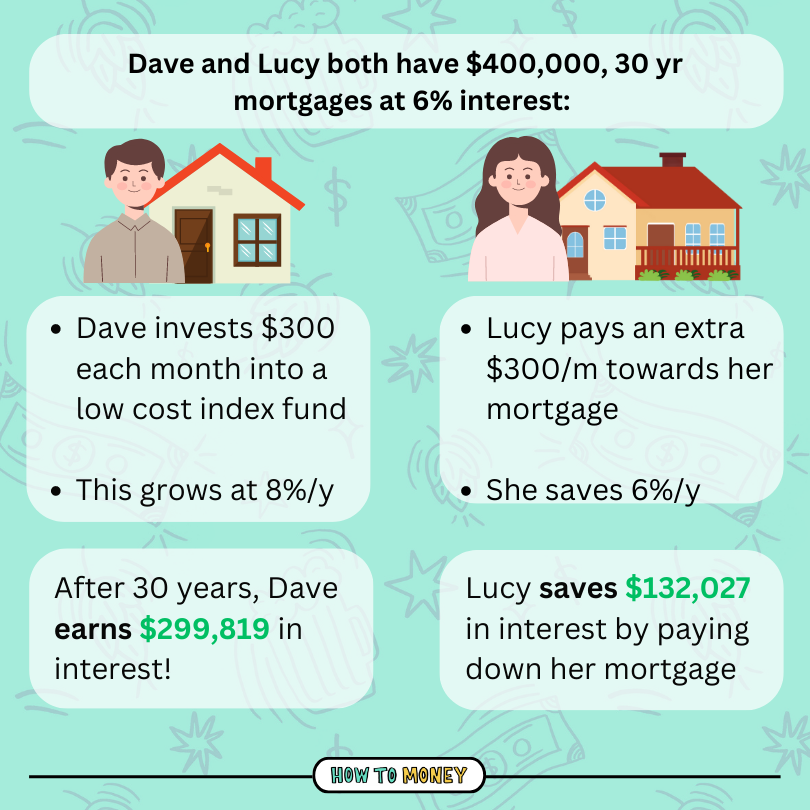

3. Invest Elsewhere for Higher Return

If you only want to pay off your mortgage early from a numbers standpoint, you might want to think twice.

When you make extra payments on your mortgage, you’re essentially giving yourself the same percentage return on your money as your mortgage interest rate. For example, if you’ve got a 4% interest rate, any extra money you put toward that mortgage payoff earns you a 4% ROI.

Depending on the mortgage rate you’ve currently got, you may actually be able to get higher returns by investing elsewhere. You might even be able to get a better return in savings too!

For example: If you have a mortgage right now with a 4% interest rate, it might be smarter to put any additional savings into a high yield savings account. A HYSA could pay you in the neighborhood of 5%, so you’d be getting a 1% better ROI on your savings vs. putting that money into extra mortgage payments.

By earning a higher ROI on your savings, you can grow wealth more quickly. This gives you options for lump sum mortgage payoff later in life!

Putting some of this spare cash that would have otherwise gone to pay off your mortgage into a broad stock market index fund could be smart, too. While this strategy does involve risk, it also has a higher probable return over the long haul. The stock market has averaged ~10% over the last 30 years, which is much higher than most people’s mortgage interest rate.

Benefits of Paying Off Your Mortgage Early:

It’s important to consider all the pros and cons when making additional debt payments. Here are a few benefits that come with crushing your mortgage early.

Save Money on Interest

The sooner you pay off your interest, the less you’ll pay in interest overall. For example, if you put an extra $500 a month towards your $400,000 mortgage, you’ll save over $182,000 in interest, and pay off your mortgage 10 years and 5 months early.

Increase Your Cash Flow

Once you finish paying your mortgage off, you’ll have more discretionary money in your budget each month. You can then put all that cash towards investing, retirement, or fun things like vacations!

Build Equity in Your Home

When you pay down your mortgage, you build equity in your home. That means that once you pay off your mortgage, you own your home outright.

More Financial Stability

Housing costs are usually the biggest line item in our budgets! Having no monthly mortgage payment means that should you lose your job or suffer a financial setback, you have a much smaller monthly debt obligation to worry about, reducing your financial risk.

More Peace of Mind

Owning your home can give you added peace of mind because the possibility of foreclosure is completely off the table. Plus, it’ll be easier to weather any financial hardships without having a monthly mortgage payment.

Downsides of Early Payoff:

Believe it or not, paying off your mortgage early does come with a few downsides. Here are a few cons to consider before taking the plunge into early mortgage payoff.

Lose Tax Deductions

Mortgage interest can be tax deductible, up to a certain IRS limit. So if you pay off your mortgage early, you could lose this tax break. This really only applies if you itemize deductions on your tax return (less than 50% of folks do because the standard deduction is usually higher), so it may not be an applicable benefit.

Miss Out on Other Investment Opportunities

Depending on your interest rate, you may be able to get a better return on your money by investing in other assets like stocks, bonds, and even sometimes in a high yield savings account. Putting extra cash towards your mortgage can result in you having less money to save and invest for your future.

Loss of Liquidity

Once you send a mortgage payment to the bank or credit union, there’s no going back. So not only do you miss out on other savings or investment opportunities, you’re also less liquid from a cash perspective, which limits other potential options too.

Prepayment Penalty

Before you pay off your mortgage early, be sure to read your mortgage contract carefully. Some mortgages have a significant fee for prepayment!

So, Should You Pay Off Your Mortgage Early?

I know you probably came to this article looking for a straightforward answer, but the best one we can give you is… maybe? Both strategies have benefits.

Ultimately, there is no single correct answer as to whether or not to pay off your mortgage early. Because that decision highly depends on your personal situation and your mortgage terms.

Here are a few more factors to consider:

Your goals in life: When deciding whether or not to be debt free, check in with your money goals and evaluate whether it’s part of the plan. If you have other more urgent money goals, like saving for a downpayment for a rental property, or creating a sinking fund for having that first baby, maybe it makes sense to hold off on making extra mortgage payments until you have achieved those near-term goals first.

Your financial situation: Will putting extra money towards your mortgage put a strain on your budget? Will it prevent you from adequately investing for retirement? If so, it might be best to just pay your mortgage as agreed.

Your risk tolerance: Are you comfortable risking missing out on the potential returns from other investment avenues? Depending on your mortgage rate, your home loan could be considered “good debt”.

Are you choosing between debt paydown and increased consumption? If so, even if paying down a 3% mortgage isn’t the most optimized financial choice, it might still be best for you from a behavioral perspective. Running the numbers is important but it’s also crucial to know your own tendencies!

The Bottom Line:

Paying off your mortgage early can be the right move for a lot of folks. You’ll save significant amounts of money on interest, enjoy more peace of mind, and increase your cash flow once you own your home outright.

However, this may not be the right move for those who have other important money goals. Or for those who need to focus on saving more for retirement. That’s why it’s important to evaluate your personal situation and crunch the numbers to decide if paying off your mortgage is the right move for you.

Well, that’s all we have to say about that! Be sure to check out these related posts for more helpful info about mortgages.

Related Posts: