Combining finances with your partner can produce bountiful benefits to both your relationship and your overall financial trajectory. Merging money forces you to communicate more, helps with financial goal setting, and enables you to hit investment milestones faster because you’re approaching your finances in two-player mode!

That being said, merging money isn’t for everyone. It requires a lot of trust, giving up individual control, and it could also potentially lead to arguments.

There’s no one perfect method to manage finances as a couple. Rather, each couple should work to build a custom system that serves their situation best. In this post we’re gonna run through a few high level examples of commonly used systems, and hopefully you can walk away with some good ideas to create your own financial management system.

Getting on the same page…

About 95% of combining finances with your partner is communication. Only 5% is tactics and specific action. For the best odds of managing finances together, focus on setting up a healthy foundation for communication.

It can take many years to get on the same page financially with a partner (especially if you come from completely different money backgrounds!) I know you might be anxious to start opening shared bank accounts dividing budgets, and saving for gargantuan goals, but hold your horses for a sec… Think of this project like steering a huge ship – it’s better tackled in small increments vs trying to change course abruptly. Good things take time!

With that in mind, here are a few things to consider as you begin to combine finances with your partner…

Learn about their current system

You might run your budget one way, and they might prefer to do things quite differently. Before you judge them on all the things wrong with how they manage money, think about some of the good things that your partner brings to the table.

When you combine your finances with a partner, you both need to ditch your individual systems and create a new, shared system. If you learn all you can about each other’s current ways of money management, you can each bring the best of both worlds into your new system, engaging with each of your respective views and beliefs.

Discuss your values

I’m a big believer in matching your budget with your values. When you spend money as a couple, the goal is that all of those dollars to be spent on stuff you both really value in life! So before you create a joint budget, make sure you chat about your mutual (and individual) values. This makes things so much smoother as you combine finances with each other.

Here’s a great example: One of my biggest values in life is giving (i know, sounds cliche – but I love helping friends and even strangers out financially). Anyway, before my wife knew this was a strong value of mine, she sometimes had a hard time understanding why I liked giving my (our) money away. Without knowing the reason, it confused her. But as we discussed more about our individual values, she came to agree that giving should be a necessary part of our shared budget.

Discussing values is a huge part of combining finances with your partner. Actually, money aside, it’s a healthy part of a long-lasting relationship in general. 😉

Discuss your financial dreams

When you’re both in your 70’s, what kind of life do you want to be living? What do you hope your finances look like for your family?

In the short term, what are your big savings goals? Buying a house, saving for kids’ education, perhaps traveling the world together?…

By discussing your dreams (and regularly revisiting them), you and your partner can put specific plans in place to make sure those dreams become a reality.

Talk about money, regularly

As awkward as it might be in the beginning, getting ‘financially naked’ needs to happen in order to combine finances with your partner seamlessly. The sooner these in-depth conversations start happening, the better.

You don’t have to make every conversation about money and base your whole relationship around it. But, in general, the more you talk about money, the more on the same page you will be financially. Having financial date nights regularly will bring you closer financially. Here are some tips to get you and your partner started.

Be honest about income, debts, investing, etc.

You can’t build trust with your spouse if you hide things from them. As painful as it might be, you have to be completely open and honest about all the incoming and outgoing funds.

If you’re bringing a lot of debt into a relationship, that’s OK! If your income is low and you don’t think it will significantly increase anytime soon, that’s OK too! The more transparent you are with your financial situation, the more successful your marriage will be. Bad news is better than hidden secrets. The whole point of a partnership is supporting and helping each other through difficult times. Not hiding things and suffering alone.

Financial infidelity is a real problem in this day and age. And it’s one of the leading causes of money fights, often leading to divorce. Long story short, don’t keep secrets from your partner – financial, or otherwise!

Strive for Financial Equality

Just because one partner makes more money than the other, it doesn’t necessarily mean they get more of a say in how joint expenses are divvied out. While equal income might not be common in relationships, (one partner usually makes more money than the other), that doesn’t mean it should result in relationship inequality.

Every relationship is different, and every couple will have slightly different ways of making financial decisions. But it’s important not to assume by default that higher income means higher ranking when making family money choices.

When you combine finances with your partner, each person needs to embrace the other as an equal financial partner. It’s ok to keep separate accounts for personal spending money. But for the big stuff, it’s crucial to approach big spending decisions together as a team. No matter who brought the money in.

Tactical Steps to Combine Finances with Your Partner

Ok, so we’ve covered the communication pieces and foundational steps to strengthen financial teamwork. Now let’s get to some of the tactical (nerdier) stuff.

Much like individual finances, you’ll need to make a budget, build up an e-fund, and start tracking your expenses and net worth as a couple. Here are the steps in more detail:

1. Create a Shared Budget

If you don’t budget currently, I strongly suggest you start. It’s really easy to save money when you’re single and have disposable income. But when you combine finances with a partner and begin to form a family, disposable income suddenly seems harder to come by.

Budgeting is basically making a plan for where your money goes. It should cover all of life’s necessities (bills for housing, food, insurance, cars etc), as well as luxuries and desires for each person (hobbies, entertainment, guilty pleasures). But perhaps the most important part of budgeting is making sure that retirement funds are being set aside. In fact, couples should prioritize “paying themselves first”, before any other money is spent.

If you’re new to budgeting, I suggest starting with the 50/30/20 budgeting system. It works like this:

- 50% of your combined income is spent on Needs

- 30% is split up for Wants

- 20% of your income is set aside for long term Saving & Investing

Remember, this is different from making a personal budget, because you’re now budgeting as a couple. It’s really important to have your partner’s support 100% in creating a combined budget. Their needs and wants must be covered just as much as yours. This will involve some give and take.

BTW – a much more modern way to share a budget is with the help of a budgeting app. We highly recommend You Need a Budget (YNAB), which helps couples get their finances in order and save better together. They have a 34 day free trial which you should definitely check out!!!

2. Build a Joint Emergency Fund

Contingency planning as a couple is a little easier than as a single person. That’s because since you’ve formed a duo, there’s some additional resilience built in because you’ve got two separate incomes coming in.

Looking at your joint budget, work out how much you’d need to save to build up an e-fund. 3-6 months worth of living expenses is the ideal amount to have on hand. It can can cover anything from a small emergency (like a car repair) to a larger crisis (one of you gets laid off unexpectedly).

How and where you save the money is up to you both to decide. The important part is to communicate with each other and make sure those emergency plans are solid. Not being prepared for financial disasters could jeopardize your joint financial situation, setting your goals back months, or worse, sending you headlong into high-interest debt products.

Personally, my wife and I have about 4 months of savings set aside in a High Yield Savings Account. We’ve withdrawn funds from it a handful of times over the past 10 years, and then replenished it after saving more. Our emergency cash earns some interest each year, which is nice. But probably the best part about having a full emergency fund is sleeping peacefully at night, knowing we can pay for an emergency if our kid breaks a leg or something crazy!

3. Create a Shared Net Worth Statement

One of the coolest parts about combining your finances with your partner is figuring out your shared net worth (and tracking it as it grows over time!)

This means adding up the value of both you and your partner’s personal assets, and subtracting each of your liabilities.

Here’s an example of a shared Net Worth Statement, using a totally made up couple called John and Sarah:

| Sarah’s checking account | $7,000 |

| John’s checking account | $13,000 |

| John’s Roth IRA | $12,000 |

| Sarah’s 401k | $19,000 |

| Sarah’s Rental Property | $240,000 |

| TOTAL ASSETS | $291,000 |

| John’s Car Loan | -$36,000 |

| Sarah’s Mortgage | -$180,000 |

| TOTAL LIABILITIES | -$216,000 |

| TOTAL JOINT NET WORTH | $75,000 |

Here comes the cool part: Combining forces and pooling resources can help you both crush your financial goals at a faster rate! Since you and your partner have aligned interests, it makes sense to “team up” and tackle money problems together.

For example, let’s say John’s car loan in the scenario above has a really high interest rate. This debt is working against them both trying to build wealth as a couple. So, both John and Sarah make a plan to throw all their excess savings at John’s car loan balance. By smashing that high interest debt out of their life, they can move quicker into other wealth building opportunities.

More Ways to Increase Your Joint Net Worth

When you fully combine finances with a partner, you get to take advantage of each other’s strengths (and support any individual weaknesses) to progress faster, together.

There are several ways to increase joint net worth:

- Buy more assets (save/invest more)

- Pay down debts (begin with high interest loans)

- Maximize tax advantages (retirement accounts, file taxes jointly, etc)

As a couple, you may have access to two different workplace retirement plans – like a 401k or 403b. This gives you double the opportunity to sock away pre-tax money than you did as a solo saver. Same with Roth IRA accounts, each person can have their own account which helps you invest more money tax efficiently.

If one partner has already maxed out contributions to their own account, they can consider then helping their partner contribute more to theirs.

Every couple’s situation is different, so it’s important to figure out the most advantageous money moves for your relationship. That’s why open and honest communication should be a regular activity – it helps you identify the best game plan for both of you!

Personally, my wife and I share an Empower account (this app used to be called Personal Capital). It’s a free app that tracks out joint net worth by connecting to all our bank accounts, credit cards and investment accounts. Both my wife and I have access to view everything in a shared login, which keeps things transparent and builds trust in our relationship.

4. Establish a Banking & Bill Paying System

The next action step to combine finances with your partner is to figure out a cash flow system to manage money coming in and out of your lives…

Keep in mind that nothing is set in stone. Things will change over the course of your relationship and as your family changes shape. Brand new relationships might start with a small merge of some budget items (like splitting rent 50/50 or having 2 separate cars), then as they stay together longer they might naturally begin merging everything completely (all income and expenses are shared).

Every relationship has different dynamics. So it’s best for couples to develop a system they are comfortable with rather than just copying how other people do things.

Here are 3 high level examples of systems to combine finances with a partner or spouse:

1. The “Share Everything” Approach:

My wife and I currently use this system. We merged finances relatively early in our relationship and never looked back. All money that comes into our life, no matter who earns it, belongs to both of us. It pays for our household bills, funds our lifestyle, and helps us save for our joint retirement.

All income gets funneled into “shared accounts.” Whether you keep these in your individual names or have joint name accounts is up to you. This will differ depending on whether you’re married or not, how long you’ve been together, or how convenient it is. (You might want to research local laws and consider the ramifications if there is a partnership split). But the concept in this shared approach is that all money is assumed to be owned by both partners, no matter whose name the accounts are in.

Next, household expenses get deducted from these accounts, as well as personal spending. Setting up auto-payments for any credit cards you possess is a good idea to help simplify the process.

For retirement savings, this can be done with tax-advantaged retirement accounts (deducted before paychecks like 401k), as well as after-tax savings vehicles, like Roth IRAs.

Here’s a high level example of what the flow of money might look like:

Pro tip: Since personal spending (think: hobbies, small splurges) are taken out of joint accounts, it’s a good idea to establish a spending limit rule with your partner. Something like “for any purchases over $100, we should check with each other first”. This builds trust on both ends and keeps the shared system fair.

Pros and cons:

By sharing literally everything, there is no “my’ or “your” money. Everything is “ours”, so all financial decisions can be made equally. Budgeting is also much easier with a complete merge of finances because there’s only one set of books to manage!

This system is perfect for single income families, because it allows for a breadwinner to cover any shortcomings in the other partner’s income. Or, it’s great for couples in which one partner has a real passion for personal finance and can “take the reins” of managing money. (Personally, my wife hates budgeting and dealing with money so she prefers that I manage our entire financial life).

However, sharing everything requires complete transparency and trust. Couples that want the freedom to spend money in complete privacy have no place to do so. Also, if one partner spends much more than the other, this can lead to resentment if it’s not communicated properly.

It’s scary to completely combine finances with a partner this way. And you have to be ready to give up control. But ultimately, this ‘merge everything’ system is the most efficient route and something most families should strive for.

2. The “Split 50/50” Approach

When couples first move in with each other, all of a sudden they have shared expenses. This can be an abrupt change for someone who’s been flying solo with their finances their whole life. So sometimes the easiest way to begin sharing money is by splitting bills 50/50.

Moving in together and sharing costs is actually an awesome time in a couple’s journey, because you can both save a lot more of your incomes. It’s cheaper paying for one house vs. two!

Here is what a visual cash flow diagram would look like:

This system involves each person maintaining their own personal budget and finances, as well as contributing to a shared fund for mutual expenses. Personal spending is completely separate, as well as retirement savings and emergency funds.

Pros and cons

Splitting costs 50/50 is “fair” to each person as individuals, because both parties need to financially contribute to the couple’s lifestyle. Also, both parties get complete control of how they personally spend and save money. It’s a great place to start for newbie couples when they first combine finances with their partner and begin to share costs.

But, over time, downsides will start to emerge because this system is dependent on always having two incomes. Problems start to occur when one partner doesn’t earn enough to contribute their half, or, if one of them wants to drastically inflate their lifestyle and the other person doesn’t agree.

Another long term downside of budgeting this way is that one person could grow wealth faster than the other. If one partner is incredibly frugal and a disciplined saver/investor, they will naturally build up a comfortable nest egg for retirement. The other partner may not save enough, meaning they won’t have the same luxury of comfortable retirement.

Furthermore, maintaining separate budgets is pretty inefficient.

Some couples share costs 50/50 and maintain separate money accounts for decades. And if it works for them, that’s great! As long as regular communication is taking place, and the couple is meeting all their personal and shared financial goals, this system can be a successful way to manage joint finances.

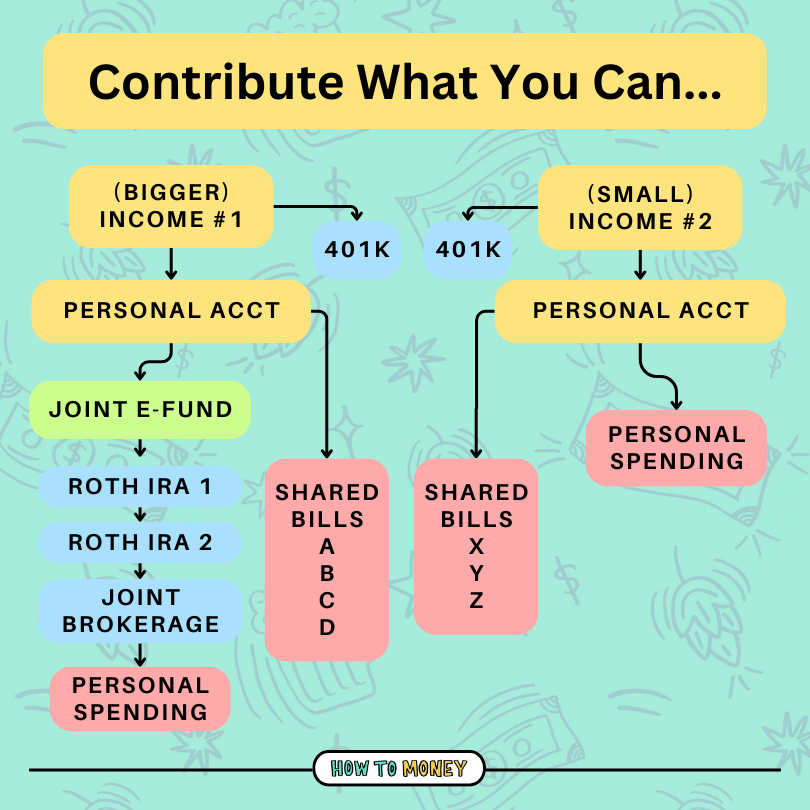

3. The “I pay this, you pay that” System

This approach is completely custom, and usually allows partners to contribute in proportion to their income. Higher income partners can cover more expensive bills, and the person who makes less can cover smaller items. It’s great for couples with drastically different pay ranges, or if both parties have individual strengths in managing a particular area of the family finances.

Much like the aforementioned split system, this approach also involves each partner maintaining their separate accounts and finances… But, when it comes to shared costs, instead of splitting things 50/50, the couple splits *prior agreed upon* bills or expenses.

For example, imagine Sally is an extremely high income earner, working in downtown Seattle. She is married to Tom, who is a middle-school teacher on a very lean income. Sally and Tom aren’t ready to share everything in their financial life, but they do recognize the huge income disparity which allows Sally to afford a more upscale lifestyle than Tom could afford on his own.

So, the couple split bills for different expense items. Sally covers the entire rent, both car payments, and socks away money into joint retirement accounts. Tom covers all grocery bills, cell phone and subscription costs, as well as picking up the tab for home furnishings here and there.

Although it’s not an equal split of costs numbers wise, both Sally and Tom are happy (and financially comfortable) paying for what they can in the relationship.

Here’s a visual of what this system might look like:

This approach to combine finances is way more common than you might think. That’s the beauty of relationships and supporting the ones you love. Each couple gets to decide what’s fair in their relationships, and if communication is strong, it will continue to last.

Pros and cons

Splitting bills proportionally allows higher income earners to splurge and live a more lavish lifestyle, without forcing their partner to afford it too. As long as each partner is working, doing something they love, and contributing what they can, this joint system can work well.

Another benefit of this approach is that each partner splits responsibility for expenses within their wheelhouse. A homemaker can pay and manage house-related bills, while a bigger earner can organize and pay for the couple’s luxuries. This system fosters strong communication and sharing everything you have.

Potential downsides come when spending gets out of control, or if the higher earning partner that contributes more starts to build a superiority complex. Financial bullying is not cool, no matter how much you make or what shared money system you have!

Another downside to managing bills and expenses separately is that spending can start leaking out if it’s not monitored properly. Having a loose budget might not seem like a big deal in high income years, but knowing your overall household expenses is extremely important when it comes closer to retirement. If neither party is overseeing how the other spends, costly mistakes (or missed opportunities) can be made without realizing it!

Relationships Change Over Time

One last note about setting up a bill paying system when you combine finances with a partner…

Things change over time. The system you start with now doesn’t have to be a forever thing. You and your boo might start with splitting bills 50/50, then slowly move to a proportional method as your incomes grow at different rates. Later in life, a complete merge of everything might be the best way to manage money.

All in all, the most important thing is constant communication. Everything falls into place when your money mindset is aligned.

Combining Finances with a Partner FAQ:

There’s no right or wrong way to combine finances with a partner or spouse. Each couple gets to determine their exact system.

But it definitely helps to ask questions and see how other folks are doing things. Here are some of the most frequently asked questions about combining finances with a partner:

Do we need shared bank accounts?

Not necessarily! Joint name accounts might be easier for some day to day tasks (like writing and cashing checks, or receiving some direct deposits), but as long as each partner has reasonable access to all the shared money, then a shared system will work.

That being said, you’ll want to check local laws for what happens if there is a break up. For unmarried folks, this could get sticky if there is a break up! For married folks, it might not make a difference. In any case, do some research on your personal relationship situation and laws for the state/country you live in.

A good middleground strategy can be to name your partner as an authorized user on your accounts (and make sure they are the named beneficiary if you pass away unexpectedly!). This keeps the accounts in your name, but allows them access, some capabilities, and survivorship.

Should unmarried couples combine finances?

This is totally up to you and your partner. Conventional advice says to not share any money or combine finances until you are legally married (or have a domestic partnership/common law marriage). That being said, some couples delay marriage or choose never to get married, and can benefit greatly by combining their finances. At minimum a 50/50 system for shared bills is easy to agree on.

Truth be told, I merged money with my wife about 2 years before we got married. We even bought a rental property together about 3 months before our wedding! Our situation is unique though, as we had total financial transparency from day one of our relationship. Although we weren’t wearing rings yet, we were committed to each other for life – emotionally and financially, really in every way. Aawwww 👩❤️👨 So we saw no problem merging finances while unmarried.

Should I get a prenup before merging finances?

Prenups are put in place to protect assets you already own before marriage. They don’t help when it comes to bringing in new money you earn while married. So it all depends on what individual assets each partner is bringing to the table, and whether they are ok sharing everything they’ve amassed until this point.

If you have significant wealth, own a thriving business, or have kids from a prior relationship, you may want to speak with a professional about getting a prenup. Here’s a few other pros and cons to consider!

Are couples who combine finances happier?

Research says yes. And, those relationships last longer. But remember, there are MANY different ways to combine finances with a partner, including having split accounts and separate personal budgets.

Don’t freak out and think you have to merge every cent you both have on day 1 of your new marriage. Successful partnerships are all about communication, financial or otherwise.

Do most couples combine finances?

Yep! A 2022 study by creditcards.com revealed that 77% of folks combine finances with their partner in some shape or form. A little less than half (43%) have joint accounts, and most (69%) also maintain personal accounts in their own name.

Here’s actually a great Couples and Money Study published in February 2024 by Fidelity. You’ll notice the theme of regular communication, and the benefits it brings to every financial aspect of a partnership.

What is the best budgeting method for couples?

If you’re new to budgeting, we recommend starting with the 50/30/20 budgeting method. That’s spending no more than 50% of your joint income on needs, 30% on wants, and saving 20% for retirement.

Couples can also benefit from using a budgeting app like YNAB, or using a free expense tracking app like Empower.

The Bottom Line:

It can take many years to get on the same page financially with your partner, and finding a way to combine finances in a way that you’re both comfortable with. No matter the budgeting or bill paying system you use, regular communication is the key to successfully managing money as a family.

Keep in mind, as your relationship grows and changes over time, so does the way you might handle money with your partner. Be open to this change, and always look for ways to improve and maximize your joint financial situation.

Best of luck!

More helpful resources: