How long is your financial to-do list? If you’re trying to build wealth and accelerate your investing progress, chances are you’ve got a lot on your plate. I hope this isn’t too annoying, but I’m going to add one more thing: Roll over your old 401k.

Why? Because chances are your old 401k isn’t doing as much for you as it could be. By getting it out of the clutches of an old-school financial institution or insurance company, you can reduce fees and ensure that your retirement dollars are working even more effectively on your behalf.

That’s where Capitalize comes in. Their goal is to turn the formerly arduous task of rolling over your old 401k to an IRA into a breeze.

What Is Capitalize?

Capitalize is an awesome fintech company that helps people roll over their previous employer 401k or 403b accounts into more efficient investment vehicles. They launched in 2019, and are headquartered in New York City.

Currently in the USA, there is an estimated ~30 million “forgotten 401k” accounts, holding approximately $1.46 trillion in wealth. This abandoned money is being eaten up by junk fees, whittling down people’s retirement savings and contributing to the country’s looming retirement crisis.

Capitalize are on a mission to help change this growing problem. By assisting folks in finding old 401k and 403b accounts, and moving those savings to low cost brokerage firms, Capitalize helps people take more control of their money and financial future!

How Does Capitalize Work?

Capitalize helps you:

- Find your old 401k accounts. Whether you worked for a large employer or a small non profit, if you had an old 401k account that’s been forgotten about, Capitalize will help you find it.

- Choose a new investment account. You can move funds over to a traditional IRA or a Roth IRA, and Capitalize will help you identify the right brokerage account that fits your personal needs.

- Manage the rollover process. Rolling over a 401k to an IRA is usually a long, manual process, which can have big consequences if it’s screwed up. Capitalize use proprietary technology and helpful customer service reps to help manage the process for you.

Does Capitalize Work With 403b Rollovers?

Yep! While 401k accounts are the most popular workplace retirement account, folks who have an old 403b can also benefit by having Capitalize roll it over on their behalf.

The reality is that 403b accounts often come with higher fees than their 401k counterparts. So it’s often even more important for a person with one of these accounts to consider making this move.

Where The Heck Is Your Old 401k?

That might be your first question. You might have completely forgotten about a retirement account that you had years ago with a previous employer. You could even have tens of thousands of dollars stashed away that you don’t even remember investing!

It could be time-consuming to track down that account. And where would you even start?

Well, another great thing about the service Capitalize offers is that they’ll do the digging and find it for you. Even if your company went insolvent years ago, even if it no longer exists, Capitalize is like a bloodhound that will help you nab that old account.

Where Should I Roll Over My 401k?

When you initiate a 401k rollover, you’ll be turning it into an IRA. There are some minor differences between these two accounts, but most folks will be served just as well by having their money in this new IRA, particularly if their current retirement account is with a company that charges high fees.

Capitalize works with a number of different investing companies, including some of our all-time favorite low-cost investment firms. You can roll your old 401k over so that you’re now doing business with Vanguard, Fidelity, or Schwab. (Or if you have an existing IRA, they can help consolidate accounts so your money is all pooled together)

All three of these are wonderful options because of how fierce each of them has been about massively reducing fees for consumers.

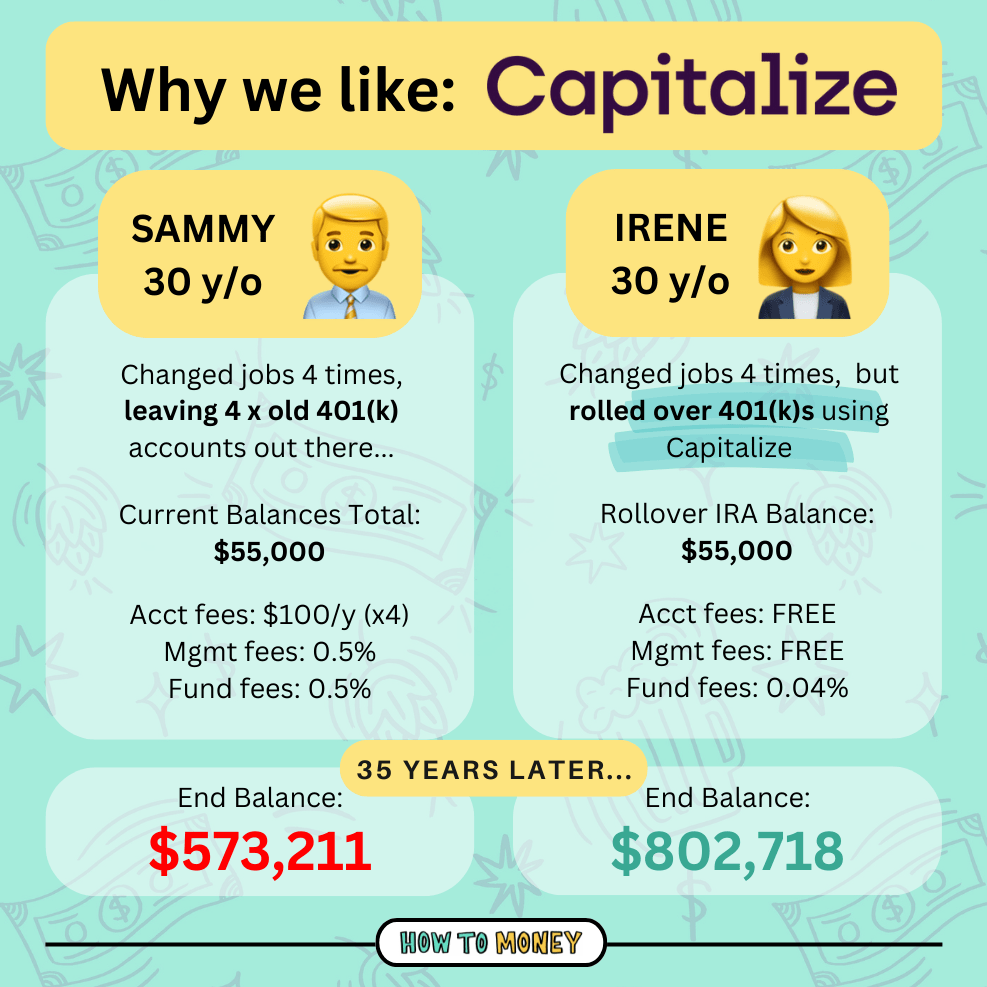

That begs the question, how rotten are fees when it comes to your retirement dollars? They can be pretty gruesome. Check out this example below 👇👇👇

You could also opt for a fairly low-cost robo-advisor like Betterment or Wealthfront.

It’s not just that Capitalize makes it easy to initiate the rollover, they’re keen on making sure that your money is being placed with a reputable low-cost IRA provider.

Capitalize Pros and Cons

| PROS | CONS |

|---|---|

| It’s a FREE service! | Only rolls over to IRAs (no 401k –> new 401k roll over) |

| Simple and easy interface with step by step guidance | Limited phone support |

| Works with 403b accounts too | |

| Broker agnostic and unbiased IRA recommendations |

All in all, Capitalize has more upsides than downsides. Their system truly hand holds you every step of the way to roll over your 401k to a new IRA. Unless you’re in terrible need of customized advice and want to speak with a representative, you’ll find their automated system and chatbot support more than helpful!

How Does Capitalize Make Money?

You might be asking, “so what’s the catch?” I’ve been told that there’s never a free lunch. And you’re right. That mailer you got for a ‘free’ steak dinner is going to come with a masterful sales pitch attempting to get you to buy a financial product or hire a financial advisor that likely isn’t in your best interest.

Capitalize makes money because the IRA providers they do business with pay them each time they land them a new customer. Here’s how they put it on their website, “if you choose to open up an IRA with one of the providers on our platform then we may be compensated.”

But the beautiful thing is that there are no losers in this arrangement. Capitalize gets paid by the investment company for landing them a new customer. Customer acquisition isn’t cheap!

Capitalize is essentially playing the role of matchmaker. They’re holding your hand, helping you ditch an inferior company so that your money is working more effectively on your behalf.

They’ll even help you move your 401k to companies that don’t pay them a dime, which is cool. Here’s the language on their site: “no matter where you decide to move your old 401k, we’ll help you do it – for free.”

And, as we noted previously, the vast majority of the companies that Capitalize partners with are ones we’ve recommended for years because of how much they prioritize offering low-cost funds to their customers.

How Does Rolling Over a 401k Work?

You don’t necessarily need Capitalize. You could choose to perform this rollover on your own. It’s not terribly complicated. Although there are severe penalties if you don’t do it correctly.

You have two options if you choose to go the DIY route.

First, you can opt for an indirect rollover, where you have a check made out to you from your 401k provider, and then send that check over to the new provider that you want to open your IRA with. That’s a scary proposition because the clock starts ticking once you receive the check. You’ve gotta deposit it at your new institution within 60 days. If you fail to do so, that maneuver now counts as a 401k withdrawal and you’re subject to tax and penalties. The stakes are too high to go this route.

A superior DIY option would be to initiate a direct rollover. This takes most of the human error elements out of the equation You’ll need to contact your investment plan’s current administrator as well as the new IRA custodian you’re looking to now do business with.

While this process comes with fewer pitfalls, it can still be time-consuming. Still, it’s nice to know that you can make this happen on your own if you choose.

Capitalize Review: My Personal Experience

There are folks all over the internet giving you recommendations for something or other. It’s hard to know who to trust. When I first heard about Capitalize I was floored. It seemed great. But I had some reservations. So I opted to give it a go myself before writing about the benefits.

My wife had an old 401k with about $18,000 in it. It was still sitting with a company she left quite a few years ago. We knew that we should roll it over. But we just never got around to it. Even financial nerds like me have bouts of apathy that prevent us from taking appropriate action!

This was the perfect opportunity for us to try Capitalize in order to see if the results matched the pitch.

First, we initiated the rollover on the website. With just a few clicks we began the process. But, although Capitalize has an extensive database of 401k providers they work with, they didn’t have my wife’s 401k manager listed in their system. That’s understandable because it was being managed by a really small company.

Typically, they can perform the rollover without needing anything else from you. That initial prompt is all you’ll need to do. Very chill. However, we had to hop on a brief Zoom call with a Capitalize rep who helped us initiate the rollover ourselves.

This won’t be the experience for most folks, but it was great to see that Capitalize has an excellent strategy for helping customers who encounter an issue during the process. Customer service was top notch and it felt great to have an expert walk us through the necessary steps.

On that phone call, we opted to send those 401k dollars to an IRA that my wife has with Fidelity. The whole process took very little time, and I’d say that even with the tiny wrench that impacted our situation, the process was seamless.

Does Capitalize do Roth Conversions?

The short answer is: they will take you half of the way.

Converting an old 401(k) to a Roth IRA is typically a 2 step process. First you move money from the old 401(k) to a traditional IRA (Capitalize helps with this bit), then you work with your IRA provider to perform a “conversion”.

Be really careful here. Converting IRA funds from traditional to Roth is considered a taxable event by the IRS. You’ll need cash on hand to pay the tax bill (you can’t just withdraw funds from the IRA to cover taxes) so make sure it’s planned carefully! Here’s a handful of things to consider when doing Roth conversions.

Is Capitalize Legit?

Absolutely. They have hundreds of 5 star reviews on TrustPilot, with an average rating of 4.9! Like I mentioned with my wife’s personal experience, we loved the speedy service and expertise of the Capitalize team. (And that’s why we’re writing such a positive Capitalize review!)

(Reviews from the capitalize website)

It’s important to note that while you are sharing financial information with Capitalize, they don’t actually take ownership of your money at any point in the process. They do not host financial accounts, they are not a bank, and they don’t control your money. Capitalize only manage the process, so they have no need for FDIC insurance or any of the regulations that most financial institutions are held to.

Alternatives to Capitalize

Although we recommend Capitalize the most and truly believe they are the best, you do have options if you want other ways to manage your 401k rollover to an IRA.

Beagle is the closest competitor to Capitalize. They’re a relatively new fintech company that specializes solely in 401k –> IRA rollovers. But, Beagle isn’t free — they cost $3.99 a month to manage your account. They do offer some additional management services, such as helping with 401k loans.

Titan is another company that offers a “rollover concierge” for folks that need hand holding rolling over their old 401k plans. But this offering is just a small part of their much larger list of wealth management services that probably aren’t applicable to most people.

As we mentioned previously, going the DIY route for rollovers is always an option. If you’re financially savvy, work with large brokers and have the time to manage the process, it’s not too hard to complete by yourself!

The Bottom Line:

Most of us don’t change the oil in our cars. We hire a specialist. That comes at a cost. The cool thing is that hiring the specialists at Capitalize to roll over your old 401k won’t cost you a dime. In fact, over the years, it could save you a bundle. And you don’t have to be an expert investor.

There aren’t many companies offering a 401k rollover service like this – and certainly not for free! Don’t just take my word for it. Capitalize gets impressive customer experience reviews and has a great reputation in the personal finance community.

Hopefully, the item that I added to your to-do list at the beginning of this Capitalize review is actually far less daunting than it originally seemed.

Rolling over an old 401k might not even have been on your radar! Hopefully, it is now. And It can’t hurt to head over to the Capitalize website in order to let them to crush this task for you.

Next steps: