Saving an emergency fund is an important milestone in personal finance. Having that cash buffer on hand is super important to protect yourself if/when things go sideways unexpectedly.

Here’s the best bit. Once you’ve saved up that full e-fund, you’re pretty much done playing simple defense. It’s time to switch to offense mode, where you can roll up your sleeves and start making your money work for you.

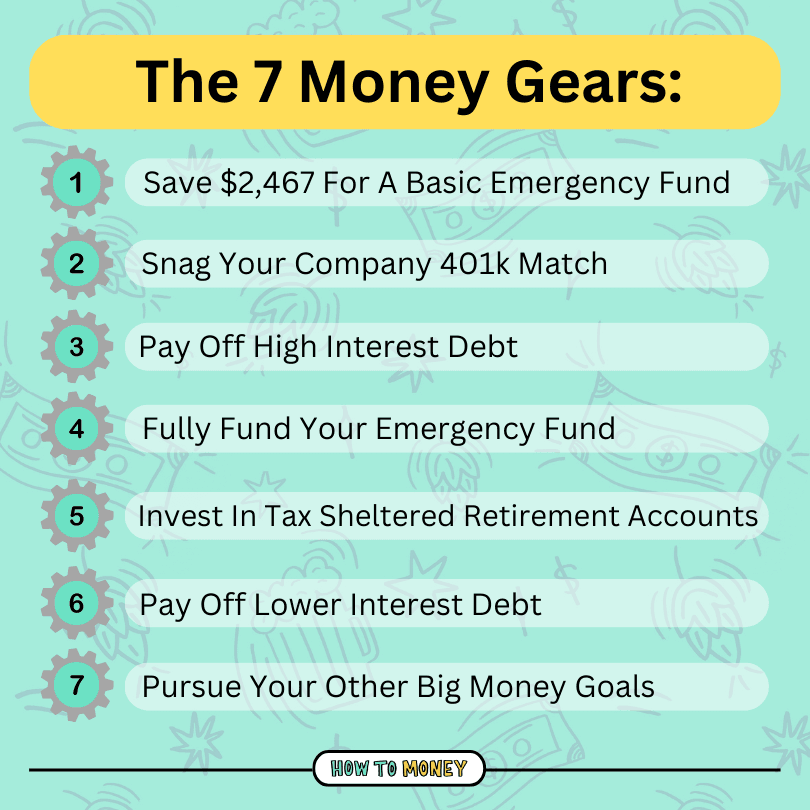

The 7 Money Gears

There’s no single “right” way to do personal finance. Everyone’s journey is different.

That being said, most people will benefit from completing money tasks in a specific order. It’s usually a more efficient route, helping you build wealth faster, or get out of debt more quickly.

We created the 7 Money Gears for this very reason. It’s a quick guide for what to do next with your money.

Whether you’ve just got a basic emergency fund of a few thousand dollars, or a full 3-6 months of living expenses saved, here are some things to consider as your next financial steps…

1. Double check your emergency fund is saved in the right place

The first step towards making your savings work for you is storing it in places that earn the most interest.

And I’m sorry to tell you this, but the “big bank” you’re likely working with right now is paying you next to nothing.

Here’s the sad truth. Big traditional banks (think BOA, Chase, Wells Fargo) take advantage of their clients. They loan your savings out, making money off of your cash, and pay you pennies worth of interest every year in return. That’s great for them, but awful for you!

Even worse, they typically charge sneaky junk fees, or make you jump through hoops to avoid them and keep your account open.

But you don’t need to put up with this!

Online banks have pretty much taken over (in a good way). They are growing like crazy. Since banking is mostly mobile these days (seriously, when was the last time you visited an in-person branch?), online banks can operate without a physical footprint.

New fintech banks like CIT, Ally and Discover are huge online players. Since they run a leaner business model, they will pay you loads more in interest to keep your savings with them.

Better yet, most don’t charge any of those garbage fees to bank with them. They are the best place to keep your emergency fund and protect your cash against inflation.

2. Get your 401k Match

If you have access to a workplace 401k plan, and it offers a savings match, take advantage of it ASAP. It’s like free money. Seriously.

401k matches are supposed to incentivize employees to save and invest for retirement. When you put money into your 401k, your company will also put some in, “matching” your efforts.

Many employers offer dollar-for-dollar matching, up to a certain percent of your paycheck. For example, a 4% employer match means if you put 4% of your paycheck into your 401k, they will put in an additional 4%.

It effectively doubles those savings, helping your account grow at an accelerated pace.

If you can’t afford to save huge amounts in your 401k, that’s OK. But save at least enough to get the full match you are offered. It’s a no brainer.

3. Pay off high interest rate debt

If you still have some high interest rate debt kicking around, pay it off ASAP.

I like to think of high interest rate debt like the man-eating plant from Little Shop of Horrors- Audrey II if you will. While this little plant seems cute at the beginning, each time Seymour feeds it (i.e.., each time you make a minimum payment), the plant continues to grow rapidly and demands more of that tasty human blood (your money).

At the end of the day, if you want that high interest debt out of your life, you have to make like Seymour and blast it out of your life!

Far-reaching analogy aside, debt with high interest rates compounds exponentially, thanks to compound interest. Making minimum payments alone won’t do the trick. You need to viciously attack debt and prioritize paying it fully off.

So, if you haven’t eradicated “bad debt” from your life yet, do that next. Taking some money from your fully funded emergency fund to cut it down could be a smart move.

Related- How to Get Out of Debt

4. Invest in Tax Advantaged Accounts

So you’ve saved up 3-6 months worth of expenses in an emergency fund, snagged your company match, and paid off all of your high interest rate debt…

Here comes the fun part. It’s all about growing your wealth for the future!

Saving vs. Investing

Investing is a crucial step in growing wealth. It means putting your money to work for you, earning dollars of its own.

Simple savings (like in a checking account) doesn’t help you much. You need to ramp up your investing efforts. Here’s an example of the difference between saving and investing…

If you wanted to save up $1 million in cash over 30 years, you would need to put away about $2,777 every month. $2,777 x 12 months x 30 years makes $1M.

Now I don’t know about you, but I do NOT have that kind of margin in my monthly budget. Most folks I know don’t either.

But, if you invested your money in stock market index funds, you’d only need to save about $710 each month. This is because your money would grow at an annual rate of roughly 8%, compounding significantly over the years.

Which accounts should you invest in?

The best place to start investing is in tax-advantaged retirement accounts, like your IRA and 401k.

Why? Because these accounts have special treatment from the IRS which helps lower your tax burden. Paying less in tax means your accounts will grow faster.

With a Traditional IRA or a 401k, you reap a tax benefit now. You can put pre-tax money into these accounts, essentially lowering your taxable income for the current year.

Then, when you pull money out of these accounts in retirement, you’ll pay taxes on it.

In contrast, a Roth IRA allows you to pay taxes on your money now, and pay no taxes on it when you withdraw it in retirement.

Take some time to learn about investing for beginners and which accounts best suit you.

Each tax advantaged account has an annual contribution limit. If you can, try to reach these limits and “max out” those accounts!

5. Pay off lower interest debt

Hopefully all the high interest debt (think: anything above 6-7%) is out of your life by now.

Low interest rate debt is next on the list. Even though this may be considered “good debt”, it’s still important to chip away at these loans and get them out of your life.

This can be stuff like student loans, lower interest car loans or even your mortgage!

At this stage, you’re already putting a good chunk of your paycheck into investments. So your retirement goals should fully be on track. By all means, you could continue to invest and leave lower interest rate debt in place.

But, becoming debt free can be emotionally freeing. It’s the sign of a truly stable balance sheet – owing nothing and having maximum cash flow!

Paying down loan principal

If you want to pay off your student loans, mortgage, or other low interest debt more quickly, here are a few simple ways to pay them off!

- Make an extra payment- Instead of paying your loan once a month, divide your payment by two and make a payment every 2 weeks. By the end of the year, you’ll have made one full extra payment, cutting down your repayment period by years!

- Use “found” money- Anytime you get surprise money, throw it towards the loan. Tax refunds, birthday money, old bonds, or uncashed checks are great for giving that repayment a quick boost.

- Negotiate your bills- One of the best ways to find room in your budget to pay extra money towards your loans is to negotiate your bills. You’re probably paying more than you need to be for insurance, your phone, internet and cable! Call up those companies and tack on the money you were spending here to your regular debt payment.

- Start a side hustle- Starting a side hustle is a great way to explore your interests outside of work, and make more money for your ambitious debt payoff goals.

Related- Ways to Pay Off Your Mortgage Early

6. Move on to the fun stuff

Once you’ve saved 3-6 months worth of expenses in an e-fund, paid off all of your debt, and are saving and investing 15-20% of your income in tax advantaged accounts, it’s time to move on to the fun stuff.

Now, you have the freedom to focus on what you want to do with your money, instead of what you should do. Here are a few things you can focus on later in your financial journey!

Pad your emergency fund even more

If you are the sort of person who loves to be prepared for anything, you can take this opportunity to save even more money in your e-fund.

You can extend your emergency fund to a full year’s worth of expenses, giving you even more financial freedom and peace of mind.

Start saving for your kid’s college

Although it is not a necessity, many parents dream about being able to give their children a financial leg up. Saving for their college is one of the most common ways people do this.

While you should prioritize saving for your own retirement first, when you reach this step (aka money gear #7), you can absolutely start saving up for your kid’s education.

The best place to save for your kid’s future education will likely be inside of a 529 plan. This investment account is tax-advantaged, and if your child decides not to pursue higher education, the funds can be rolled into a Roth IRA for them.

Consider pursuing early retirement

The FIRE community, or “financial independence, retire early” community are all after one thing. Quitting their jobs before traditional retirement age and spending their time doing things that are more meaningful to them.

In order to retire early, you’ll need to save and invest a considerable amount of your income each and every month.

However, once you’re at this stage of the game, without debt commitments taking up your precious money every month, you’re in a good position to really amp up your investing!

Pursuing early retirement isn’t be for everyone. There are pros and cons to the FIRE movement.

So make sure to really take the time to consider whether or not this is something you really want to pursue. We’ve covered it extensively in other posts, so giving these a quick read through should give you a good overview!

Travel more

You’ve worked hard and saved a lot. Maybe it’s time to take your foot off the gas and explore other areas of life more?

Travel can be one of the most rewarding things to spend your money on. Not only are vacations good for our mental and physical health, they also bring us closer to our loved ones and help to open up our minds to new cultures and ideas!

BTW – if you love traveling, you can stretch your budget even further by using travel rewards credit cards.

Often, when you open a new credit card, the issuer will offer you a welcome offer of miles or points for meeting a minimum spend within a certain time frame. Those points and miles can be redeemed for real travel rewards, like flights, hotel rooms and even rental cars!

Budget Travel Resources:

- Using Credit Card Rewards for Cheap (or Free!) Travel

- How to Save for A Vacation (+10 Ideas to Help You Save More)

- Best Hotel Credit Cards for Frequent Travelers in 2024

Give Some Money Away

If you have a favorite cause or charity, you can donate more generously now that you have excess savings.

We believe that everyone should be generous with their time and money. There are so many personal benefits you derive, and your community benefits too. It truly makes your life “richer”.

Just make sure to thoroughly vet any charities before giving them your money! You’ll want your donations to make the biggest possible impact for the causes you care about the most.

The Bottom Line:

Saving up an emergency fund is an important first step in personal finance. But once that’s done, you’re ready to delve into the world of investing and making your money work for you.

Start with the low hanging fruit of tax-advantaged accounts like your 401k and Roth IRA. These accounts are designed to help your money grow faster, by deferring or lessening your tax burden.

Once your finances are in full swing and you’re socking away a large portion of your paycheck, you have a lot more flexibility in deciding where to spend or invest your savings.

If you ever get lost or need direction, refer back to the 7 money gears for guidance.

Related Posts:

thanks for info.