You may have heard people boast about the awesomeness of a Roth IRA. We certainly love them and sing their praises all the time on our podcast. So what exactly is a Roth IRA, and how is it different or better than a Traditional IRA?

We know that investing options can be confusing – mainly because there are so many to choose from. In this post we are going to break down why we’re such huge fans of the Roth IRA and why you should be investing in a Roth assuming you qualify.

What is a Roth IRA?

A Roth IRA is an individual retirement account (IRA) that offers tax-free growth and tax-free distributions when you reach retirement age. You start by contributing money that has already been taxed, and then you can sit back and relax, knowing that your money can grow and multiply as much as it wants, without you accruing a big tax bill later.

It’s important to note that a Roth IRA serves as a vehicle, not an actual investment. Once you’ve opened an account and added money to it, you can then purchase investments such as stocks, bonds, and mutual/index funds, etc.

There are two features that make the Roth IRA unique. The first is that your contributions and earnings grow tax free, for as long as you live. You can withdraw any of the money beyond the age of 59 ½ (if the account has been open for at least five years) without penalty or tax.

The other is that your initial contributions can be withdrawn at any time, for any reason, without penalty or tax. You only have to pay taxes and penalties on earnings and growth if you withdraw early.

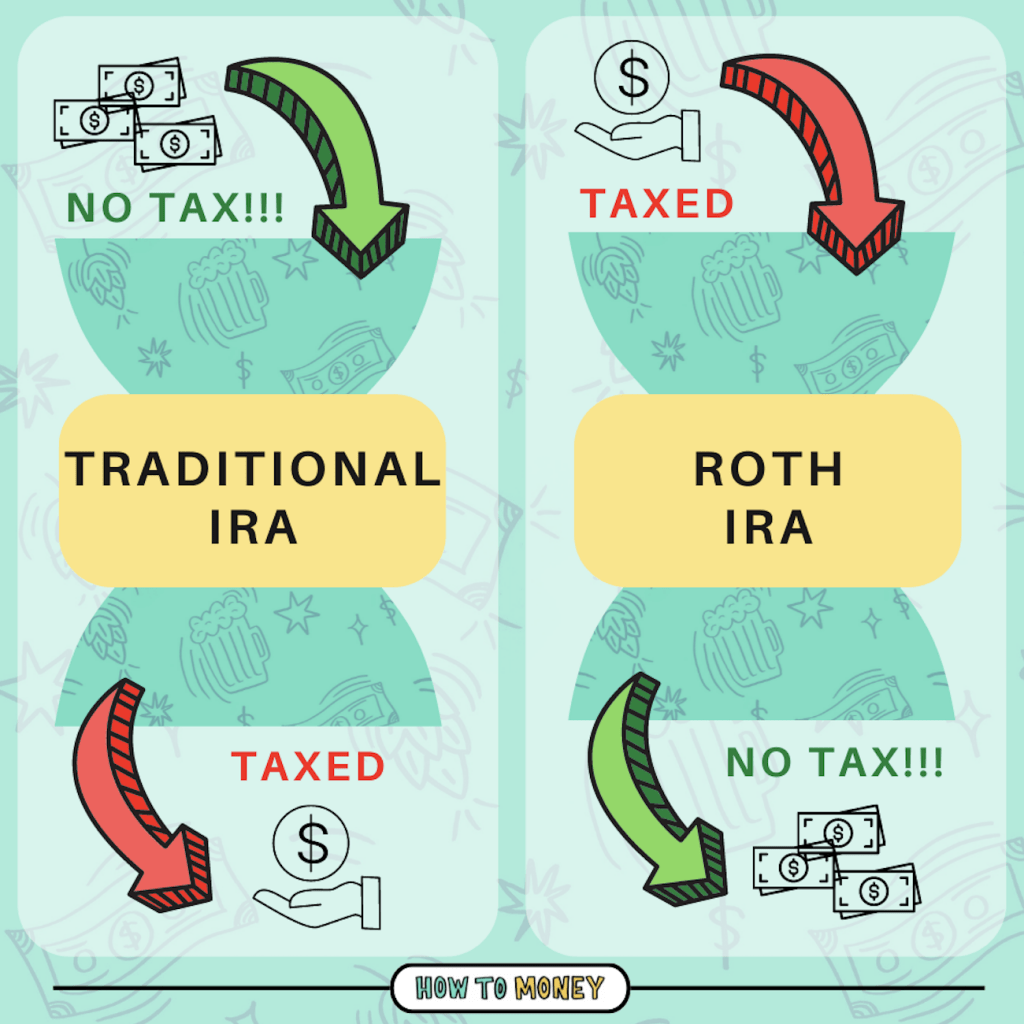

Roth vs. Traditional IRA

Each IRA has different rules and benefits resulting in various pros and cons depending on your individual situation. Roth IRAs are similar to Traditional IRAs, with the main difference being how the two are taxed. Roth IRAs are fueled with after-tax dollars – meaning the money you put in is not tax deductible. However, those Roth funds are tax free upon withdrawal.

No one can predict the future regarding America’s ever-changing tax codes. However, the current tax structure has provided a more beneficial opportunity for many low/middle-income people to take advantage of a Roth IRA today. Remember, you build wealth faster by paying taxes at the lowest rate possible.

For a complete breakdown on the two IRA options and to discover what might work best for you, check out our post – Traditional vs. Roth IRA: Which Is Better?

Who qualifies for a Roth IRA?

If you want to jump on the Roth bandwagon, you’ll need to qualify to be able to contribute. The first requirement to open an account is having earned income. Married couples who file taxes jointly can do spousal Roth IRAs for a non-working spouse. That can help you contribute more than you’d otherwise be able to!

You can open a Roth with as little as $1. There is no minumum dollar requirement. There’s also no age requirement! However, you may or may not be able to contribute to a Roth IRA depending on your income level. Your income must be below a certain level for you to be eligible to contribute to a Roth. Also, Roth IRA contribution amounts can be limited or phased out. If your modified adjusted gross income (MAGI) surpasses a specific number, the amount you can invest is decreased, and at higher income levels, it is completely removed. These limits depend on your tax filing status (i.e., single or married) and how much income you earn.

The IRS established its income limits for 2023. Single-tax filers with a MAGI of less than $153,000 (phaseout begins at $138,000) and married couples filing jointly with MAGIs of less than $228,000 (phaseout begins at $218,000) are eligible to make Roth IRA contributions.

Check out the IRA website for more income limit info: IRA income and contribution limits

Why Roth IRAs are Awesome

- Flexible options (open anywhere, invest in anything) – With a Roth IRA, you have more specific-fund options than you likely have through your workplace retirement account. And you get to choose the company that you do business with.

- Access anytime (backup emergency fund) – Your Roth IRA can function as a glorified emergency fund after a few years. You can pull out contributions tax and penalty free at any time. For those of us who lack discipline, that can be a bad thing. But it’s great if you are making an investment or major purchase that won’t derail your retirement plans.

- No RMDs – A required minimum distribution (RMD) is the amount of money that MUST be withdrawn from a variety of retirement plans each year, generally starting at age 72. However, Roth IRAs don’t require you to take RMDs like Traditional IRAs do. So, if you’re still working some, enough to cover living expenses, you don’t have to take money out.

- More post retirement money – With a Traditional IRA, you get to enjoy the tax benefit now, and chances are, most folks aren’t likely to invest that savings/benefit because it’s just seen as a bonus. With a Roth, tax benefits occur during retirement once you’ve stopped working – also when you’re wiser and less likely to spend that money on consumption.

- Backdoor access – For folks who earn over the Roth contribution limits, there is a conversion option known as a “backdoor Roth IRA.” This will allow individuals with high incomes to fund a Roth despite the IRS’s income restrictions. This is an advanced tactic, so you might want to consult a tax professional before looking into this option.

Best Places to Open a Roth IRA

If you’re ready to open a Roth IRA and start investing, we recommend seeking out a low-cost investment house. (If you’re completely new to investing, start with our beginners guide on how to invest). Here are a few great brokerage firms to choose from:

- Fidelity is free to open accounts, free to buy most funds, and they also host a handful of ETFs with no or incredibly low management fees!

- Vanguard: Probably the fastest growing index fund provider in the world. Its founder, John Bogle (RIP 🙏) invented index investing!

- Charles Schwab has been around for decades. They are the 3rd-biggest broker (behind the aforementioned).

- If you prefer using a mobile device, M1 is a great investing app.

Roth IRA FAQ:

Here are a handful of common questions about Roth IRAs:

What are the disadvantages of a Roth IRA?

There are only a couple of potential downsides to Roth IRAs. One big one is that there’s no up-front tax break. You need to wait years for investments to grow and interest to accrue before you realize the huge tax benefit.

Another downside is the contribution limit. Each year you can only contribute so much (the max for 2023 is $6,500, or $7,500 for those older than 50).

What is better, a Roth or Traditional IRA?

Check out our full post on Roth vs. Traditional and which might be better for you. Long story short, if you believe your tax bracket will be higher in the future than it is now, a Roth IRA is probably best.

Can you have both a Roth and Traditional IRA?

You sure can! But, the contribution limit is split across BOTH account types each year. For example, if the limit is $6,500 for this tax year, you can contribute $2,000 to a Roth and $4,500 to a traditional IRA. You cannot put $6,500 into each account.

Can you lose money in a Roth IRA?

Yep, a Roth IRA is just like any other investment account. It grows or shrinks based on what you invest the money in. Remember, a Roth IRA is just the account type, not the actual investment.

PS. We recommend low-cost index funds, invested for the long haul. That’s how we invest our money!

The Bottom Line

If you’re a young adult having difficulty even grasping the concept of retirement (because it’s so far off), opening a Roth IRA could prove to be a wise choice. The longer your money sits in a tax-free growth account, the more you benefit. Simply investing $500 a month could easily grow to over $1.5 million (tax-free!) over 40 years!

Another peace of mind perk of a Roth IRA is the ability to withdraw contributions at any time (as opposed to a Traditional IRA or most other retirement accounts). Let’s say you invest $2,000 this year and desperately need it back in a few years. No worries, you can withdraw that initial $2,000 without penalty (although we hope you don’t ever need to!). It’s just nice to know there’s access if a major emergency pops up.

Lastly, if you choose to pass on your Roth at death, your beneficiary gets to continue those tax-free withdrawals.

The Roth IRA is a beautiful investment account that can help you build wealth in a meaningful way (and even become a millionaire) over the years!

Related posts:

For Roth IRA, are contributions subject to penalties and tax if I withdraw just the contributions before 5 years of opening the account?

Nope! Contributions may be withdrawn from a Roth at any point.

Thank you!

Hi Matt,

I have been listening to your show for quite some time now and it has helped me organize my personal finance A LOT! I have a question about traditional IRA. I have an inherited traditional IRA and am wondering if I should convert it to Roth IRA, as I anticipate that my tax bracket will go up pre-retirement. My question is when and how. Should I convert now or right before the bracket goes up? Should I convert all at once or in small chunks over time? Thanks!

The tldr is yes, do a Roth conversion now! But if you’d like to hear a more thorough answer, we’d love for you to submit a listener question: https://www.howtomoney.com/contact/

Hey Guys. I created a Roth IRA Brokerage account with Vanguard and put a lump sum of about 3k into it, since savings rates are so low right now. I kept the funds in there for about 3 months, but didn’t notice any change in returns or dividends so I thought I hadn’t taken all the necessary steps. In one of the episodes, you guys mentioned that you have your Vanguard funds in a Total Stock-market Index fund. I found this resource in their investment funds section, and thought it seemed to be what you were referring to: (https://investor.vanguard.com/mutual-funds/profile/overview/vtsax). Was I correct in that assumption? I ask because I know the big selling point with ROTH IRAs is that you can take out what you put in when you need it, but whenever I look at withdrawing/selling any amount, it asserts that there will be a fee for anyone under 59.5 yr of age.

And if, as I presume, I did this incorrectly, would it be worth it to take the penalty and move things into the right place?

Thanks for all the great advice over the years, guys!

-long time listener, couple times caller

Hey Corey- congrats on getting some money into your Roth IRA! Just make sure it’s money that you’re planning to leave in there for the long-haul.

For your specific situation, it sounds like you have money in your account, but that it’s just sitting there as cash. And so you’ll want to use those funds, which should automatically be swept into a ‘money market’ fund, to purchase whatever funds you’d like- for instance VTSAX or VOO which is my favorite. You won’t need to take money out of your Roth in order to do that.

But it is also true, that you can withdraw any contributions to your Roth IRA without tax or penalty.