We all want to see our kids flourish financially. But we can’t just give them buckets of money and consider their future problems solved. We need to teach them responsibility and equip them with the right tools and habits to build wealth independently.

One of the things that keeps me up at night is that the majority of U.S schools do NOT teach kids the most basic life-survival skill – money management. So, if you as a parent and the schools are not teaching youngsters about core money concepts, you better believe they are learning those behaviors from other sources.

In this article we are going to share our top eight tips and strategies to give the kids in your life a financial head start up in order to better prepare them for the future.

1. Set the best example

Kids are human sponges. They are watching and listening to everything you do…whether you realize it or not. They soak up your beliefs, habits, and use you as a gauge for what success looks like in life. With that said, it should come as no surprise that the biggest money influence in a kid’s life is their parents.

Before you think about your child’s financial future, you should solidify your own first. This means proper budgeting, saving, retirement planning, and investing, as well as respecting the money that flows into your life. The goal is to set a good example of money management for the next generation to follow.

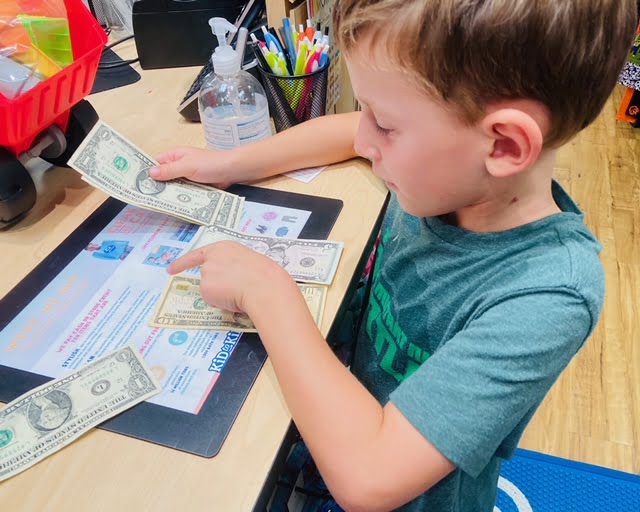

For children to truly grasp a concept they need a tangible experience. Think about it…when was the last time you went to a brick-and-mortar bank and cashed a check or made a cash deposit into your savings account? When it comes to handling money, the technological age we live in has made every transaction digital.

It’s time to turn back the clock to our grandparents age and incorporate some of these ideas to help kids experience money in a meaningful way:

- Use actual cash to show youngsters how money is exchanged in a more tangible way.

- Take your children to a brick and mortar bank to show them how you withdraw and deposit cash.

- Explain the value of a savings account to them.

- Make saving fun with short money challenges

- Give them three jars and label them “Give|Save|Spend” to teach the fundamentals of money management.

2. Talk to them about money often

It’s never too early to start talking about money with kids. Start by discussing with your children how much items cost and how you pay for them. Young people are often faced with the challenge of wanting to buy more than they (or their parents) can afford – or are willing to pay for.

Along the same lines, it’s a good idea to train kids how to become better bargain shoppers and to understand that life is full of choices. Situations like, “You can buy this skateboard for $60, or you can buy these roller skates for $35 and still have $25 left over to buy something else (or hopefully to save).” These circumstances provide children with vital opportunities to weigh decisions and contemplate the potential outcomes.

Speaking of kids wanting to buy things, have you ever caught yourself saying, “We can’t afford it,” when they ask to buy something? What do you think your child’s interpretation of that is when he/she sees you spending money on other things? “We can’t afford it” actually means, “In our family budget, we prioritize what we spend money on. That toy you want is at the bottom of our list of priorities.” Good luck trying to explain that to a kid!

Assuming your kid isn’t in the middle of a meltdown, try to explain simple, core budgeting concepts like. For example… “We make $X a month and have to spend $X of it on living expenses such as housing, groceries, and clothes.” Then grab a pen and a paper and have them write down all the family expenses to understand where all the money is going and how things are prioritized.

The idea is to help them learn how you earn and spend money. Then the next time junior has an impulse to buy a toy you can say, “That’s not in our budget right now, but maybe we can add it to our birthday or Christmas list.”

3. Add them as an authorized user to your credit card

We’re not saying you should actually give them free rein to spend with your credit card (you are responsible for PAYING the balances). But just adding them as an authorized user on your account will give your kids a financial head start. Because taking that action will start reporting your hopefully flawless payment history to the three credit bureaus on your child’s credit report, giving them a leg up when the reach adulthood.

A good credit score can help with apartment rentals, cheaper insurance, job applications, obtaining better rewards credit cards. Also, better loan term! You can give them all these benefits earlier in life – for free – by adding them as users to your credit card account.

The minimum age to be an authorized user is typically 13. But certain card issuers, such as Capital One, Citibank, BOA, and Wells Fargo, do not specify a minimum age.

4. Encourage them to work early

Did you know… Kids who do daily chores (starting as young as age 3-4) grow up to be happier, more successful adults? That’s right, folks! Teaching kids the value of hard work (and getting paid) can boost their confidence, independence, and it’s a great segue into learning about saving/investing.

**Before we go further — this is probably a good time to mention child labor laws. Definitely familiarize yourself with federal/state laws before putting minors to work! Especially if they’ll be using this income to invest in a Roth**

My work story: My mom literally dragged me to Kroger the day I turned 15 so I could begin my illustrious career as a bag boy…uhh…I mean, “courtesy clerk.” I made a whopping $3.85 an hour, plus tips! From then on, I was responsible for paying for things that I wanted in life…like a car!

The benefits of working at an early age are innumerable. In addition to earning money, you learn people/social skills, time management, organization, teamwork, communication, problem solving, decision-making, networking, resourcefulness, and leadership.

Many kids are eager to start earning money. They just need a little encouragement and some handholding to kick things off. And getting money into their hands is one of the best ways to help teach them good financial habits.

5. Help them budget & save

The word budget is not a negative concept – and your kids should grow up knowing that. A budget is simply a tool that will allow you to control where your money goes. In fact, a budget can be a truly freeing device. You can probably guess what happens if you don’t take control of your money?

Kids in today’s advanced tech world are glued to their smartphones. Take advantage of this by assisting them in locating a decent budgeting tool that will get them into the habit of recording all of their income and expenses. Budgeting will help instill children with core financial literacy skills and reduce their financial anxiety. Here are four easy budgeting strategies you can teach them, along with our favorite budgeting apps.

If you’re new to budgeting, it might be easier to start a basic budget. Begin by writing down your income and expenses using pen and paper. Be sure you include savings goals along with allocating a percentage of your money to give away to notable causes that you’re passionate about supporting.

6. Open a custodial Roth IRA

Minors cannot normally open investing accounts in their own names. But you can help them by opening a Roth IRA for children, and acting as the account custodian. The custodian retains control of the child’s Roth IRA, including contributions, investments, and payouts.

There is no age requirement to open a Roth for kids. BUT… The contributions must be made with earned income. Also, contributions are restricted to the annual limit (just like regular Roth IRAs for adults).

Investing on a regular basis is one of the greatest strategies to accumulate wealth over time. Even if it’s only $20 a month. Time is a youngster’s best ally. By starting at an early age, investing in a Roth can substantially boost the odds of future success. Just think – how much wealthier would you be if you started investing when you were a teenager!?

Related: In addition to a Roth IRA, here are other great investing accounts for kids.

7. Buy adequate life insurance

Should something unforeseen happen to you, there are ways to prevent leaving your loved ones in financial ruin. Purchasing a cheap life insurance policy protects your spouse and children from potentially severe financial losses if something were to happen to you. It gives financial security, aids in debt repayment, assists in the payment of living expenses, and helps in the payment of any medical or final expenses.

Should the worst thing happen, this is a legitimate way to make sure your kids have a financial head start.

8. Create a solid will & estate plan

Not having a will in place can wreak havoc in your kids’ lives after you pass. That’s because if you die without a will, you leave vital decisions to a local court and the laws of your state. You will not be able to choose who receives your property and other assets. That’s not ideal, to say the least.

If you don’t have a will yet, there are great sites out there like Trust & Will, that allow you to create or update your last will and testament at any time. FreeWill is simple and 100% free! Others will cost you a bit of money. And if you have a more complicated situation, you’ll likely want to go see a lawyer who specializes in wills, estates, and trusts. Still, don’t skip this step!

Not sure if you should go the DIY route or lawyer up? Be sure to check out our guide to creating a will!

The Bottom Line:

One of the best investments you can make in the next generation is through the power of financial education. Despite most American school systems not offering any form of financial literacy courses, there are plenty of helpful resources available to assist in educating your loved ones so that you can offer those kids a financial head start in life.

Understanding and managing money is a lifetime journey. However, the sooner you can teach solid financial habits to your children, the more likely they will to adopt those habits. They’ll then discover the beauty of financial independence and freedom in the future!

Read more:

Great information Particularly on educating kids on money.

Is there a a newsletter/website, besides your own, that you would recommend for investments?