If you have children in your life and want to give them a financial head start, helping them learn about investing will undoubtedly provide countless benefits. Time is a youngster’s greatest ally. The more years (preferably decades) that you allow investments to grow, the larger your nest egg is likely to become.

Unfortunately, most people aren’t taught about how to invest in those early years. It’s often not until they have access to their first 401k that investing even crosses their radar. At that point, a decade or more of that potential investing timeline has already been lost.

Imagine how much wealthier you might be if you started investing when you got your first job as a teenager instead of waiting to start making retirement account contributions until your 30s!

FUN FACTS:

- Only 39% of children have a savings account

- 53% of Americans haven’t opened ANY financial accounts for their kids

- 6% of children have an investment account where they hold stocks, mutual funds, or ETFs

- 5% of kids say they have cryptocurrencies or other digital assets

Source: 2022 survey by T. Rowe Price

Learning to Save Money

Before you dive into investing with your children, it’s a wise idea to start with basic financial concepts like saving and spending.

One of the most important money habits you can develop is learning how to save money. The first thing we did with our boys was give them each a savings jar (along with a spending and giving jar). We also opened a savings account for each of them at our local bank to deposit any Christmas, Birthday, Easter, or special occasion money they receive from friends or family.

The sooner you teach kids to start saving, the easier it is to teach them the concept of growing their money, which is what investing is all about.

Most folks think about saving for the future, but saving for the present is also important. The habit of saving helps you set aside money for the things you might need or want to do, for emergencies, and for helping others.

One of the main reasons many individuals have challenges saving money is that they don’t have a savings plan. A solid savings plan helps you determine how much to save, how much to spend, and what to spend that money on. You might want to consider encouraging young kids to distribute their savings money into four buckets:

- Current spending – smaller purchases such as inexpensive toys, clothes, food, and entertainment

- Future spending – first car, college, or money for investments

- Big wants – taking a fun trip, a new bike, video games, or leather jacket

- Helping others – charities, churches, or community needs

Related: Saving vs. Investing Differences

Introduction to Investing

Once your child has a grasp on the fundamentals of spending and saving, you can move forward on discussing basic investing concepts.

Asking questions such as “What is a stock?” or “What is a bond?” is a great start. Keep the chats simple and easy for your kid(s) to understand.

Explain that in most cases investing is a waiting game, requiring much patience and planning – two skills that will take time for youngsters to comprehend and develop. Reiterate that investing is a lengthy process that, over the course of time, can deliver impactful results.

“Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.”

Paul Samuelson

Stock Market Overview

Begin with the basics of investing by explaining that a stock — or share of a company — allows them to have ownership in that company. Have a “show and tell” moment and show your child how your investment portfolio has grown over the years through compounding returns (more on this below).

- Stock – a stock is a fractional share of ownership in a company. In this case we are referring to stocks of publicly traded companies. Publicly traded companies are companies that have stocks that are available to the public. Private companies do not have stocks available for everyone to own.

When you invest in stocks you own shares of a company. For example, if you buy one share of the Coca-Cola company you become a shareholder of Coca-Cola and are entitled to the profits they pay out – if they pay them out.

- Stock Market – the stock market is a place where stocks of all publicly traded companies are bought and sold. Thousands of companies are represented in the stock market and can be grouped into categories that collectively represent something. It’s called an index. For example, the S&P 500 index is a group of the 500 largest publicly traded companies in America. Together they are a representation, or indicator, of the U.S. economy. Companies like Alphabet (Google), Apple, Amazon, Walmart, and Disney are also part of this index.

Fun Fact: The average stock market return is about 10% per year for nearly the last century, as measured by the S&P 500 index.

The Power Of Passive Income

One of the exciting aspects of saving money is watching it grow without having to do anything. This is an example of passive income.

Your kids might ask, “How is it possible for money to grow on its own?” Well, this phenomenon is possible because banks pay interest on the money you deposit. These institutions are paying you to keep your money with them so they can turn around and lend it out to other people.

Passive income —> is earning money from a source that doesn’t require effort, like a dividend stock or rental property.

There are two types of interest: simple interest and compound interest. The difference between the two is that simple interest is paid only on the amount deposited, which is commonly referred to as the principal. Compound interest is paid on the principal plus accumulated interest from previous periods.

What is Simple Interest?

Let’s say you deposited $1,000 into your savings account at your bank which offered to pay 4% simple interest per year. That means each year that money was sitting in your back you would earn $40. Here’s how it would look over a five-year period:

| Initial Deposit | $1,000 |

| End of 1st year | $1,040 |

| End of 2nd year | $1,080 |

| End of 3rd year | $1,120 |

| End of 4th year | $1,160 |

| End of 5th year | $1,200 |

In five years you will have earned $200 in passive earnings without having to do anything. This shows you why it’s important to start saving as early as possible. Kids have a more valuable tool for saving than adults – it’s called time!

What is Compound Interest?

Compound interest is making money on top of the money you’ve already earned. A simple way to demonstrate this concept to a child is to ask them, “How much do you think a penny would grow to if you doubled it every day for a month?” They might be shocked to discover that a single penny is now worth over $10 million!

As you can see, one of the biggest benefits of getting kids started with investing is the opportunity to earn compound returns over the long haul.

For example, if a youngster saves and invests $1,000 at age 10, it will be worth nearly $190,000 when they’re 65 or almost $790,000 when they’re 80 (assuming 10% annualized returns). Those astronomical numbers are attention grabbing and should give them something to think about. Even small contributions can lead to significant returns.

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” — Albert Einstein

Teaching Kids about Risk (high risk vs low risk)

There’s a famous saying in the personal finance world: “There’s no such thing as a free lunch.” If someone invites you to a free lunch, they’re trying to sell you something. There’s always a cost.

In the investing realm, the cost is risk – the risk of losing your money. There’s no reward if you take no risk, and the more risk you take, the higher the potential reward. This is what is meant when you hear, “There are no free lunches.” You can’t get something – whether it’s a free lunch or a high reward – for nothing!

It’s important to talk to young kids about the risks involved when they invest their money. Some investments have very low risk but offer returns that are also quite low. Other options, such as stocks, come with higher risks attached, but also have the potential for strong returns. One of the best ways to learn about these differences is by ensuring that they have real money on the line and then letting them see how their investments perform.

Helping them understand the investing process as they incur both gains and losses is invaluable. This will allow your kids to gain a sense for their personal risk tolerance, which can help guide them throughout their investing lives. There’s something massively important about helping your son or daughter actually invest while they are still living under your roof.

There is, of course, a tradeoff between risk and return. To make a considerable amount of money, you must take the chance of incurring sizable losses. However, play it safe, and you will most likely have to settle for modest returns.

Long-Term Thinking

As a young investor, it is vital to realize what level of risk you can tolerate and how that can translate to returns when choosing investments. For example, stocks are considered much riskier than bonds because they are more susceptible to market fluctuations. Just look at how the stock market fared in 2022. It wasn’t pretty!

While the stock market took a nosedive last year, it’s important to zoom out. As I mentioned earlier, long-term investors have seen average returns of 10% over the decades. Savvy investors (which is what you want your kids to be) won’t pay too much attention to short-term results.

Related: How to move out of your parents’ house

Learning about Diversification

You’ve probably heard your parents say – “Don’t put all your eggs in one basket.” In the realm of investing that means you should spread out your risk in case one investment doesn’t work out. That way you still have your money growing even if one investment doesn’t go as planned.

Diversifying can help you:

- Lower overall risk of investments

- Smooth the ride of ups and downs

- Earn more money, in more ways

- Boost investment confidence

The best way to diversify in the stock market is to invest in index funds. An index fund is a pool of money that’s invested across a whole bunch of companies. Index funds make it much easier for people to get exposure to hundreds – or even thousands – of companies without having a ton of money to begin with.

Highly diversified (and low cost) index funds we recommend:

- VTI, VTSAX, FSKAX: These all track the total stock market, meaning you own a tiny piece of every single publicly traded company there is!

- VOO, SPY: These funds track the S&P 500, which are the 500 largest companies across all stock market sectors.

Learning the concept of diversification at a young age will serve your child well. It will help them to avoid pyramid or get-rich-quick schemes. They will know the risk of putting all their money into one investment, which means they’re more likely to make wise decisions with their money for years to come instead of the succumbing to so many of the traps that other investors fall prey to.

Later in life, If your kids start a business, understanding diversification will encourage them to put some of their income aside into a lower-risk investment to offset some of the risks that their business has taken on.

Diversification is the opposite of a get-rich-quick scheme. It is a part of a slow and steady wealth accumulation method that helps mitigate risk and grow wealth. And it’s a necessity for all young folks to understand!

Best Investing Accounts for Children

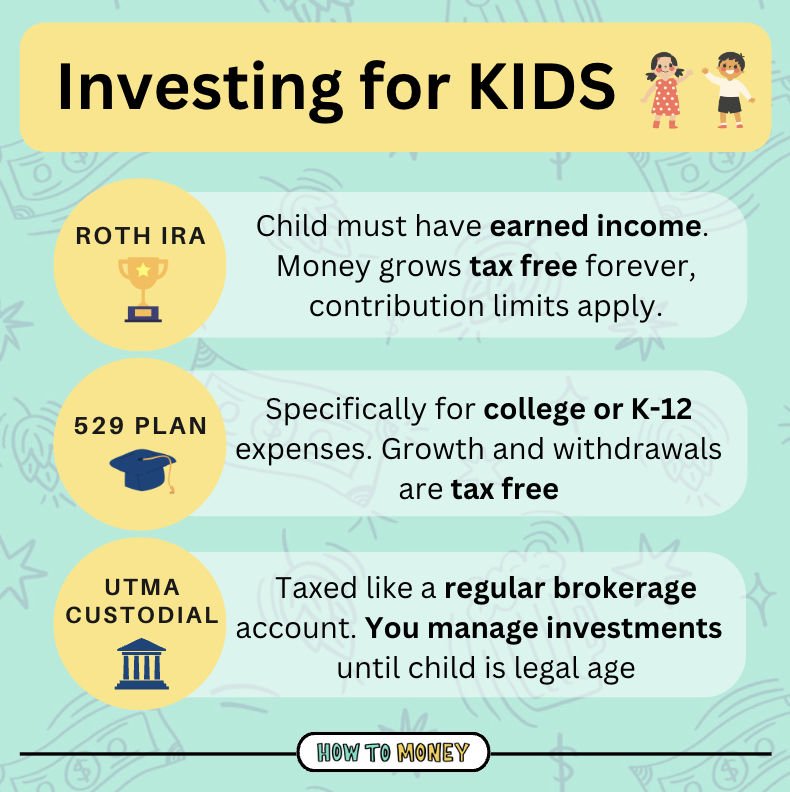

- Custodial Roth IRA – A Roth IRA is one of the best options for saving for retirement, and if your child has a paid part-time job, they may qualify for a custodial Roth IRA. The parent opens the account on behalf of their child and manages the money until that kid turns 18, or 21 in certain states. The account’s value can grow tax-free, while contributions and earnings can be withdrawn penalty-free for qualified educational expenses.

- 529 education savings plan – A 529 plan is like a retirement account, but instead of saving for retirement it allows you to save for a child’s future education. Your money is allowed to grow tax-free, and withdrawals are tax-free as long as they’re used for qualified education expenses.

- Custodial trust account – Also known as a UGMA or UTMA trust account, is opened by an adult for the benefit of a child. The adult is the custodian of the account until the minor reaches a certain age, typically 18-25 years old, depending on the state. The accounts have more flexibility than a 529 plan, but don’t come with the same tax benefits.

- Brokerage account – Some brokers allow minors to open their own brokerage account, giving them ownership of their money and investment decisions. Fidelity’s Youth Account allows kids aged 13-17 to open an account with no fees or minimum balances and start saving and investing. A brokerage account is taxable, so they’ll have to pay taxes on any income they earn. Also, know that the money your child accrues in this account can impact financial aid they may receive for college.

Bottom Line/Final Thoughts

The earlier you can teach kids about investing, the more likely they are to develop better financial habits and build wealth over the course of their lives. Instilling youngsters with investment smarts can also be a great way to encourage shrewd saving and spending habits that will benefit them greatly throughout adulthood.

There are so many different ways that your child can start investing. And I’m not just talking about the aforementioned accounts. However, one way to think about this teaching endeavor is that you are teaching your kids to invest in themselves.

When you teach kids about investing, it’s not just a once off conversation. It should be an ongoing dialogue about your child’s investments, including chats about losses, gains, and mistakes. This constant discussion will push them in the right direction. Everything is a teachable moment.

You might be surprised at how much your kids can understand on the investing front, even in their elementary school years. But by helping them start building knowledge and a nest egg now, they’ll appreciate it (and you) later.

Recommended Books

- Investing for Kids: How to Save, Invest, and Grow Money by Dylin Redling and Allison Tom

- Investing for Teens: How to Save, Invest, and Grow Money by Michelle Hung

- Investing for Kids Activity Book: 65 Activities About Saving, Investing, and Growing Your Money by Justine Nelson

- The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns by John Bogle

- The Motley Fool Investment Guide for Teens: 8 Steps to Having More Money Than Your Parents Ever Dreamed Of by David and Tom Gardner

- How to Turn $100 into $1,000,000: Earn! Save! Invest! by James McKenna, Jeannine Glista

- The Simple Path to Wealth: Your road map to financial independence and a rich, free life by JL Collins

*Feature pic by Kenny Eliason on Unsplash