So your workplace doesn’t offer a 401k plan? No worries! There are plenty of ways to save for retirement without a 401k. In fact, sometimes investing outside an employee-sponsored plan can be a better way to save for retirement. That’s because setting up your own accounts gives you more flexibility to invest where you want, how you want, and ultimately allows more control of your nest egg growth.

Don’t get me wrong – 401ks are great. But they’re not the be-all-end-all account for growing wealth. In this post, we’ll run through some alternative strategies and tools to help save for retirement for those people without access to a 401k.

Better yet – later on I’m going to list, in order, the accounts most people should prioritize first. And, we’ll cover what type of investments (hint: index funds) you should prioritize for long-term diversification and growth.

Psst!… If you work for a small business that doesn’t offer a 401k plan currently, check out Human Interest! Forward this site to your boss/owners – they might be able to launch a 401k retirement plan for you.

Tax-Advantaged Retirement Accounts

The more you can avoid or delay taxes, the more efficient the growth of your nest egg will be. So it makes sense to prioritize investing inside tax-advantaged accounts first.

Here’s an overview of the main tax-advantaged accounts, their tax treatment, and some notes on withdrawals and contribution limits.

| Traditional IRA | Roth IRA | HSA | |

|---|---|---|---|

| Tax Benefit | You pay less taxes now, deferring them and paying in retirement. | You contribute with post-tax dollars, but don’t pay any in retirement! | Triple tax advantage (tax-deductible contributions, tax-free growth, tax-free withdrawals for medical expenses) |

| Withdrawal Rules | Taxed as ordinary income; penalties before age 59½ (with exceptions) | Contributions can be withdrawn anytime. Investment growth withdrawals are penalized before age 59½ | Tax-free for qualified medical expenses; penalties and taxes for non-qualified expenses before age 65 |

| Contribution Limits (2024) | $7,000/year (under 50); $8,000/year (50 and over) | $7,000/year (under 50); $8,000/year (50 and over) | $4,150 for individuals; $8,300 for families |

| Income Limits | No income limits for contributions; deductions phase out after $77,000 | No contributions allowed if income exceeds $161k for individuals or $240k for married filing jointly | No income limits for contributions. But you must have a HDHP! |

| Best For | People who want immediate tax deductions | Individuals expecting higher taxes in retirement (most folks!) | Anyone with a HDHP plan should utilize this account |

Traditional IRA

A Traditional IRA is kind of like the little brother to a 401k plan. They come with a very similar tax structure.

When you put money into a traditional IRA, you don’t pay income tax on that money in the current year. But, when it comes time to withdraw funds in retirement, income tax will be due when you start to pull those dollars out.

The biggest difference between a Traditional IRA and a 401k is the contribution limit. For 2024 you can only contribute $7,000 to an IRA. This may seem small, but it’s still a hefty chunk that will compound over many years of growth. For example, if you maxed out only this account for the next 35 years, you’d be sitting pretty in retirement with a nest egg of about $1.2M!

Roth IRA

A Roth IRA is a cousin of the traditional IRA but its tax advantage is different in nature. You won’t receive a tax benefit when you put money in. BUT, any withdrawals that you make in your retirement years are all tax-free!

Even better, any money you put into a Roth IRA can be withdrawn at any time. So if you plan on retiring early, or need to move money around before age 59½, you can access that cash penalty-free. Only investment growth and gains are subject to penalties if you withdraw funds early.

A Roth IRA also has a $7,000 contribution limit for 2024. But it’s important to note that the annual contribution limit is a total across BOTH traditional and Roth IRAs. People tend to favor either one or the other based on their current and projected income.

More info: How and Where to Open a Roth IRA

Which IRA is better, a traditional IRA or a Roth?

This is a common question, and it really comes down to your income tax rates, both now and in the future. If you’re in a high tax bracket now and anticipate being in a lower tax bracket in the future, a traditional IRA is typically your best bet.

If you’re in a lower tax bracket now and anticipate taxes will be higher in the future, a Roth IRA is often a superior choice. Plus, Roth IRAs have the added benefit of extra flexibility.

For the average American, a Roth IRA should be prioritized over a regular IRA.

Health Savings Account (HSA)

Health savings accounts are often overlooked as retirement accounts because they sound really confusing. We’re led to believe that the HSA is a savings vehicle that isn’t intended for long-term investments. But the truth is, HSAs are one of the best investment vehicles in existence. That’s because they have a triple tax advantage. No other account has the same tax avoidance perks!

First, the money you put into a HSA is tax deductible. Next, withdrawals are tax-free anytime when used for qualified medical expenses. And lastly, your money grows within that account tax-free as well!

Healthcare costs are one of the biggest expenses for retirees. In fact, Fidelity estimates that the average 65-year-old retiree can expect to spend around $157,000 throughout their retirement! 🤯

Investing in a HSA over the years not only saves you on taxes now but also helps you avoid taxes when it comes time to pay medical bills. And, if you happen to reach age 65 and have no medical bills (congrats, by the way!) you can withdraw funds from an HSA for any reason without penalty. You will, however, have to pay income tax, which means your HSA account essentially functions like an IRA after age 65.

One last important note about HSA eligibility… you need to have a high-deductible health plan to be eligible to contribute. So, if you’re interested in opening one up, make sure your current health insurance plan qualifies.

Taxable Investment Accounts

OK, let’s move on to regular savings and investing accounts that you can use to save for retirement if you don’t have a 401k.

While these accounts don’t really have built-in tax advantages, they offer the most flexibility. You don’t have to worry about income limits, IRS rules, or any money being “locked up” until you’re old and gray. You have full control over how and what to invest in, and when to access funds.

Here’s a quick summary of the two main account types, and what they are best used for:

| Taxable Brokerage Account | High Yield Savings Account (HYSA) | |

|---|---|---|

| Tax Treatment | You will either pay long-term or short-term capital gains tax on realized profits or dividends. | You pay taxes on any interest that is paid out each year |

| Withdrawal Rules | No restrictions | No restrictions |

| Contribution Limits | No limits on contributions | No limits on contributions |

| Income Limits | No income limits for contributions | No income limits for contributions |

| Best For | Investing for medium and long-term periods | Short-term savings and emergency cash |

| Risks | Investments will go up and down in value (but in the long run always up) | Money is FDIC insured, typically up to $250k. There is no risk! |

Brokerage Accounts

After you’ve maximized any tax-advantaged accounts available to you, the next step is to invest in a regular brokerage account.

You’ve got many choices for where to open an account, but we recommend Vanguard, Fidelity, or Schwab. These firms have no monthly fees or investing minimums and offer free trades and low-cost index funds. You can pick any broker to open an account with, but the less you pay in fees, the quicker your account will grow.

The sky is the limit with brokerage accounts. Invest as much as you can and let the money grow for as long as you’re able! These are the most flexible investing accounts to save for retirement if you don’t have a 401k.

High Yield Savings Accounts

Technically, a HYSA isn’t an “investment” account, but it’s a crucial part of your overall financial strategy.

HYSAs are regular savings accounts that allow you to earn a higher interest rate on your cash. They are designed to hold your emergency fund, helping you build savings for short and medium-term financial goals. These accounts are risk-free because the money is FDIC-insured.

So let’s say you are saving up for a downpayment on a house. Investing those savings might be too risky because of stock market fluctuation in the short term, So putting that cash into an HYSA will keep the money safe, allow it to earn a little interest, plus give you immediate access when the time comes to buy your house.

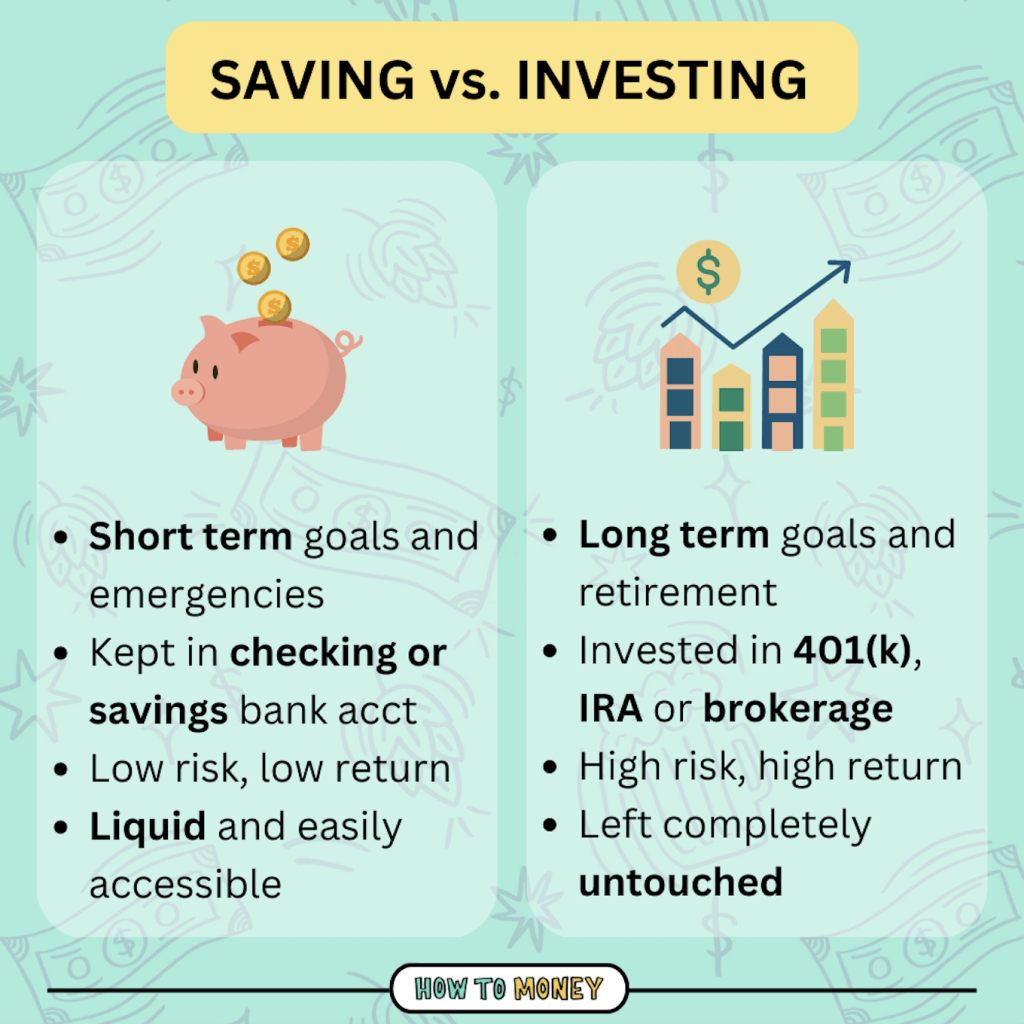

Saving vs. Investing

Most people use the words saving and investing interchangeably. But there’s a big difference. You need to understand the purpose of both. Simply put:

Saving → is protecting your money

Investing → is growing your money

Protecting your cash is important because disasters can strike at any time and you need to have liquid access to a healthy cash reserve at all times. But, saving money alone won’t allow it to grow very fast. If you never made any investments and just saved plain old cash, you’ll never reach your long-term retirement goals.

For example, if you wanted to build up a retirement nest egg of $1M, you would need to save $1,173.04 every single month for 47 years. For most folks, that’s completely out of reach! But, if you invest in highly diversified index funds within a Roth IRA, you could reach your goal in just 34 years by investing $541 each month. That means you’ll reach your goal more quickly and won’t have to come up with nearly as many dollars to achieve your goal.

Investing is important because your money can double, triple, or even 10x in value over the years. But, if you throw all your savings into risky investments and they encounter a few turbulent years, you might find yourself in a tough situation if you need access to that money.

Basically, when you’re saving for retirement, you’ll want to have a mix of savings + investments. Savings accounts are for emergency funds, house down payments, and for any other large expenses you plan to make in the next 5 years or so. For all other money you don’t need until retirement, invest it!

Real Estate Investing

I purchased my first rental property when I was 18 years old and focused solely on investment real estate until my early 30’s. While it helped me build wealth, if I had to do it all again I would prioritize stock market investments within tax-advantaged accounts first. It would have been more financially advantageous due to tax advantages. I’d have had a lot less work to do too!

Just like you can save for retirement without a 401k, you can build wealth without real estate. Don’t fall into the trap of thinking you NEED to buy a rental property (or 6) to retire happily. Sticking to traditional investment accounts and buying index funds is the simplest path to building wealth.

That being said, if you enjoy calculating real estate numbers, have great people skills, and like rolling up your sleeves and getting your hands dirty, real estate might be a good fit for you.

Rental Properties

Owning rental properties can help to diversify your portfolio, provide multiple income streams, and give you more flexibility when the time comes to access money in retirement. Cash flow is extremely appealing to retirees because they can collect monthly income without having to sell any assets.

I’ve written a huge guide on how to buy a rental property, which I suggest you begin with if you’re interested in taking this route. Researching, buying, and managing rental properties carries a lot of risk, and there’s a ton of hard work involved. But, the rewards can be amazing if you do it right.

Every rental property investor starts with zero experience. So if you’re completely new, have no money, and no contacts, that’s OK! It might seem overwhelming and totally out of reach to invest in real estate right now. But if you commit to saving up a downpayment slowly over time, and putting in the time to research thoroughly, you can (and will!) own investment real estate one day.

Home equity fallacy

I hate to burst your bubble. But buying a “home” is not really a great investment. That’s because a primary residence costs so much to maintain and operate. And traditionally, home equity doesn’t grow as quickly as the stock market.

A big mistake many Americans make is thinking that buying a home and paying the mortgage will help them build a retirement nest egg. But the truth is it takes a lot more than a paid-off house to retire. People who don’t focus on building up retirement assets become “house poor”, and often need to keep working past retirement age.

Now, we’re not saying that you should never own a home. You definitely should if you want! Just don’t neglect the other very important retirement accounts at the expense of saving up a down payment. If and when you do buy a home, just make sure you’re still regularly investing in the stock market and building a nest egg outside of your home equity.

Which Accounts Should I Invest In First?

With so many accounts each having different advantages, it’s hard to know where to put your savings first. If you don’t have access to a 401k (and that sweet, sweet employer match), here are the next best accounts to save for retirement:

- HYSA → Emergency Fund: Building up cash reserves is priority number one in personal finance. Emergency funds protect all your assets so you don’t have to disrupt any investments if/when trouble strikes.

- Roth IRA → Max it out every year: Most people will have higher taxes in the future than they have now, so Roth IRAs make the most sense. If your income is past the allowable limit, consider a traditional IRA (and look into Backdoor Roth conversions)

- HSA → Max out if you are eligible: If you have a high deductible health plan, stick money into your HSA. Then, invest in that HSA!

- Brokerage Account → For all excess savings: Once you’ve leveraged tax advantaged accounts, put everything else into a regular brokerage account.

- Real Estate → Optional!: After your main accounts are set up and being funded regularly, real estate investing could be a good next step.

Of course, there’s no one size fits all when people save for retirement, especially without a 401k plan. The above list just outlines the ideal options for most people.

Choosing Investment Funds

Figuring out which accounts to use is just half the battle. The other half is ensuring your money is invested wisely in stocks/bonds that give you the best and safest return over the long haul.

Since retirement is decades away, we almost exclusively encourage people to invest in low cost, highly diversified index funds. Here’s why:

- Huge diversification: Index funds allow you to invest in hundreds, if not thousands, of different company stocks across various industries.

- Passive management: When you buy an index fund you can “set and forget” about your investments. There is no active management for you, and you don’t have to pay a team of people to buy/sell stocks for you.

- Low costs and taxes: Since there’s no active management, fees are MUCH lower. And since the funds don’t trade often, there’s lower tax liability vs. actively managed funds.

- Better performance: Index funds consistently BEAT actively managed funds. Sadly, the “average investor” averages a measly 2.3% return.

Check out our full post on how to buy index funds here. And here’s our cheat sheet of funds we love, and the brokerages that host them!

How Much Do You Need To Retire?

One rule of thumb we like is the 4% rule. To work out how much money you need to retire, multiply your desired annual retirement income by 25. For example, if you want access to $80,000 per year in retirement, you would need to have $2 million saved ($80,000 x 25).

We’ve written about a few other ways to calculate how much you need to retire, as well as other considerations you’ll want to factor into your number.

How much of my paycheck should I invest each month?

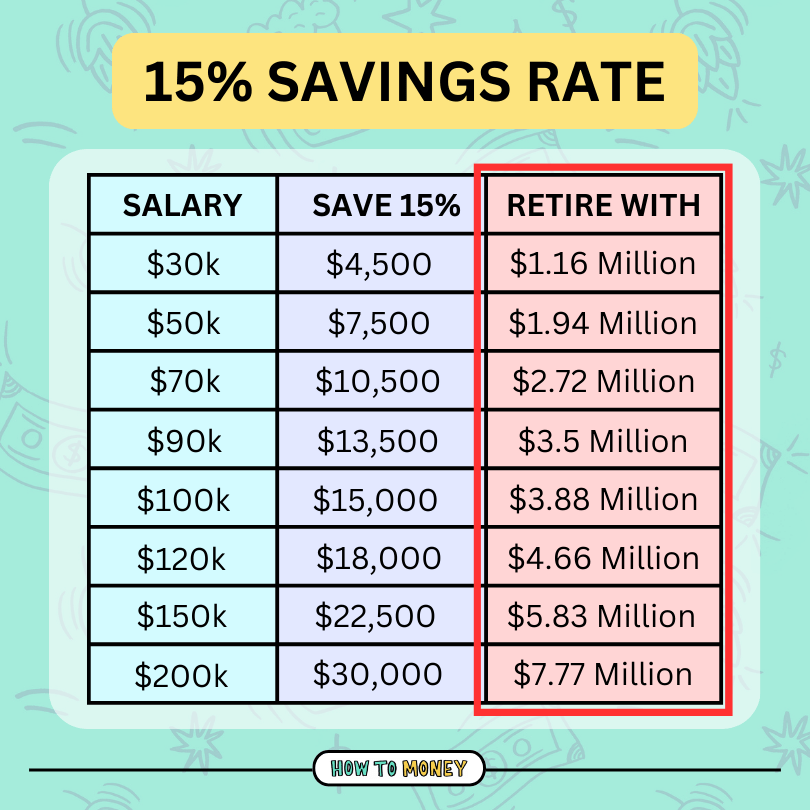

Conventional wisdom says to set aside 10-20% of each paycheck for retirement investing. We agree, and usually lean towards the upper recommendation (20%), especially if folks are getting a late start.

Here’s the cool part. If you consistently invest 15% of your salary every year, no matter what your income is, you’re almost guaranteed to retire a millionaire. Here’s a summary table of annual salary scenarios showing a 15% savings rate. Assuming a 40-year savings horizon and an average 8% investment growth rate, here’s what you could retire with:

Of course, if you’re in your 50’s and have zero dollars saved so far, you’ll need to play catch up and invest much more of your paycheck. Next we’ll talk about ways to save more money for retirement investing.

How to Save More

Whether you’re behind on retirement savings or just want to kick your savings rate into overdrive, here’s a few things that will help you get there…

1. Basic Budgeting and Expense Tracking

If you don’t have a budget right now, it’s time to learn ASAP. Making a budget is making a plan for where your money goes.

For beginners, start with the 50/30/20 budget system. This means spending 50% on needs, 30% on wants, and setting aside 20% for saving and retirement investing. It’s crucial to budget consistently and prioritize your future nest egg. Nobody is going to do it for you!

Good news – modern apps like You Need A Budget (YNAB) automate much of the budgeting process so it’s less work on your end. They track expenses in the background, group your spending into categories, and make sure every dollar you earn has a job. YNAB is $8.25 a month, but the average user saves over $6k in their first year using the software. Try it!!

2. Cutting Unnecessary Costs

The biggest savings will come from your largest spending categories. While cutting out your morning $5 latte will help save some money, bigger efforts like negotiating your rent or biking to work a few times a week can save you HUGE amounts.

So start with your biggest spending categories. Learning to cook and meal prepping is a game changer if you want to save money on food. My friend just tried a 30 day no eating out challenge and saved a whopping $600! No kidding.

It can be hard to make lifestyle changes all of a sudden. So taking things slow and being realistic with budget cuts will likely get you further. Frugal habits take a while to build, but it will be worth it in the end!

3. Increasing Income

There is no limit to the amount of money you can make in a year. You might think there is – but that’s a limiting belief.

Asking for a pay raise is the quickest way to increase your paycheck without totally disrupting your current position. I know it can be nerve-wracking, but your employer isn’t likely to give you more money randomly for no reason. You need to advocate for yourself and ask for it. And if you aren’t getting paid what you are worth, it might be time to look for another higher paying job.

Exploring side gigs, part-time work, or freelancing are always options if you have spare time. All of those additional earnings can be tossed into retirement accounts. For example, you could pick up a bartending job one night per week. If you bring in only $100 per shift, that’s suddenly $5,000 per year you can use to save for retirement. Boom!

We live in an amazing era, where gig work can be picked up on a dime with no experience needed. Just make sure all your extra earnings are saved, not spent!

4. Invest early, invest often

The sooner you learn how to invest, the sooner your money will start “working for you”. This means, in addition to the money you’re socking away from your paycheck, your existing dollars are all multiplying in the background also.

The biggest factor in growing wealth is time. The more years you have to consistently invest money and leave it untouched, the bigger your wealth pile will grow. So if you haven’t started investing yet, get on it ASAP. Even if you have a tiny income, you can still put away small amounts of money. Even small amounts will meaningfully build over time.

The Bottom Line:

You can still save for retirement quite easily without a 401k. By utilizing other tax-advantaged accounts like Roth IRAs and HSAs, as well as regular brokerage accounts, you can build a sizable nest egg over time with fewer restrictions. The key is saving at least 15% of your income, and prioritizing long-term investments like index funds.

Remember, time is your biggest ally for growing wealth. The earlier you begin investing (and the longer you stay consistent over the years), the bigger your nest egg will grow. If you haven’t started saving for retirement, it’s time to learn how and start ASAP. Whether you have access to a 401k or not – you got this! 💪

Related posts: