This question comes from Atlanta local, Graham!…

“On a previous episode, a caller asked if 401k matches should be considered as part of their savings rate. I personally include the match as part of my total income, and therefore do include it as part of my savings rate calculations.

My question is this: should folks consider 529 plan contributions as part of their overall savings rate?

On one hand, the beneficiary of a 529 plan can be changed to any family member, including oneself, at any time. But the purpose of most 529 plans is for the benefit of someone other than themselves.

Similarly, how would you classify the savings that folks do for a large purchase or for gifts for the holiday season? Perhaps a better question is what’ll qualify as saving versus not saving?

Thanks for all that you do!

Matt & Joel’s response:

Hey Graham! We love that you’re tracking your savings rate! It’s one of the most important financial calculations we have to measure our trajectory.

The short answer to your question is: Yes, we think 529 contributions can be included in your savings rate.

Even though that bucket of 529 money might not be used by you one day, it is money that you are socking away personally.

That being said, we really should talk more about savings rates, and how much people should be investing from their paychecks.

If you’re including things like 529 contributions in order to “fluff up” your savings rate number to hit the bare minimum 15% rate, you’re only cheating your future self.

But if you have a really healthy savings rate (think like 20%+) and you want to tack on 529 contributions, we’re all for it!

401k matching

Graham said that a 401k match should be considered as part of your savings rate. Which we’re ok with – as long as it elevates your desire to reach higher savings rate heights!

For example, if you get a 6% match from your employer, and you’re trying to reach an overall savings rate of 15%, it might be tempting to only save 9% yourself. This might not be enough.

That’s because there are other things you’ll want to be saving for. It’s not just about sticking 15% into your retirement accounts and spending the rest of your paycheck. You’ll almost inevitably want to hit other short and medium term savings goals.

So while 15% going into a retirement account is really good, you’ll likely find that you’re keeping debt around longer than you should, or that you don’t have cash on hand for things like buying a car, or putting a down payment on a house.

Long story short, we don’t mind you including 401k matching as part of your savings rate as long as you ensure that your savings rate floor is higher.

Are we being sticklers? Too conservative? Maybe. But the alternative scares us. Not saving enough is clearly worse than saving too much. You want to strike a healthy balance.

529 contributions in your savings rate

OK, back to your main question: Should 529 contributions be considered part of your savings rate?

Yes, we think so! Even if you aren’t saving for yourself, you’re still putting those dollars aside from your paychecks.

529 plans are great. But they’re reserved for folks in money gear 7. You should really only be investing in 529 accounts if you’re already hitting all your other savings goals.

This is one of the reasons why we de-emphasize 529 plans so much on the show. People tend to fund them too early, which hurts their own ability to retire comfortably.

We obviously don’t want our kids to take on loads of student loan debt. But waiting to help kids after you’re already crushing your own finances is a better move.

Yes, 529 plans have gotten better with recent rule changes. But the main goal of saving is for your own financial freedom.

What is “savings” anyway?

Graham asked kind of an existential question about “what qualifies as savings?”.

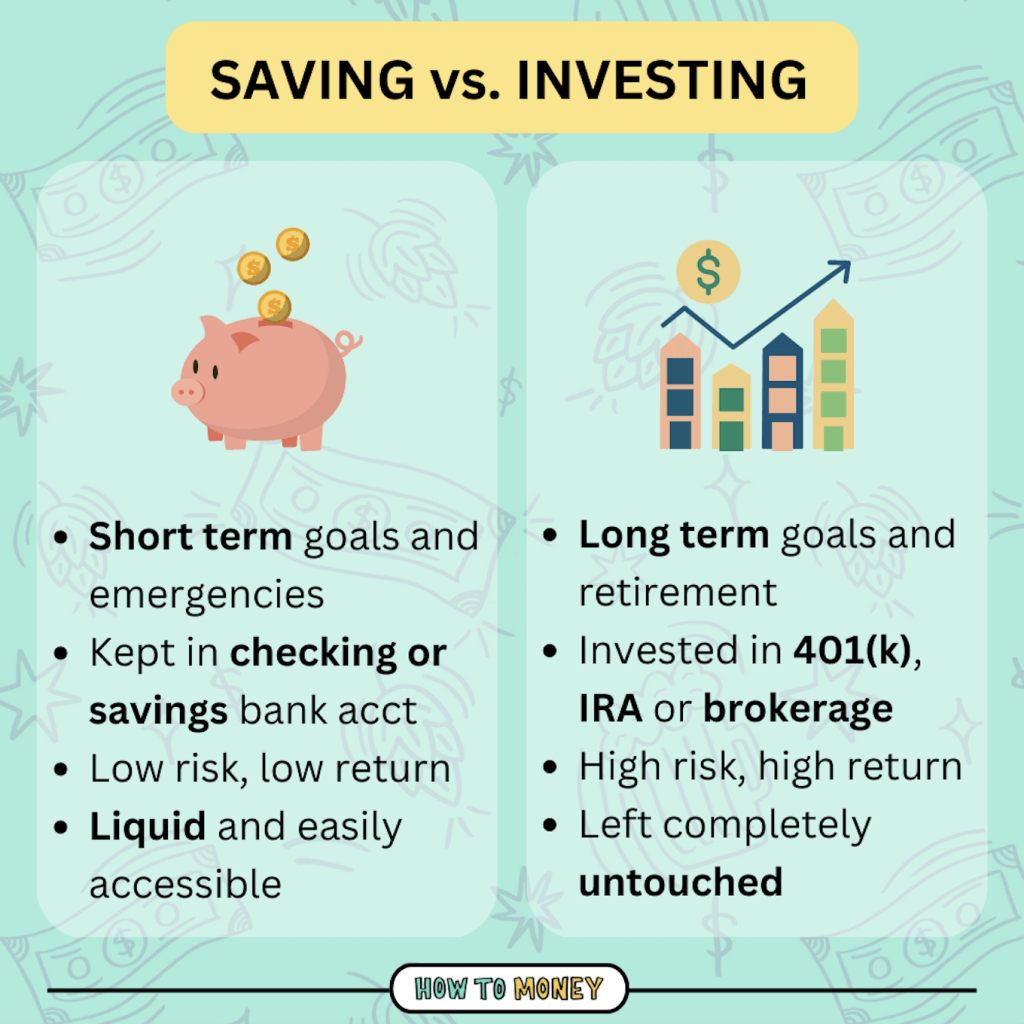

We’ve discussed how saving vs. investing are both forms of delayed spending. (And debt is the opposite, you’re prolonging the pain of a purchase).

But saving is also more than that. It’s a recognition that we have more than we need. And setting aside larger amounts feels like a counter cultural act.

We also emphasize that the goal isn’t to die with millions. It’s to give yourself more options for future freedom (the ability to make less and have more personal autonomy) and to spend more down the road.

There will always be a debate about what should be included in a savings rate and what shouldn’t. But it really comes down to the person calculating. And whether they’re hitting the financial goals they are setting for themselves.

Finding balance

Part of this question comes down to how much money we put in the ‘save bucket’ should go towards short-term goals, and how much should go towards long-term goals?

That’s highly dependent on your financial situation. Clearly it’s important to save for birthday and holiday presents and for vacations. Those are more short-term goals.

But we also need to be saving for those medium-term and long-term goals too. Building sinking funds for buying a house, or paying cash for a car are both really important.

If you put ALL of your savings in your 401k you might be retirement account rich and cash-on-hand poor.

The reverse could be true, too. Too much cash savings means missing out on long term investment gains and growth.

So, ask yourself. How much have you saved for each bucket? Have you achieved a good balance?

You wouldn’t want to forego the employer match, for instance, in order to save for a vacation. But you also won’t want to max out your 401k to the exclusion of saving for that vacation.

We’re all trying to achieve multiple goals at once. And the amount of money flowing into long-term vs short-term savings goals will fluctuate over time.

The Bottom Line:

If you’re already saving a healthy percentage of each paycheck across personal retirement and savings accounts, yes, you can also include 529 plan contributions as part of your savings rate.

But if you’re just trying to artificially inflate your savings rate, you should step back and rethink your overall savings strategy. 529 accounts shouldn’t be an investing priority. Think of them like a bonus account after you’re already crushing your personal savings goals.

At the end of the day, savings rates are just a rule of thumb to help you keep tabs on your trajectory. You shouldn’t live or die based on the exact percentage you’re saving. It fluctuates over time!

The end goal is to make sure you’re saving enough to hit both short-term and long-term savings goals. And this looks different for everyone – so it’s on you to determine this in your own life.

Good luck Graham, thanks for the question!

For the full version of this discussion, check out Podcast Episode #817 (it’s the 3rd question we tackle in the episode)

Related posts: