As you move from job to job, one very important financial task is deciding what to do with your old 401k. Rolling it over into an IRA can be a smart choice. It gives you more investment choices, lower fees, and can pave the way for Roth conversions. But sadly, many people botch the 401k rollover process, and these mistakes can have massive financial consequences.

In this post, we’ll go through the most common blunders when rolling over their 401k to an IRA. Hopefully learning about these screw ups will help you avoid the same fate! Let’s make sure your hard-earned savings are well-protected and continue to grow in the most effective and efficient way possible.

Mistake #1: Not Rolling Your 401k Over at All

The single biggest oversight with old 401k plans is forgetting about them completely. I know what you’re thinking… How can someone forget about all the money they’ve saved!? Well let me tell you, it’s waaay more common than you think.

A report from Capitalize estimates that there are about 29.2 million “forgotten” 401k accounts out there. That’s like 1 in every 5 people that have funds stuck in old 401ks – many who have no idea the accounts even exist!

Leaving your 401k with your ex-employer intentionally is one thing. There could be strategic reasons for doing this, especially if you’re closer to retirement age.

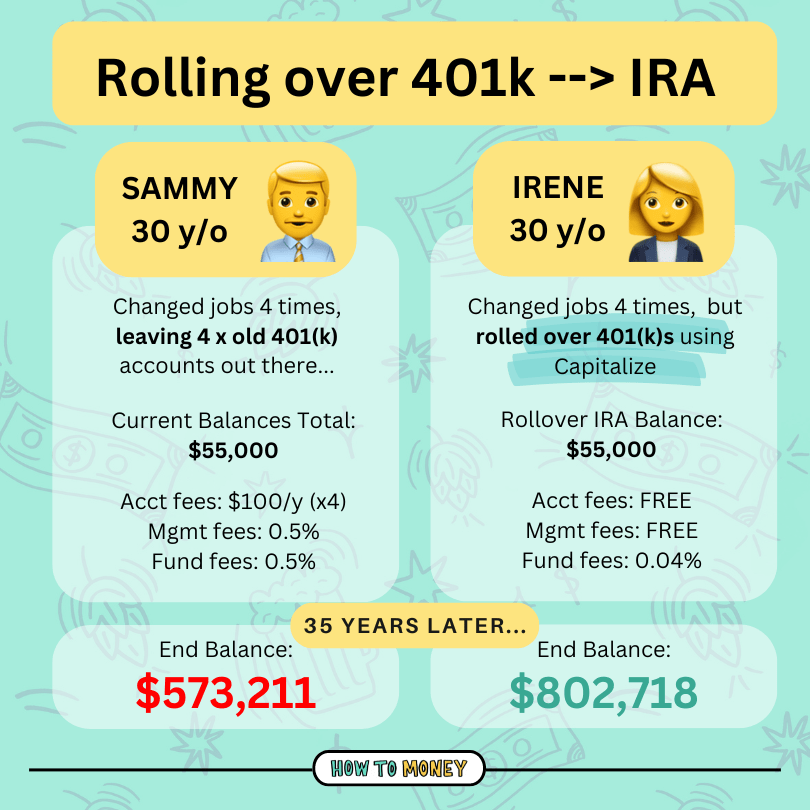

But for the majority of people, rolling over all your 401k funds into an IRA is the course of action.

Why? First, 401k plans can be riddled with administration fees. Why pay those fees when IRAs with the low-cost brokerage firms have none of those fees attached? Also, IRAs have a much wider range of investment options, which means cheaper expense ratios and more flexibility.

Here’s an example of the difference these fees can make over a 35 year time frame…

All in all, while it might seem daunting to perform a 401k rollover, it’s a very important task with easily made mistakes. It could mean the difference of hundreds of thousands of dollars in your retirement nest egg. Never procrastinate when it comes to rollovers.

Mistake #2: Forgetting to Invest and Leaving Money in Cash

This is one of those 401k rollover mistakes that makes me cry…

Basically what happens is people begin the rollover process, but only take it 90% of the way. They successfully move funds from their 401k to a new IRA, but in the final stages when the money lands in the new account, they forget to invest the funds. And that’s the most important part!!

Not investing means the account sits in cash. And there is no growth, dividends, or tax free compounding for multiple years. Here’s a chart showing how common this mistake is, at all age levels…

Crazy, right? Over 50% of 20-something year olds still have their IRAs sitting in cash positions after 7 years. That’s not good.

Do you know what the stock market has done in the last 7 years? It has doubled in value. If these rollover folks had invested in a total stock market index fund, their account balance would be roughly twice the value of what they hold today.

While having some cash on hand is important for emergencies, it’s almost never a good asset for retirement investing. Cash typically earns very minimal interest, often failing to keep pace with inflation.

To avoid this pitfall, always make sure your retirement savings are invested in long term assets that have a proven track record of growth. We love and recommend low cost index funds, because it’s the perfect “set and forget” investment strategy.

Remember, the sooner you invest, the more time your money has to grow. Don’t let your hard-earned savings sit idle – make all your dollars work for you!

Mistake #3: Not Understanding the Tax Implications

Another of the top 401k rollover mistakes that can really hurt your finances: not fully grasping the tax implications involved. While a direct rollover from a 401k to a Traditional IRA is generally tax-free, there are nuances that can trip you up if you’re not careful.

For instance, if your old 401k provider sends you the funds directly (instead of transferring straight to the new IRA broker) your former employer is required to withhold 20% for federal taxes. Even if you plan to deposit the full amount into an IRA within the 60-day window to avoid taxes, you’ll need to come up with that 20% out of pocket to avoid it being treated as a taxable distribution.

Filing the right IRS forms is important, too. Because you need to make sure it is recorded as a qualified rollover. If not, you could be hit with early withdrawal penalties + a huge tax bill. Ouch!

So, if you’re planning a rollover, do your research. Or, consult the firm Capitalize! They can help you with the entire rollover process, at no charge, and make sure all the right IRS paperwork gets filed. It’s hitting the easy button.

Mistake #4: Choosing the Wrong Type of IRA

Picking the right type of IRA for your rollover is important! You can’t just transfer funds between post tax and pre tax retirement accounts on a whim.

The two main types of IRAs – Traditional and Roth – each have distinct tax benefits. A Traditional IRA allows your money to grow tax-deferred until you withdraw it in retirement, at which point it is taxed as ordinary income. It’s very similar to how a regular 401k works, except it’s not tied to any employer. When we talk about regular 401k rollovers, we are usually assuming the funds will be rolled over to a Traditional IRA.

On the other hand, a Roth IRA involves paying taxes on your contributions upfront. But all your withdrawals in retirement are tax-free. If you have a Roth 401k, your funds should be rolled over to a Roth IRA.

If you’re considering converting your traditional 401k to a Roth IRA, be prepared for a tax bill. Since any money that goes into a Roth is done with after-tax dollars, you’ll owe taxes on the 401k amount you convert. Roth conversions can be a strategic move for some (like early retirees using a Roth conversion ladder). But for the majority of people, they should stick to rolling over to like-like accounts.

Traditional 401ks → rollover to Traditional IRAs

Roth 401ks → rollover to Roth IRAs.

When in doubt, consult some fellow money nerds. Like the one’s you’ll find in our free HTM Facebook community.

Mistake #5: Ignoring Fees and Costs

My good friend’s father retired recently. He built a pretty huge nest egg over his long career, and had over $2 million in his 401k when he retired.

A few months after retirement, he consulted a financial advisor who ended up convincing him to roll over his 401k to an IRA with their firm, and invest in a bunch of actively managed funds.

Being a nosey finance nerd, I asked which funds the advisors put his money into, and what their management fees were. Believe it or not, he’s being charged a 1.5% fee for all his assets under management, and they invested his money in funds with nearly a 1% expense ratio. While these percentages seem small, this works out to be about $50,000 a YEAR in fees! Yikes!!!

There are some really good, honest, and smart financial advisors in this world. But charging a retiree $50k a year and not providing much value in return is highway robbery.

Anyway, this story is just an example of how fees are often overlooked and dismissed. Whether it’s small monthly account maintenance fees, trading fees, fund expense ratios or portfolio management fees, they can really add up. Especially over the long term.

To avoid the most fees when rolling over your 401k to an IRA, choose a broker that offers free accounts. Fidelity, Schwab and Vanguard all offer free IRAs and Roth IRA accounts. As for investments, choose low-cost index funds with expense ratios under 0.15%. And for financial advisors, pick flat fee advice from fiduciaries that have your best interest in mind.

Mistake #6: Day Trading (aka Gambling)

401ks have very limited investment options. And that’s for good reason. It’s because employers and the government don’t want people to “gamble their life savings” away. Investors are often restricted to sensible and conservative mutual funds. These are made up of stocks and bonds, matching the age and risk of the account owner.

IRAs on the other hand have almost an unlimited amount of investment options. Account holders can buy/sell/trade single company socks, futures, alternative investments, crypto index funds, and more!

So after a 401k to IRA rollover, it can be tempting to invest in more exciting things. People start to tinker with their portfolio in an effort to ‘hit it big’ with risky trades.

But sadly, day trading is one of the main reasons people lose money in the stock market. Stock picking is almost impossible on a long term basis. You might get lucky with a few trades, but almost everyone loses money trading stocks over the long term.

No matter what accounts you use to save for retirement, be sure to remember that slow, boring, diversified investments are the ticket to growing wealth over the long run. Don’t try to outsmart the system. Invest in index funds and chill.

The Bottom Line:

Rolling over your 401k to an IRA is best for most people who leave their employers. And the sooner the process is taken care of, the more money you’ll save on junk fees and admin costs. But, just because the 401k rollover process seems simple in theory, it’s really important to be thorough and avoid the common mistakes. They can be costly.

From understanding tax implications and choosing the right type of IRA, to actively investing your funds and being mindful of fees, each decision plays a crucial role in shaping your retirement savings. I know it can be boring to take care of financial tasks like this. But your future self will thank you for the hard work you’re putting in today.

Related posts and resources: