Sometimes life happens and you need lots of money in short order. Suddenly, the money you’ve socked away into your 401k over the prior years is looking enticing. Should you borrow money from your 401k to solve temporary money problems?

There’s a reason why they make it difficult to access retirement funds early. Withdrawing money from tax-advantaged accounts is typically accompanied by hefty penalties and tax consequences. That’s because they’ve been set up in a way that encourages you to leave your retirement funds invested for the long term.

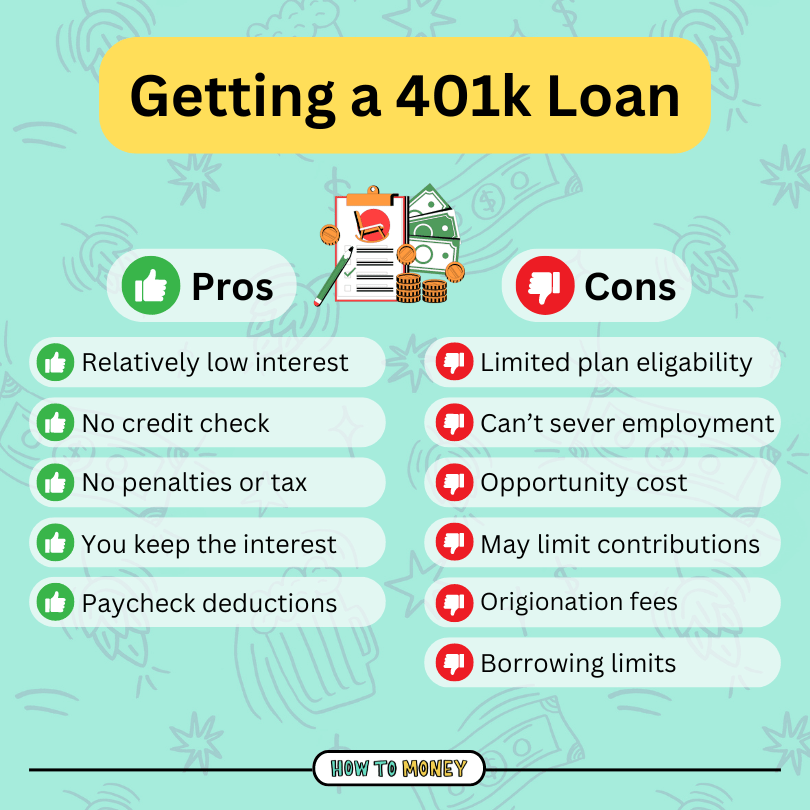

Our advice is: 401k loans should be used only if you’ve exhausted all other loan options. Let’s look at all the pros and cons when you borrow money from your 401k…

What is your 401k?

You know that money is taken out of your every paycheck and gets placed into a 401k, but do you actually understand how they work?

Simply put, your 401k is an investment vehicle that you can use to grow your wealth for retirement. 401ks are awesome because your contributions are made with pre-tax dollars. This means that money goes into a traditional 401k before you pay taxes on it. This minimizes your tax burden with every dollar you contribute because it lowers your taxable income.

Even better, many employers offer a matching incentive. This means they will contribute money to your 401k on top of your individual contributions. For example, if your employer offers a 50% match, they will put in 50 cents for every dollar you contribute up to a certain, specified amount. Translation? FREE MONEY!!

All in all, 401ks are an excellent way to plan for your retirement. But should you ever consider taking out a 401k loan to borrow money from it?

What is a 401k loan?

At your company’s discretion, you might have access to borrow from the money you’ve invested using a 401k loan. A 401k loan allows you to temporarily withdraw money from your 401k account. Then, you promise to pay it back with interest to yourself over a period of time, typically capped at five years. All interest paid goes back into your retirement account.

Not all company plans offer loan capabilities. So it’s important to check with your plan administrator (usually someone in the HR department) to learn about available features.

With a 401k loan, you can borrow 50% of your vested account balance, up to $50,000. You won’t need to pay any penalties or taxes, just the payments and interest back to your account as agreed. In general, you never want to treat your retirement savings like a piggy bank. But in some cases, it could make sense to utilize a 401k loan. More on this later…

401k Loan vs. 401k Withdrawal

A 401k loan is NOT the same thing as an early 401k withdrawal.

In some cases, you may qualify for a hardship withdrawal. For example, you can typically use a 401k hardship withdrawal for medical expenses, funeral expenses, and tuition/education expenses. However, if you take a withdrawal from your 401k, that money will permanently leave your account. You can’t just “put back” the money later. Also, you’ll be hit with a 10% penalty if you’re under 59 ½ years old, and you’ll need to pay taxes on all of those pre-tax dollars you’re removing from your account!

Plus, in many cases, you won’t be able to make additional contributions to your 401k for six months after taking a hardship withdrawal. This can seriously set you back on your retirement investing journey. So it’s important to explore all other available options before taking a hardship withdrawal. If you can pay the money back, taking out a 401k loan is a much better option.

The Downsides of Taking a 401k Loan

Like we said before, your 401k is not a piggy bank. The money isn’t supposed to be touched until retirement. Thus, if you borrow money from your 401k it comes with significant downsides. Here are a few things to look out for before taking out a 401k loan.

1. Some 401ks don’t offer a loan option

First, you’ll need to double-check that a 401k loan is an available option. Although most 401k plans allow you to borrow from your retirement account, not all do. You can check with your plan administrator at work, or refer to the IRS’ website overview of 401k plans.

2. You may need to pay it back sooner than you think

Should you quit your job or be laid off, you could end up needing to pay your 401k loan back prematurely. If this happens, you’ll only have until the due date of your federal tax return to fork up the money you borrowed. So, for example, if you leave your job in December of 2024, you’ll have until tax day in April 2025 to pay off your entire loan. If you’re unable to pay that loan back, it will be considered a default withdrawal. Then you’ll be on the hook for taxes, and a 10% penalty if you’re under age 59 ½.

Even if you feel very secure at your job now, who knows what will happen in 5 years time. So be sure to take your company’s financial stability, as well as your own career plans into consideration before taking the plunge.

3. Factor In Opportunity Cost

Perhaps one of the biggest downsides to borrow money from your 401k is the opportunity cost that accompanies it. When you pull money out of your investments, even temporarily, those dollars aren’t in the market working on your behalf. Even though you’ll be putting that money back into your retirement account over time, that money will have less time to sit and grow. You’re potentially missing big gains if the market performs well throughout your 5-year loan, reducing your retirement nest egg substantially.

When you pay back money on a 401k loan, you’ll pay interest to yourself. So in theory your portfolio may not suffer much in the long term, especially if the market doesn’t perform well. But the main difference is that instead of having your money working for you, accumulating interest on your behalf, your portfolio growth is coming straight from your own pockets!

Because no one can predict what market returns will be like in the future, it’s impossible to know exactly how much taking out a 401k loan could end up costing you by the time you reach retirement. But the potential opportunity cost can be staggering. Reckon with that before you decide to borrow from your 401k.

4. You might not be able to contribute to your 401k

The aforementioned opportunity costs of a 401k loan are exacerbated in some cases. That’s because certain 401k plans prohibit you from making any contributions while your loan is being repaid. If your plan falls into this category, you could be prevented from contributing additional money to your 401k for up to 5 years as you pay off your loan. This can seriously set you back in your retirement investing journey. Not to mention, you won’t be able to take advantage of any employer match or tax advantages!

Plus, even if your plan allows you to continue contributing, you’ll likely have less cash available. Monthly loans payments will eat up a significant slice of your monthly paycheck. This is one of the main reasons we recommend avoiding 401k loans if at all possible.

5. Loan payments are not tax-advantaged

Even though your contributions to a 401k are typically made with pre-tax dollars, you won’t be able to use your loan payments to reduce your tax liability. You’ll pay taxes on your repayment money now, and when you withdraw it in retirement. Total bummer!

6. Origination/Administration fees

If you know anything about How To Money, you know that we hate fees. Some 401k plans require you to pay a small origination or administration fee in order to borrow that money. While these fees are generally pretty modest, it’s pretty ridiculous to pay a fee just to borrow money from yourself.

7. You can only take them at your current job

If you were hoping to tap that old 401k from a job you worked at twenty years ago to put a down payment on your new duplex, think again. You can only take a 401k loan out with your current employer.

Pros of borrowing from your 401k

Borrowing from your 401k does have some benefits when done for the right reasons. Here are a few of the perks of taking out a 401k loan.

1. Relatively low interest

Taking out a 401k loan can make a lot of sense if your credit score has seen better days, as 401k loan interest is typically the prime rate plus 1-2%. This is much lower than most credit card interest rates, and many personal loan interest rates. However, if you have pristine credit, you may be able to get a lower rate if you opt for a personal loan instead.

2. No Credit Check

Again, because you are borrowing money from yourself, there is no credit check necessary for a 401k loan. This also means that taking on a 401k loan will not affect your credit score. A 401k loan can be a great option for those with poor credit who are still working to rebuild their credit score.

3. No penalties and tax

When you withdraw money early from your 401k, you’ll need to pay hefty taxes and penalties. Luckily, with a 401k loan, as long as you pay it off as agreed, you’ll be able to avoid losing more of your hard-earned money to taxes and penalties.

4. You pay interest to yourself

One of the best benefits of a 401k loan is that you pay interest to yourself, instead of to a bank or loan servicer. This allows you to keep more of your money in your hands, and can make a 401k loan an appealing option in certain situations.

5. You have extra time to pay it off if used to buy a home

If you use a 401k loan to pay for your primary residence, you can have more time to pay back those funds. That being said, this can be a blessing and a curse. Stretching out that repayment period means extending the time that your money is removed from your retirement account, potentially stifling its growth even further over the long term.

6. It’s automatically deducted from your paycheck

If you lean a bit towards the forgetful side (like me), you’ll be happy to hear that a 401k loan essentially puts itself on autopay. Just like how your 401k is funded with paycheck deductions, your loan payments will be automatically deducted from your paycheck too. This can help to ensure that you won’t miss any payments.

So, should you borrow money from your 401k?

Try not to! You should always try to avoid drawing on your retirement funds before retirement. However, there are some cases when it could make sense to borrow money from your 401k, and plenty of instances when you should avoid it.

To fund lifestyle purchases:

Unfortunately, many people treat their 401k like a piggy bank instead of the retirement investing powerhouse it is. While it might be tempting to tap into that reserve for things like vacations, cars, or home refurbishments, we urge you to resist the temptation. Tapping your 401k for frivolous reasons could leave you struggling to get by in retirement. Trust me, it’s not worth it. Better to keep saving up instead!

To pay off high-interest rate debt:

If you’ve been struggling to tackle that high-interest-rate debt, you may be tempted to use 401k funds to pay down your debt. Because the interest rate will be lower than credit cards and most personal loans, it could be a good idea to take out a 401k loan, and use the money to pay down your debt.

However, remember that this will ONLY help your finances if you’ve addressed the root of the problem that caused you to fall into credit card debt in the first place. If overspending is still an issue for you, taking out a 401k loan won’t help in the long run. Take steps to start practicing mindful spending, and consider using one of these debt payoff plans instead.

A better option for paying off debt could be to do a balance transfer to a credit card with a 0% APR offer. If you can pay down your debt within the promotional period, you’ll stop that interest altogether, all while leaving your precious retirement savings intact. However, if your credit is in the dumps and you don’t qualify for a new credit card, or your balance is too high to pay off during a credit card promo period, sticking with a 401k loan could be the right option for you.

Related: Will a balance transfer hurt my credit score?

For emergency expenses:

Should you be blindsided by an emergency expense, for example, surprise medical expenses or a pending foreclosure/eviction, your 401k might be a way to get the cash you need quickly to avoid impending doom. However, we would encourage you to use any emergency savings first before you tap that 401k.

To buy a home:

While you can use a 401k loan for housing costs like closing costs or a down payment, you’ll want to seriously consider the consequences before jumping into it.

Borrowing money for a down payment means that you’ll not only be taking on a new mortgage, but also making payments on that 401k loan. Doing this could put a serious strain on your budget if you aren’t careful, so you’ll need to make sure you have enough monthly income to handle this.

If you’re struggling to get a down payment together, you might need to practice patience and keep saving. Also, look instead to a FHA loan or a down payment assistance program. That way you’ll be able to keep your retirement dollars invested and still purchase the home you’ve been dreaming of owning.

The exception? Buying a home you plan to house hack with could potentially yield income you can use to pay back your 401k loan more rapidly.

401k loan alternatives

Before taking out a 401k loan, it’s important to consider all alternatives before plundering your retirement accounts. Here are a few other options to consider before taking the plunge.

Emergency fund/other savings

If you need an influx of cash, the best choice is often to use any emergency savings you have on hand. We recommend creating an emergency fund of 3-6 months’ worth of expenses to help you weather any storm. But even saving up just $2,467 can help you overcome most financial emergencies.

HELOC

If you’re strapped for cash and own a home, you could consider taking out a home equity line of credit, or a HELOC. HELOCs allow you to borrow money from the equity of your home. Typically, most lenders will require you to maintain 20% of your home’s value in equity after your loan, so if you just purchased a home, this might not be your best option. HELOCs typically come with relatively low interest rates and you avoid the sticky consequences of tapping your 401k early.

0% APR credit card

Some credit cards will offer a promotional bonus of 0% APR for a period of between 9-18 months. If you have good credit, and don’t need to borrow too much, opening up a credit card with a 0% APR can be a savvy option. You’ll enjoy 0% interest, and your retirement accounts can continue to grow.

However, this can be risky, because at the end of the 0% APR period, whatever you have not yet paid off will transform into high-interest debt. So crunch the numbers, and make sure you can afford to pay off your balance before that promotional period ends.

Find money in your budget

If you need money to cover a more modest expense, could you find that money somewhere in your current budget? Consider “roughing it out” for a few months using a bare bones budget. A bare bones budget consists of only necessities like food, housing, bills, and transportation, and cuts out all the fun stuff like restaurants, entertainment, and streaming services. 😱

A bare bones budget is not meant to live in perpetuity. Instead, it should be treated as a strategy that you can use to either save up money quickly or to stretch your emergency fund during times of financial hardship. If you need cash within the next few months, make some drastic budget cuts and you can avoid messing with your retirement funds or taking on debt.

The Bottom Line:

When does it make sense to borrow money from your 401k? We only recommend taking on a 401k loan when you need a large amount of cash quickly, and you’ve exhausted your other options. This isn’t a financial move that should be taken lightly, and you should never tap your 401k for lifestyle-related expenses.

It’s best to leave your retirement funds invested long-term. The opportunity cost of taking out a 401k loan could leave you with far less money in retirement. Try to avoid borrowing from your 401k at all costs. However, there are some cases where it might be your only option. Just remember to work towards fully funding your emergency fund to reduce your need to borrow in the future.

Related Posts: