Today’s question comes from Arsenio in San Antonio, Texas…

“I have about $1,000 a month extra that I want to pay towards the house, to get the mortgage paid off sooner.

Another idea I had is… What if instead of the $12,000 annually that I have been paying towards mortgage principal, I was to stick it into an S&P500 account and let it accrue for 5-8 years?

After it grows, I would pull it out and then throw all of that towards the principle in one lump sum.

I don’t know if I’m off on this or not. Any guidance will help. Thanks!”

The short answer:

There are a few ways to look at this. There’s a financial component and emotional aspects to consider.

Financially speaking, investing your money in broad index funds like the S&P 500 is a smarter move over long periods of time vs. paying off low-interest mortgage debt early.

Emotionally, however, living debt-free is one of the best feelings in the world. Prioritizing that goal can be a great lifestyle choice.

There’s no “wrong” decision here. Both options spur you forward and help to grow your wealth. Any savings is good savings!

But is this the exact right path for you?… It’s based on your goals, timeline, and risk tolerance. Here are some things to consider 👇👇👇

Timeline and risk tolerance

First, paying down the mortgage principal is essentially a risk-free money move. It’s guaranteed savings, which are locked in immediately after each payment is applied.

But, investing in the stock market comes with real risk if you’re investing on a shorter timeline. The market can swing up and down wildly in the short term. Over longer periods though, the market tends to generate positive returns.

Some people are very risk-averse and can’t stomach market volatility. If this is you, stick with paying down that mortgage (and other debts!)

For your timeline Arsenio, you mentioned 5-8 years. It sounds like that’s long enough to where investing makes more financial sense. Personally, I’d feel comfortable investing instead of paying down your mortgage.

If your timeline was 2 years, we’d be FAR less inclined to sign off on this investing plan. Things could take a dive quickly, which would put you out of pocket and ruin your early payoff plan for the mortgage.

The good news is that you can also be flexible, right? Once you start investing those dollars, you still aren’t committed to paying off that mortgage early. You can let the circumstances on the ground inform how you proceed.

For example, if you’re at the 7-year mark and the market is in a really tough spot, there’s no need to sell stocks in order to pay off the mortgage.

You can always wait longer until things recover. A flexible timeline is clutch.

Good debt vs. bad debt

We obviously want you to consider your current mortgage interest rate too.

If you’re in the 3% range then there’s no rush to pay it off. I’d just invest every spare penny for as long as possible and pay the mortgage off over the original timeline.

With a low-interest mortgage, even if you can pay it off sooner, you might not want to. Generally speaking, low-interest-rate debt is good debt.

If your interest rate is much higher, say 7%+ for your mortgage, the guaranteed return is a better deal. Paying the mortgage off earlier will save you a decent chunk!

For more info, check out our post on good debt vs bad debt.

Roth contributions

By the way, think long & hard about which accounts you opt to use for investing.

Taxable brokerage accounts are great for shorter-term investing goals like quicker mortgage payoff. There are no withdrawal rules so you can grab that money whenever you like. There are also no contribution limits.

But don’t forget about the Roth IRA! If you aren’t already maxing out a Roth IRA, you can use this awesome account to help you fulfill this mission, while still keeping extra dollars locked away for your future.

How? Well, contributions to a Roth IRA are made post-tax. And the rules are such that you can take out those original contributions at any time in the future, tax & penalty free.

So why not max that account for the next 8 or so years, and pull out the contributions (about $56k in total at that point) to help pay off the mortgage? Just keep the earnings in there to continue growing.

Many people tap into their Roth IRA to buy a house (or pay off debt). It can be a great move! But again, leaving that money to grow for longer in the Roth is much better if you have a locked-in, low mortgage rate.

Why not do both?

If you’re truly struggling to make a final decision, you could also opt to mix a bit of both worlds.

Maybe put $500 a month into an investing account, and use the other $500 to pay down your mortgage?

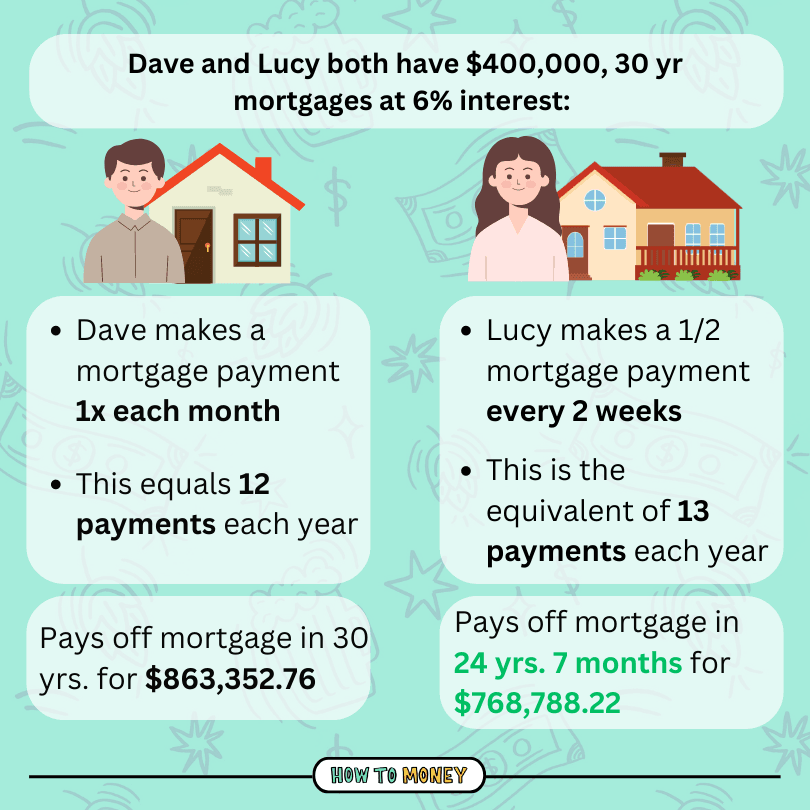

Or, another option is to change your mortgage payments to bi-weekly instead of monthly. By making a half payment every 2 weeks, you actually end up making 13 full payments over the course of a year.

Here’s an example of potential savings…

It’s a sneaky trick to pay down that mortgage faster, without really even noticing the money gone from your paychecks.

With the mortgage on auto-pilot, you can focus fully on investing your excess savings, juicing your returns for the long haul.

The Bottom Line:

I love that you’ve got an extra $1,000 each month & that you want to use it to make serious progress. Good on you! Those dollars can make a big dent in whatever financial goals you might have.

And you’re also thinking long-term here, not about spending this money or taking shortcuts.

We want you to keep debt levels reasonable and own that home outright sooner rather than later. But if your money can be put to more productive uses, why not take that route instead!?

You already came to that conclusion with your question… But we wanted to hammer the point home. Paying off your low-interest-rate mortgage in today’s environment only makes sense if you’re doing it for personal reasons, not because the math makes sense.

Cheers for the question! Happy investing!

For the full version of this discussion, check out Podcast Episode #793 (it’s the 2st question in the episode)

Related posts: