Today’s question comes from Ariel in PA!…

“Hey, Matt and Joel. This is Ariel calling out of Philadelphia, and I have a kind of unique situation this year where I decided to quit my job and take some time for myself.

I had built up some savings and was able to travel and kind of reset. And I wanted to take the opportunity to take some of my 401k earnings (while I have very very little income for this year) and possibly transfer those using a backdoor Roth IRA.

So I was calling to see if you guys had any words of wisdom for how I could accomplish that? Love the podcast and thanks for your input.”

The short answer:

Congrats on your sabbatical, Ariel! Glad you’re traveling and making the most of that time off.

In short, yes! It’s smart to realize any tax gains in extremely low income years, vs. paying them during higher income years. In fact, you might even be under the federal tax threshold for owing any tax at all!

And by converting to a Roth and keeping that money invested, the funds can grow with no additional taxes to be paid ever again.

You mentioned a “backdoor Roth”, but that term isn’t quite right. What you’re actually planning is a “Roth Conversion”. We’ll get into the details below!..

Roth Conversions

Simply put, you’re trying to move existing funds that you funneled into traditional accounts (401k or IRA) into a Roth IRA.

This conversion is a taxable event. Meaning, you will have to pay income tax on all the money that’s converted.

BUT, if you plan things well, and transfer a relatively small amount, you can use that sabbatical (or any lower earning year) to lessen the tax hit. It’s a huge financial win that is definitely in your long-term best interest.

Not making much money will, of course, put you in a lower income tax bracket for your year off. But you’ll need to do some napkin math to figure out what bracket you’ll be in.

One thing to consider is if your sabbatical aligns well with a specific tax year. I know a friend that took 1 year off work, but it was from July → July. So he actually ended up earning a decent chunk of W2 income in both the taxable years he took time off in.

But if you take January → December off, you’ve got a much better ability to benefit from a Roth conversion because your W2 income is next to nothing!

No Tax Threshold

You mentioned avoiding taxation completely if your income is super low. How much tax you’ll be able to avoid on this conversion depends on how much you actually make this year – and how much you opt to convert.

Because of the much higher standard deduction in 2024, you can convert up to $14,600 for single filers & $29,200 if you’re married filing jointly and pay no taxes. This is assuming you made basically nothing in W2 income.

Any dollars converted that keep your AGI under that threshold won’t be taxed at the federal level at all.

But, you might want to convert even more, which can make sense too. If the dollars you’re converting are in the 10 & 12% tax brackets, that’s still an incredibly low tax rate that you might never encounter again!

Once you start moving beyond the 12% bracket, conversions make less sense. You may as well leave that money in tax-deferred accounts and let them compound.

Ultimately, we DO think that rolling at least some of those 401k funds into a Roth IRA could make a lot of sense for you in a low-income year. It would be even more ideal if the market were also down. But alas, that’s not the case in 2024!

How to do a Roth conversion

If you’re converting from a traditional IRA to a Roth IRA, that process is pretty straight forward.

You basically contact your broker and fill out the necessary forms to move the funds. Tell them how much you want to convert, and then they’ll help you process the conversion.

Some brokers even have an online process where you can process the conversion very simply! You’ll need to have both the old IRA and the new Roth with the same broker.

Converting from a 401k to a Roth IRA is much tricker. Because getting those funds out of a 401k is almost always a manual process. They will post you a physical check usually for the funds you withdraw, then you must put those funds manually into the new Roth.

Any rollovers you perform will generate a 1099-R form that you’ll need to file with your taxes. This is super important, because if you don’t handle the filing correctly there’s a chance the conversion will be flagged as a “withdrawal”. This would leave you on the hook for taxes + early withdrawal fees!

We’re big fans of a company called Capitalize. They can be a great resource to help you perform a conversion (or any rollover). There is no charge and they can help assist you through the whole process!

Roth conversion ladder

Not everyone can take a lengthy sabbatical like Ariel, experiencing a year of little to no income.

Still, it’s possible to find smart times to make a conversion that will help you to pay fewer taxes overall, which is a smart part of any thoughtful financial plan.

If you contribute straight to the Roth that can still make sense, but so much depends on how much you make, your AGI, and whether or not you desire that future flexibility.

One technique is to plan a series of roth conversions in small amounts over several years. For younger folks (and in particular early retirees) this strategy is called a roth conversion ladder.

Making those conversions NOW (up to a certain dollar point) in the years in which you are in lower tax brackets will help you beef up your Roth and avoid all future taxation on that money.

And if you choose to convert money that goes beyond the tax-free threshold, just make sure that you’ve got the cash on hand to pay that additional tax come April!

Taking a year off work

Ariel, we love that you’re using the financial independence you’ve gained to your advantage.

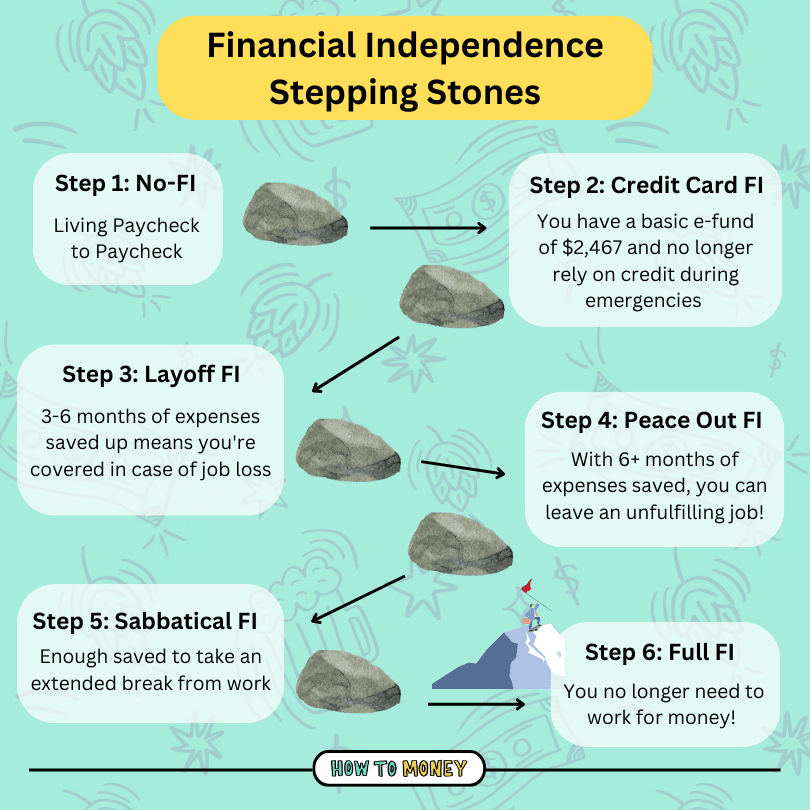

We talk about the stages of FI and the 7 money gears all the time. Taking a year (or two!) off of work is one of those options for folks who are well ahead of the game in saving for retirement.

Reaching financial freedom is not an all-or-nothing endeavor. It’s a journey. One that everyone travels at their own pace.

Using some of your hard-earned freedom along the way is something we encourage.

And we hope that this time off has been refreshing so that you can get out there and kick more butt!

The Bottom Line:

Roth conversions make more sense when you’re taking a year off work. It’s not about using the money and spending it. You’re just shuffling around funds from tax-deferred accounts to post-tax accounts!

Paying a small amount of tax now can help you avoid a much bigger amount of tax later! Or in some cases in years where you earn very little you might be able to avoid taxes completely.

We like where your head’s at, Ariel. Great job thinking holistically about your retirement funds and minimizing your future tax bill.

For the full version of this discussion, check out Podcast Episode #790 (it’s the 1st question in the episode)

Related posts: