Good morning lovely people! Here are a few dad jokes for the holiday week…

- Where does Santa keep his emergency fund? —> In the snow-bank.

- How much does it cost Santa to park his sled? —> Nothing. It’s on the house!

- Does Santa’s workshop have a good 401k plan? —> No, but they offer pretty good elf insurance!

- What type of credit cards points does Santa like best? —> He likes ho-ho-hotel points.

OK, that last one was a stretch. But my kids laughed at it, and that’s all that matters this week 😉

(I promise the rest of the newsletter won’t be as lame). Let’s get to it! 👇👇👇

TO DO

Start Next Year’s Sinking Fund

This week: Start a sinking fund for *next year’s* holiday presents. (yes, for real)

I know you’re likely still finalizing this Christmas’ events and items, but the best time to begin planning for next year is while it’s all fresh on your mind! And the earlier you start, the less you have to save monthly, and the less it hurts your wallet.

Set aside an account, an envelope, or digital money bucket and start moving small bits of cash into it. You’ll thank yourself in Dec 2023!

HOUSING

To Buy or Not To Buy?

Following last week’s theme on contradicting market predictions for 2023, I came across this really interesting read from WSJ about how confusing the housing market has become.

“Home buyers and sellers are trying to make sense of a downturn that’s full of contradictions: Demand has seized up but supply is still low; prices are sliding but not plummeting; and no one can agree on what comes next”

It’s really hard to know what the future looks like. There are SO many factors at play for house prices.

But, while it all might seem out of your control, much of the decision to buy (or rent) a home is about your personal situation. Here are a few factors to consider and evaluate in your life:

- Your money situation (duh): If you don’t have the downpayment or income to support a purchase, then that’s that. Harsh reality check, but if buying a home will financially stretch you, then it’s better to just wait and keep saving/earning. (And in most of the country renting is cheaper than owning right now anyway)

- Your time frame: Are you willing to commit to a 7-10+ yr period living in a home once you buy it? Most people think the answer is yes, but a LOT can happen in 7 years with the uncertainty of your career/health/family and time can heal an ill-timed financial move.

- Responsibility: The ongoing duties of a property owner are inescapable. Before buying a home you need to be honest with yourself and make sure you’re ready to tackle (or pay for) maintenance/problems/upgrades.

- FOMO: Don’t succumb to recency bias. For any investment, remember “past performance is not indicative of future returns.” That’s true of home prices too. Could they continue to go up? Sure! Will they continue to increase at a double-digit pace for years to come? Probably not. Don’t let whatever has happened in the last 24 months cause you to feel financial FOMO and make a rushed decision that isn’t right for your specific situation.

All in all, there’s no one-size-fits-all guidance on purchasing a home. But don’t ignore your personal factors, they are more important than whatever weird stuff the housing market is doing.

Also check out:

- 💻 Lending Tree: Rent vs. mortgage payments in the 50 largest metros

- 🔢 Calculator: How much house can I afford?

- 👩💻 Blog post: Your house is an awful investment

- 🎙️ Megapost: Pros and cons of renting vs. buying(including 8 questions to help you decide)

TOGETHER WITH CARDRATINGS

Search Tool FTW!

Joel was playing around with our new credit card tool the other day, thinking about opening a credit card for Southwest points (planning for a family vacay over spring break!)

Anyway, something cool happened. When he clicked “Southwest” as the points preference, it recommended the Chase Sapphire Preferred card as the top choice, not the Southwest credit card. After looking into it further, it seems the welcome bonus for Chase is higher than the Southwest card (and Chase points can convert to Southwest points easily for a 1:1 transfer). This recommendation means an extra 10k in points. 🥳

It pays to do comparisons! If you’re considering opening a new credit card in the near future, give this search tool a whirl. It’s kind of fun, too. 😉

INVESTING

It’s About Time-in, Not Time-ing ⏳

A big reason people don’t invest in the stock market is because they are scared to lose money.

That’s totally understandable. The risk of losing money is real, and so are the scary feelings…

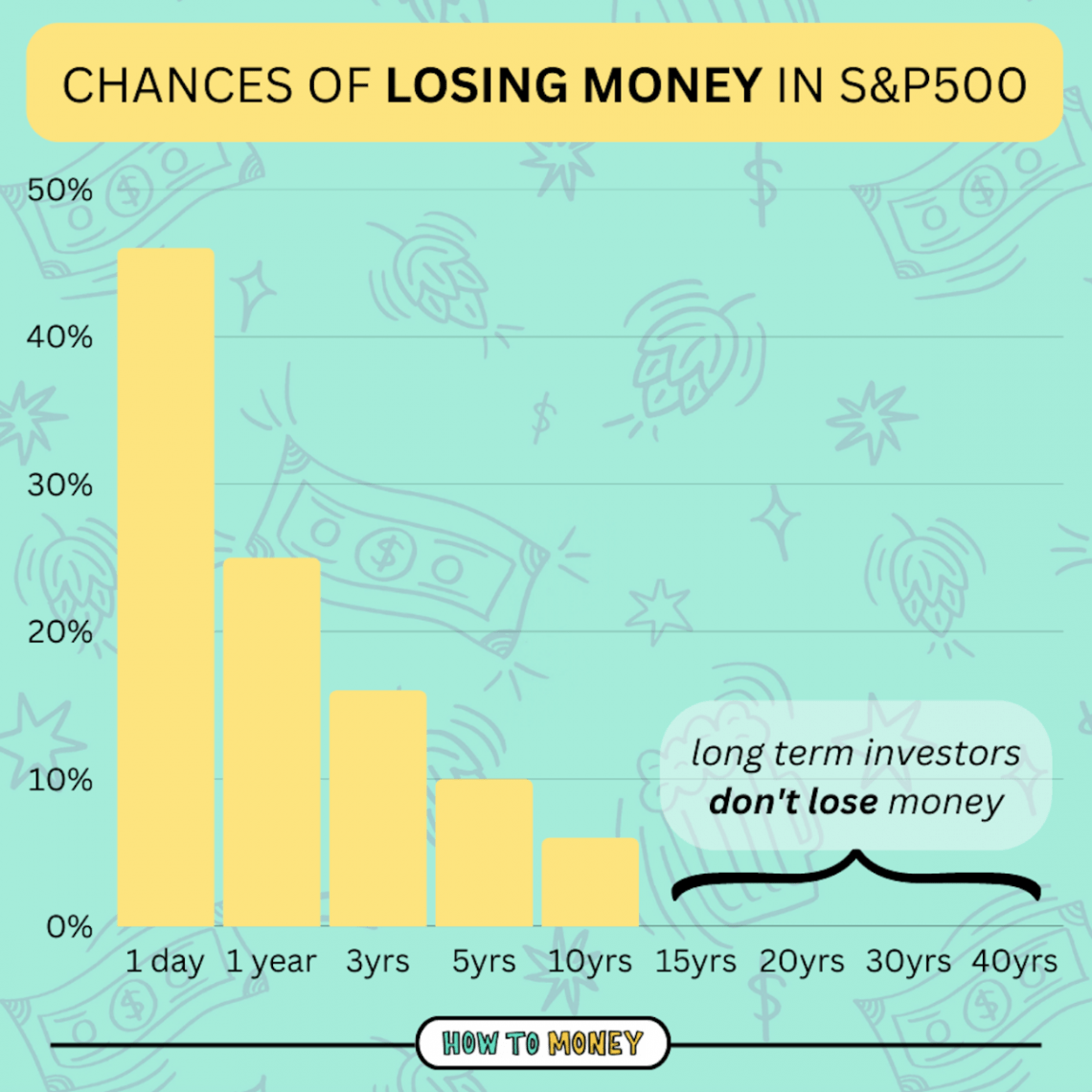

But, one thing most people don’t understand are the actual mathematical chances of losing money. Here are some investing odds based on rolling historical S&P 500 data. 👇👇👇

If you invest for just 1 day, the odds of you making or losing money are almost the same as flipping a coin. The stock market has good days and bad days.

If you invest for 1 year, the odds of losing money drop to 26%. The stock market has 3x more good years than bad years.

3 Years, 5 Years, 10 years… the chances of losing money continue to decrease down to 16%, 10% and 6% respectively.

Then around the 15 year mark, something funny happens… The chances of losing money in the stock market become about the same as you landing a hot date with Chris Hemsworth. Zero.

The bottom line is: It’s incredibly hard to lose money as a long term investor (if you invest in a low-cost broad market index fund!). Yes, the journey will be scary, especially in the first few years. But the longer you remain invested, the more that feeling fades away.

Related stuff:

- 💻 HTM Blog: 6 Reasons why most people lose money in the stock market

- 📖 Book Rec: Simple Path to Wealth, by JL Collins

- 🎧 Podcast Ep #175: Simple & smart investing (a great episode if you’re scared about losing money)

ICYMI

Supplemental News Bites…

30 yr fixed 📈

Mortgage rates have been ticking down recently, closer to 6% (vs. recent highs of 7%). That’s still a LOT more than they were a year ago, but great to see. Btw, if you are buying, don’t forget to shop around for rates. According to Freddie Mac, “buyers could save an average of $1,500 over the life of the loan by getting just one extra rate quote”!

Car insurance 🚘

Sadly, all our car insurance premiums are likely to increase in 2023 by about 7% on average, due to more expensive vehicles and higher crash rates. Something to plan for when estimating your 2023 budget!

Free returns ❌

According to The Washington Post, the era of free returns might be coming to an end (at least for online sales)… Many retailers are tightening their belts due to a 13% increase in returns from last year.

Venmo 1099-K ⚖️

If you received more than $600 for goods and services via Venmo, PayPal, Amazon, Square, or a similar platform this year, you will probably receive a Form 1099-K to file with your taxes. Don’t freak out, this only applies only to payments received for “sales of goods and services” (not transferring money to friends and family). As a reminder: All income must be reported to the IRS anyway, whether you receive a 1099 or not.

Inflation 👍👎

Although last month’s report showed inflation cooling overall (down to 7.1%), certain categories that make up the data were higher than others… Airfares, home energy, and pet products saw the biggest increases.

FRIENDS OF HTM

Joshua Becker – Own Less, Live More!

We met Joshua years ago at a money conference and were instantly impressed with his sincerity and down-to-earthy-ness (is that a word? — it is now!)

On top of his popular blog, Becoming Minimalist, Josh has written 4 books on minimalism and intentional living, and he also founded a non-profit called The Hope Effect, helping kids in orphan care.

As we enter 2023, perhaps you’re interested in living a more intentional year with less clutter and more happiness… If so, check out Josh’s site, or listen to our interview with him on episode 525!

Wishing you a very happy holiday! Remember, the best way to have yourself a merry little Christmas —> is to center it around what everyone else wants.

Best friends out 🍻

*****

* Advertiser Disclosure: How to Money has partnered with CardRatings for our coverage of credit card products. How to Money and CardRatings may receive a commission from card issuers.