We all make the occasional money mistake. Some missteps are small and the impact they have is a tiny blip on our radar. Other bigger common financial mistakes can be like an albatross weighing us down for years to come.

In this post we’ll break down the most common financial mistakes people make that frequently lead to serious money troubles. Even if you’re already struggling financially, avoiding these pitfalls could help you achieve a life of financial freedom.

Whether the screw up is small or big, it’s important to learn from them quickly so we can move on and start kicking butt with our money again.

1. Spending More Than You Make

One of the most common financial mistakes is living above your means. We’ve all heard the cliched advice, “Don’t spend more than you make.” However, sometimes that’s easier said than done. Large fortunes are frequently lost a few dollars at a time.

It might not seem like much at the moment. You might even say to yourself, “It’s only $10,” but every item adds up over the long haul. Running late for work, you grab a coffee from your favorite vendor ($5). Oops, you forgot your lunch, you’ll have to eat out today ($25). Your coworkers are knocking off early and grabbing drinks at the bar downstairs ($20). You go home and pay to watch that Oscar-nominated movie on your favorite streaming service to unwind after a hard day ($10).

Let’s say the previous example costs you $60 for all those items. If you have a day like that only once a week, it will cost you $3,120 per year! That’s extra money you might not have in which you could be putting on a credit card and potentially paying enormous interest rates!

How to Avoid → You don’t need to cut out things that bring you joy. But you should develop a budget to track your expenses and income. Here are some different budget strategies – these will help you avoid overspending.

Opting for a more minimalist existence will help a lot also! This involves replacing disposable items with unforgettable experiences. Minimalism is defined by “owning fewer possessions” and “living intentionally” with only what you need or value most. Financial minimalism is simply buying less and saving more for important goals or things that bring real value to your life. It all comes down to asking yourself, “Do I really need this?”

2. Not Budgeting (Or tracking your spending)

A budget allows you to control your money. Without one, guess what happens? Your money controls YOU!

You’re not alone if you aren’t budgeting. Sadly, only 32% of U.S. households keep a monthly budget. It’s no wonder so many folks are living paycheck to paycheck!

It’s usually easy to determine where all the money is coming in from (income) but sometimes challenging to track where it’s being spent (expenses). It’s often expenses like subscriptions, eating out, entertainment, and transportation that deplete your finances quickly.

How to Avoid → Don’t be like my mom who used to always said, “I hate budgets. It goes against my nature.” We are fortunate to live in a digital world where we have countless budgeting tools at our disposal!

No more pen, paper, or calculator (unless that’s your thing). Personal budgeting apps like Mint, Personal Capital or YNAB (You Need a Budget) are all user-friendly options. Budgeting will help you take control of your spending and potentially reveal which habit you might need to break.

3. Having No Emergency Fund

An emergency fund (or rainy-day fund) is simply insurance against debt. Life happens and we can never plan for everything. That’s why they’re called “unexpected” expenses.

Having an emergency fund in place is critical. Without one, you may find yourself resorting to short-term solutions you may regret down the road. Examples of events that lead to unexpected expenses include:

- Losing your job

- Urgent medical procedures

- Emergency home issues

- Sudden car repair bills

- Death/funeral expenses

- Pet emergencies/vet bills

- Unexpected tax bills

- Natural disasters

How to Avoid → Check out this ultimate guide to emergency funds. It includes a bunch of different ways to save for emergencies and where to keep your cash. In short: We recommend saving a minimum $2,467 in savings, but eventually growing that to about three-to-six times your monthly expenses. This will protect you from entering a financial crisis if you lose your job or have to move across the country unexpectedly.

4. Lifestyle Creep

Lifestyle creep happens when you get pay raises and immediately increase your spending to match. Just because you got a raise or a bonus doesn’t mean you should head to the car lot to spend it in one fell swoop on a brand new Bronco!

The reason lifestyle creep is one of the most common financial mistakes is because it can cancel out broader financial goals such as preparing for an emergency, contributing to a retirement fund, or saving for a down payment on a home. Unknowingly, your newfound lifestyle may take precedence over your financial security. Even if you earn a nice salary, you may find yourself living paycheck to paycheck or incurring unmanageable debt.

How to Avoid → Put your pay raises (and bonuses) directly into savings. Or, get into the good financial habit of only spending a portion of your pay increases. For example, consider implementing the 50/50 rule which is using at least half of any extra money you earn toward saving, paying off debt, or investing, while the other half should be spent however you want! As a result, you’ll reach your financial goals sooner, as well as improving your lifestyle. Win, win!

5. Waiting Too Long To Start Investing

Another classic money mistake is delaying investing and retirement planning. When you’re young, it’s difficult to grasp the concept and importance of retirement because it seems like it’s a lifetime away. Ah, the naivete of youth.

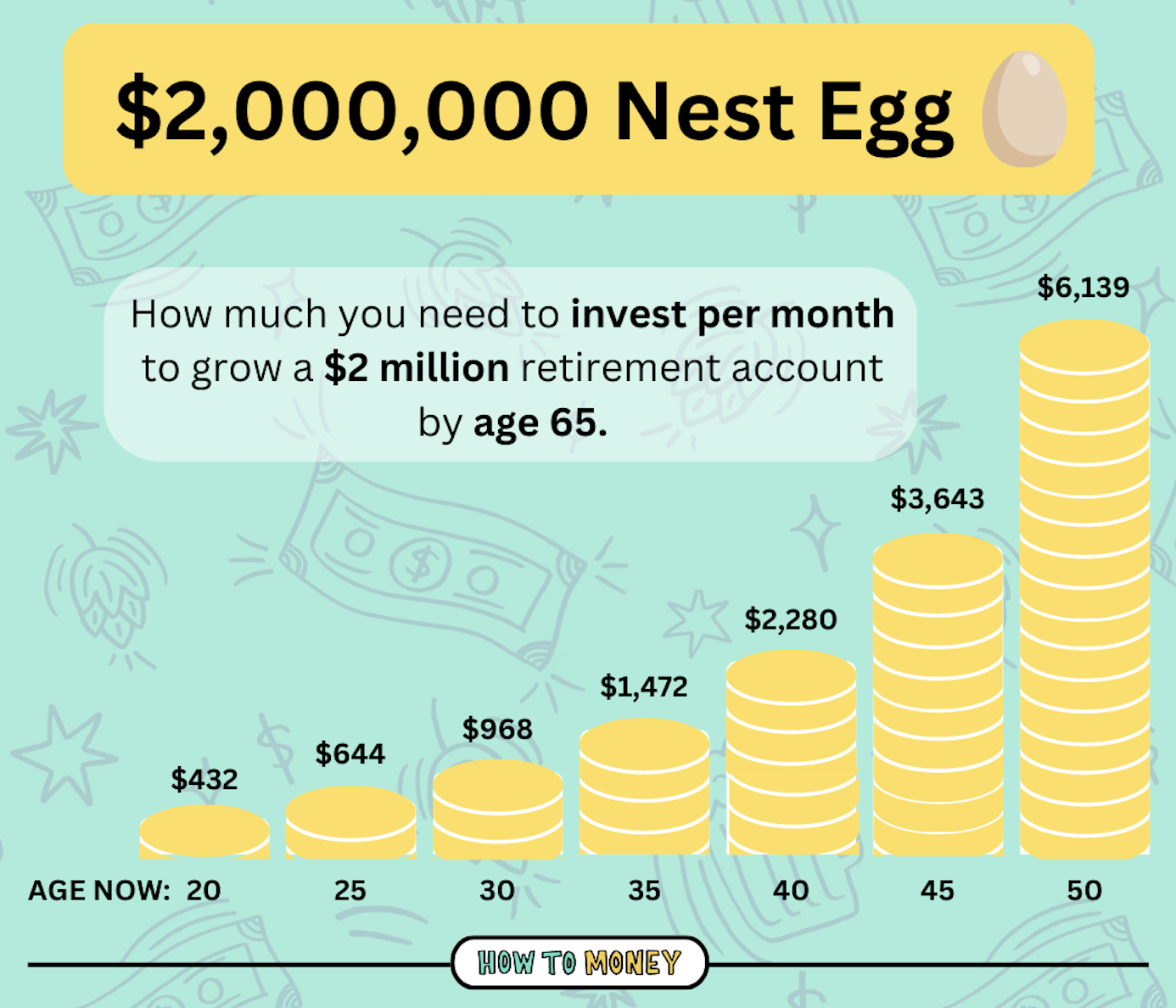

But delaying only makes it harder for you later. Here’s an illustration of the monthly savings it takes for people at different ages to grow a retirement nest egg. As you can see, the earlier you start investing the less you need to put aside.

NOW is the time to have your money working for you or else you may never be able to quit working! Making monthly contributions to targeted investment/retirement accounts is essential so that you can reach your financial goals and achieve financial independence.

How to Avoid → Take advantage of tax-deferred and tax-exempt retirement accounts! Examples include your employer sponsored 401(k), Traditional IRA, and Roth IRA or Health Savings Account (HSA). Find out if your company matches any of your contributions to your 401(k), then consider maximizing the amount you contribute. Remember the more time you give your investments to grow, the more you have the potential to earn!

6. Spending Too Much on Housing

Housing is one of the top expenses for most of us. It’s easy to spend too much on housing – especially if you live in an expensive city. But here’s the thing, bigger is not always better. A 5,000-square-foot home comes with more costly taxes, maintenance, and utilities.

How to Avoid → The general rule of thumb is not to spend more than 30% of your pretax income on a house. This of course depends on your personal financial situation and the goals you have with your money. Consider living with roommates or in a less expensive part of town to help bring your costs down.

While real estate does help grow wealth over long periods of time, your house is rarely a good financial investment. In many cases it’s cheaper to rent than to own – as long as you are continuing to INVEST your excess income.

7. Buying a New Car

Cars are a huge money pit for most American families. When you buy a new car, the value drops by as much as 30% as soon as you drive it off the lot. For most car purchases that is akin to incinerating thousands of dollars.

And it’s even worse if you borrow money to buy a new car… This means you are paying interest on a depreciating asset! Folks who trade in a vehicle every few years end up losing money consistently, impacting their ability to build wealth and retire comfortably.

How to Avoid → Buy used, reliable vehicles and keep them as long as you can. In doing so, the depreciation has already come out of the previous owner’s pocket – not yours. Additionally, the loss of a car’s value is significantly less from years three to six than from years one to three, which means you’ll get more of your money back when it’s time to sell.

8. Not Having Proper Insurance

Having the right insurance is key to good financial planning. Sadly, most people are underinsured for life insurance, overpaying for car insurance, and possibly getting ripped off for insurance products they don’t need (like Universal Life Insurance).

While it can be difficult to navigate insurance types and coverages, not having the right balance of insurance (and price!) can wreak havoc on your finances.

How to Avoid → For car and home insurance, shop around annually to make sure you have the cheapest policy available. Insurance carriers don’t give you loyalty discounts! For life insurance, purchase Term Life Insurance policies to make sure accidental deaths don’t leave loved ones in a financial crisis. Renters and Landlord Insurance are necessary to protect your living situation and property.

Review all your insurance coverage annually to figure out which policies you need based on any major life events you’ve experienced. For example, if you’ve purchased a new, more expensive car, it’s time to reevaluate your auto insurance. If you’ve recently gotten married or had a baby, you’ll likely want to review your health insurance. Make sure the insurance you have will cover the value of your assets so that you aren’t leaving your finances exposed.

9. Not Negotiating or Shopping Around

When it comes to major purchases, people forget to shop around, not realizing how much money it could save them. Most folks are too scared to ask for an additional discount on an item they’re looking to purchase too. This means that we’re often paying more than we need to for the items we’re buying.

Many places offer unadvertised cash discounts – you just have to ask! Always paying sticker price has serious financial consequences.

Sometimes just googling for price comparisons or searching deal websites can save you meaningful bucks on something you are planning to buy.

Speaking of negotiating and getting better prices, another common financial mistake individuals make is not negotiating their salary before starting a new job!

How to Avoid → Get comfortable asking for discounts. Here are 11 tips to get you started – the worst they can say is “No.” Regarding salary negotiation, start with a number that is higher than what you’d expect, so you have wiggle room to negotiate down to the actual figure you would accept. Again, the worst they can say is no!

Also check out these podcast episodes:

- Negotiation as a winning everyday tactic

- Maximizing your income in 2023

- Proven ways to reduce your rent (with Justin Pogue)

10. Lending Money to Family and Friends

Lending money to friends, especially when you can’t afford to part with those dollars, is ill-advised. It creates awkward relational dynamics where you find yourself tallying up their spending and thinking “that money could have been used to pay me back” every time they make a purchase.

Also, it often leads to them asking for more money, later. Since you said yes the first time, you might feel obligated to say yes again, which digs the hole even deeper.

How to Avoid → Simply don’t do it! Lending money to family and friends will inevitably lead to that awkward conversation where you have to ask for your money back. There are a TON of other ways for people to borrow money – via banks, personal loans, etc. Direct them to those other methods and support them that way.

If you really want to help someone financially, try this idea… Let’s say a friend asks to borrow $1,000. Instead of “loaning” them the money, tell them you’re happy to help out but you can only give them $500 (or any amount less than their asking price) as a “one-time gift.” Meaning, you will not be asking for the money back. However, they need to ask others for the remaining money they need. Give that money as a gift – if you can afford it. That changes the whole dynamic of a potentially clumsy situation.

11. Not Monitoring Your Credit Report

Credit scores can impact you more than you realize. From borrowing money, to buying a house, and even renting an apartment. Having a higher credit score gives you a financial advantage!

When taking out a loan, your credit score can affect what type of interest rate you receive. For example, the better your credit score when buying a house, the lower the interest rate you should qualify for – meaning less money for you to pay back!

Also, with identity theft at an all-time high, regularly checking your credit report can quickly catch any fraudulent charges or accounts opened under your name.

How to Avoid → Review your credit report and score on an annual basis, at minimum. Credit Karma is a great site that will allow you to check your credit score for free. It also offers advice to help you raise your score. AnnualCreditReport is another great site that gives you access to your credit report each and every week for free. If you spot any errors you can easily report them to the three main credit bureaus – Equifax, TransUnion, and Experian.

12. Trying to Get Rich Quick

Whether it be winning the lottery or picking a unicorn investment, people are obsessed with the idea of making millions overnight. They constantly throw good money into ideas and schemes that have ridiculously tiny odds of succeeding. We’re looking at you, made-up internet meme coins!

How to Avoid → Don’t buy lottery tickets. It’s one of the most common financial mistakes and is like throwing money down the toilet. Your chances of winning are 20,000 times less than you getting struck by lightning! Instead, invest your money into proven, mature investments. Educate yourself on how most people lose money in the stock market – and then do the opposite! (Buy broad, low cost index funds) If something sounds too good to be true, it usually is. The slow, boring, simple route is the surefire path to building wealth.

The Bottom Line

Nobody’s perfect, especially when it comes to money. It’s OK to make mistakes. What’s most important is learning from them and understanding how to not repeat them.

Hopefully, these tips have given you a starting point to avoid the most common financial mistakes and stay out of trouble. With a little mindfulness and care, you can build solid money habits that make financial freedom much easier to attain.

Related:

- 5 biggest financial regrets people have in life

- Debt snowball vs. avalanche payoff methods

- How to buy index funds for beginners

Beer notes: While covering the common financial mistakes on this episode, we enjoyed a Hydrus Double IPA by Two Tides Brewing! And as we’ve ramped up the podcast with an additional Friday episode every week, we could really use your help to spread the word- let friends and family know about How to Money! Hit the share button, subscribe if you’re not already a regular, and give us a quick review in Apple Podcasts or wherever you get your podcasts. Help us to spread the word to get more people doing smart things with their money in these difficult times!

Best friends out!