When I was growing up, my dad used to always tell me that there was “no such thing as a free lunch.” He wanted to teach me that everything has a cost. And that if something seems too good to be true, it probably is.

Pops was pretty much universally right in all aspects except for one… 401k matches!

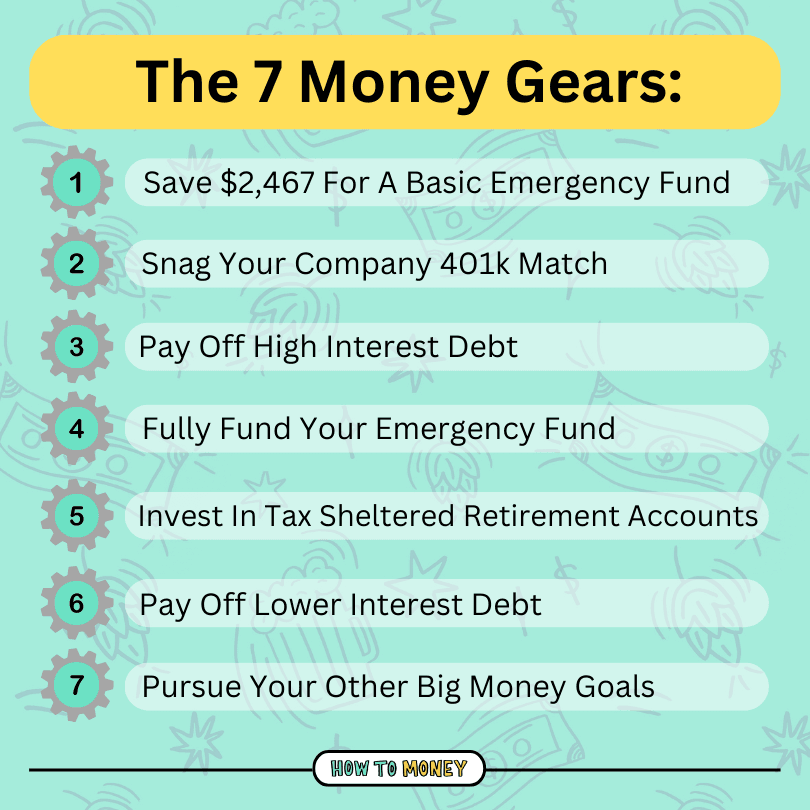

The money gears are kind of like our “one size fits most” roadmap to financial success. They help folks figure out exactly what money moves they should focus on based on their current financial stage.

Each “gear” is a mile marker along the winding path to financial freedom.

While gear 1 has you saving a basic emergency fund, money gear 2 is all about beginning your investing journey by taking advantage of your company’s 401k match!

BTW – if you haven’t cycled through Money Gear 1 yet, go back and complete that first. It’s really important to follow the steps in order!

401k Matching

A 401k match is perhaps the only time in your life where you’ll be offered free money. The only catch is YOU have to pony up some of your paycheck too, before your company contributes.

It’s a way to incentivize employees to save more for their retirement. And it works!

Sadly, not all employers offer 401k matching incentives. And some programs are better than others.

For example, a large tech company employer might offer $1 matching for every $1 you put in up to a maximum 8% of your salary. This is an awesome perk!

If you earn $100k per year and you sacrifice $8k towards your 401k, your employer will put in another $8k. This is a huge perk that will rapidly increase your wealth-building progress.

Other employers might only offer a 50% match for each dollar you contribute, up to 5% of your salary. The incentive is much lower, but it’s still free money!

Taking advantage of whatever your employer offers should be a high financial priority.

Why? Because it’s the best ROI you can get on your money. Dollar-for-dollar matching provides either a 50% or 100% return on investment. It’s a no-brainer!

What if I don’t have a 401(k), or an employer match?

If you don’t have access to a 401k, go ahead and skip this money gear.

While it sucks that you don’t have this killer perk, there are other ways to save for retirement without a 401k.

If you do have a 401k, but your company is too tight to offer a match, that’s OK too. There will be plenty of opportunities for you to invest later on! Go ahead and skip right to money gear 3 and work on paying off all high-interest debt.

How exactly do 401k matches work?

A 401k match is when your employer puts extra money into your 401k as a match to the amount YOU put into it.

When you put money in, they do too. That’s the only way to get the free money.

First, you need to designate a certain percentage of your paycheck to be socked away into your 401k. This is done by working with your company’s HR department.

The money is taken out of your paycheck before it reaches your bank account. But it’s done so pre-tax!** Which is another perk of having a 401k.

Every employer has a different matching program. So you’ll need to check with your benefits officer to find out exactly how to maximize the matching incentive.

It’s worth noting that 401ks are not the only accounts that might have matching programs. Some jobs will offer you a 403b account with a match, which essentially functions the same way.

**Another important note is that 401k’s are not always pre-tax. It’s the most common option, but Roth 401k’s exist with some employers and are growing in popularity!

Maxing out your 401k

If you have a massive salary, you might want to contribute a huge chunk of it to your 401k!

In 2024, the maximum you can contribute to a 401k is $23,000.

But any money contributed by your employer does not count towards that limit. The combined limit for all 401k contributions cannot exceed $69,000 for folks under 50 years old, or $76,500 for those over 50.

But we’re getting a bit ahead of ourselves. Maxing out your 401k comes later in the money gears.

Right now we’re telling you to only focus on the matching component.

If your company offers matching up to 3%, contribute 3%. If it’s 8%, then you should contribute 8%. Whatever the maximum benefit is, make sure you’re fully taking advantage of it.

Watch out for vesting schedules

Unfortunately, some employers put terms and conditions on their matching dollars.

These are called vesting periods. Basically, it’s when the employer says you need to stay at the company for a certain amount of years for their match to become fully effective. If you quit or get fired sooner, they revoke the match!

While they want you to invest for retirement, your employer likely isn’t too keen on you snagging their free money and then dipping out. This is all part of their golden handcuffs plan.

Vesting periods vary from employer to employer. For example, 25% of your match might become permanently yours after a full year of work, followed by an additional 25% each year until you reach four years of work service.

If you were to quit after two years for example, your employer would take back 50% of the money they matched in your 401k.

Other employers may take a more “all or nothing” approach to vesting. Like allowing you to keep all match money after three years of working for the company.

Hopefully you don’t have a vesting period at your workplace. But if you do, make sure to think ahead about whether you’re likely to be working there in the next couple years or not!

The difference an employer match can make

We want to illustrate just how valuable employer matches are. They can have a huge impact on the amount of money you will ultimately retire with.

Let’s say your employer offers a simple 3% match to your 401k.

You might think that 3% isn’t really that much. But compounded over decades it adds up to a massive amount!

Let’s say you make $75k a year, and you contribute 3% of your salary to your 401k. (That’s only $87 per paycheck BTW!!!)

And let’s say your employer matches that 3% too. Here is what that will look like over 40 years…

Obviously there’s a lot of assumptions baked in here.

You probably won’t stay in the same job with the same salary for 40 years. You’ll be getting pay raises, contributing more, etc.

This is just showing the power of matching. Especially when you’re young!

Here is a 401k matching calculator you can play with yourself if you want to use your own inputs or estimations.

How to Get Your Company Match

Here’s a quick review of the steps you should take in money gear 2.

Step 1: Find out if your company has a 401k match incentive

You know those boring papers you signed when you first got the job? Your benefits were probably all laid out in that package.

But if you threw those away already (I don’t blame you), just head to your HR department or ask your manager if your workplace offers a 401k.

Most companies hire an outside benefits provider to manage the process. Your 401k might be administered by a big broker, like Fidelity, Vanguard, or Empower.

Step 2: Figure out how much you need to contribute

Next, you’ll need to figure out exactly how much you should contribute to take advantage of the full match.

Usually 401k contributions are a percentage of your salary, not a specified dollar amount. So it’s pretty easy to just select the percentage to deduct, and your employer calculates the exact dollar amount on the backend.

Some plans are super simple. Like, “match up to 4%”. In this scenario, you simply set contributions to equal 4%.

Others are more complex. Like, “match 50% up to the first $5000”. In this scenario, you’ll want to use your salary to figure out how much you need to contribute to get that full $5,000 incentive.

If you’re confused, that’s OK! Your HR department can help! Or ask a knowledgeable co-worker.

Or, why not join the HTM Facebook Group and ask for advice from our community?

Step 3: Make room in your budget

Since 401k contributions are taken out of your paycheck automatically, you’ll need to figure out a way to live on a tiny bit less.

But it’s way easier than you think.

If you don’t have a budget yet, we recommend starting with a 50/30/20 budget. The simple structure is perfect for beginners.

Taking the time to create a budget will be essential for accomplishing all of the money gears from this point on.

If you’re currently living paycheck to paycheck, you’ll need to find ways to cut your monthly expenses. Try negotiating your bills, switching your phone provider, canceling unused subscriptions and watching your energy consumption.

I know it’s hard to make cutbacks. But you can rest assured knowing that every dollar you are socking away for retirement is being matched by your employer. So all savings have a double value effect!

Step 4: Enroll in your 401k (If you aren’t already)

Almost all employers will be required to automatically enroll new workers in their 401k plan starting in year 2025.

But if you joined years ago, you might need to manually enroll in your 401k plan.

Again, this is simply done by working with your HR or benefits department.

Part of your enrollment is setting your contribution amount. This is where you input the number you already calculated in Step 2.

You can always change this later. And you’ll want to in the future when you get pay raises!

Step 5: Choose your investments

The other part of enrollment is setting up investments.

One of the best parts of 401k investing is auto-investing. This means you only need to choose your investment options once. After that, all future contributions will be automatically put in those same investments.

401ks are notorious for having horrible investment options. But that’s starting to change these days as index funds become more popular.

If you’re confused about which investment options to select, read our beginners guide to investing. And also check out this post on how to buy index funds! It includes our favorite funds to choose inside your 401k account.

Here is also a cheat sheet for index funds at our favorite low-cost brokerages!

Step 6: Set and forget!

Here comes the hardest part… Waiting and doing nothing!

Building wealth takes time. So you’ve gotta be patient and let those investments do their thing.

While it might be tempting to withdraw money from your 401k when emergencies pop up, or to take that fancy vacation, it’s important that you leave the money in your 401k invested.

You’ll get hit with a big penalty for early withdrawals. Not to mention using your 401k as a piggy bank is a good way to go broke later in life!

What Next?

There are still a lot of money gears to cycle through. Snagging your 401k match is a great second step, but it’s not the only investment you should rely on for a comfortable retirement.

You’ll want to save a lot more. Especially if you are older and don’t have much in the way of savings.

While it never hurts to contribute more to your 401k (above the match amount), there are some other important financial to-dos we want you to take care of first.

We’ll revisit your 401k at money gear #5. But for now it’s time to move on to money gear #3 and work towards paying down high-interest debt.

The Bottom Line:

Getting a 401k match is probably the most important first step for investors. While it might seem like a small perk, it has huge ramifications over a long timeline, adding hundreds of thousands of dollars to your eventual nest egg!

Sadly, not all employers offer a 401k program, or a matching incentive. That’s particularly true for folks who are self-employed, obviously. But don’t worry, there are still a ton of money moves and other tax-incentives you can jump on. It’s all a matter of following the money gears in order.

Related Posts: