Emergency preparedness. It’s something we’re taught from a young age. Between fire drills in school or pointing out emergency exits on flights, we learn the importance of preparing for the unexpected.

But what a lot of people don’t realize is that it’s important to do the same with our finances!

We created the 7 Money Gears to help people follow an easy path to financial success. By shifting through these gears (in the correct order) wealth builders will create a smoother financial ride. 🚴🏻♂️

This post is all about that very first important step. Saving a simple emergency fund.

Money Gear 1: Saving a Basic Emergency Fund

Emergency funds are savings you set aside for surprise expenses you can’t plan for.

Having that cash on hand is the first step towards financial independence because it protects you from having to take on debt to cover emergency expenses.

You’ll also enjoy more peace of mind with an e-fund, and be less stressed when emergencies do pop up.

If you’re a financial n00b or deep in debt right now, you might be thinking “how the heck can I save up thousands of dollars!?”. Well, that’s exactly what we’re going to help with in this post!

What is a basic emergency fund?

When we talk about emergency funds, we need to make an important distinction between the two types. While a fully funded emergency fund consists of enough cash to cover 3-6 months of expenses, a basic e-fund involves saving up $3,045 in liquid savings.

Why such a specific number?

It’s because economists have found that this specific amount of savings can help you to cover most minor financial emergencies.

Here’s a quick breakdown of some of the most common financial emergencies and what they could end up costing you:

| TYPE OF EMERGENCY | COST |

| Hospital ER Visit | ~$75 – 200 |

| Calling an Ambulance | ~$1,300 |

| Flat Tire | ~$20 – 100 |

| Minor Car Crash | ~$150 – $2,000 |

| Dead Battery | ~$45 – 250 |

| Broken Starter Motor | ~$150 – 1,100 |

| Calling a Tow Truck | ~$110 |

| Locksmith | ~$150-400 |

| Plumber | ~180-500 |

| Electrician | ~$150-550 |

As you can see, most emergencies can be covered with just a few hundred dollars in cash. But having a few thousand fully protects you from even more significant unpleasant surprises.

A 2024 Bankrate survey found that most Americans are unable to afford a $1,000 emergency. Which leads to many folks taking on debt!

BTW – eventually you’ll want a much bigger emergency fund. Like 3-6 months worth of living expenses. But, let’s not get ahead of ourselves. We’ll tackle that when we reach money gear #4!

When should you spend your emergency fund?

An emergency fund serves a very specific purpose. Money inside of this fund should ONLY be used for irregular, unpredictable expenses.

You may not be able to predict getting crushed by a falling grand piano, but you can plan for the new tires you’ll eventually need to put on your car.

For irregular expenses that you know are coming, but maybe don’t know when, use sinking funds! These are buckets of money you can set aside for expenses like annual car and home maintenance, holiday gifts, medical checkups, vacations, and more.

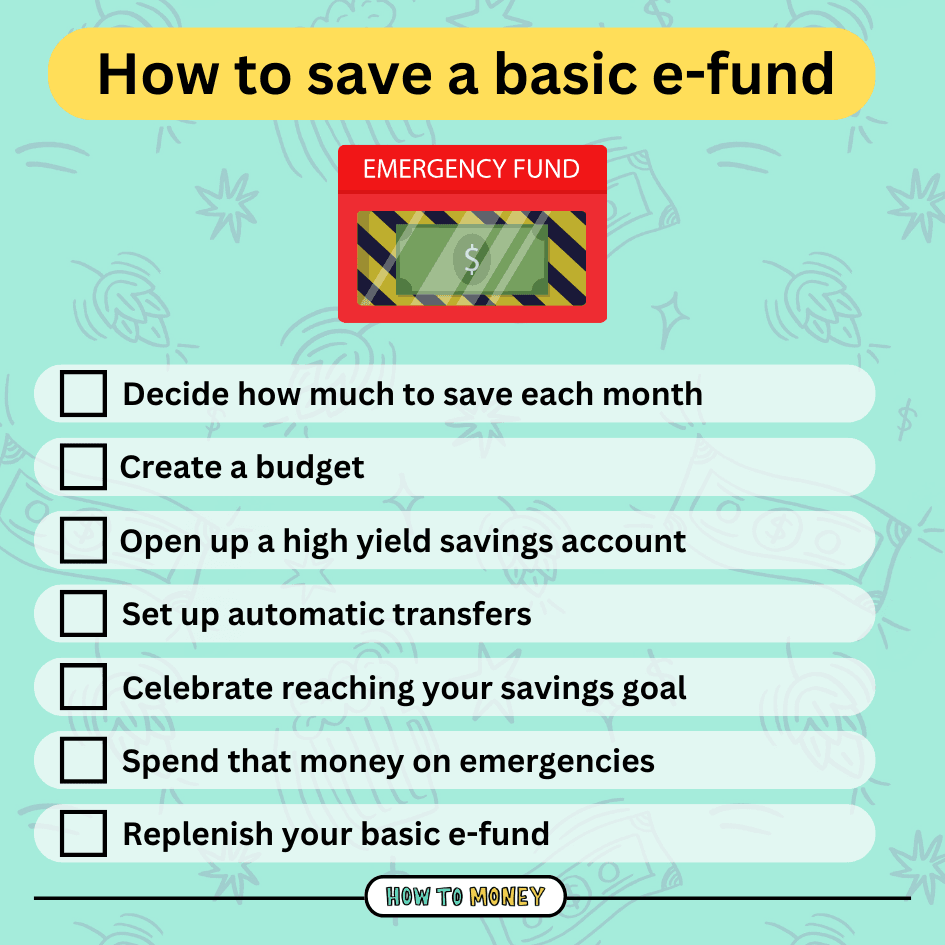

How to save up a basic emergency fund

It’s time to stop living paycheck to paycheck! You just need to set a goal, make a budget, and slowly build up that stash of savings.

Here’s a guide to help, with ideas on ways to cut back spending…

1. Decide how much to save each month

The first step in saving up your basic emergency fund is figuring out how much you want to put into it each month.

To help come up with a number, try thinking about when you want to achieve money gear 1 by, and divide $3,045 by the number of months.

For example, if you want to have a basic emergency fund within 1 year, you’d need to save about $253.75 per month.

It’s important to set a realistic savings goal. Don’t be afraid to start small. $20 saved is better than $0, and every dollar counts. Plus, slow and consistent savings builds a solid habit!

Remember, the idea here is to set yourself up for success in the long run. So plan to set aside an amount of money that you could realistically save every month, in good times and bad.

2. Make a simple budget

Making a budget is a crucial step in reaching all of the money gears. So if you don’t already have one, it’s important you create a budget now.

Don’t worry, budgeting is not nearly as hard or boring as you think it will be. Actually, it can be fun, quick and easy!

At the end of the day, it actually gives you the freedom to spend on the things you value, while helping you cut the spending categories that don’t bring you joy. A budget is just a plan for your money, and you get to make the rules.

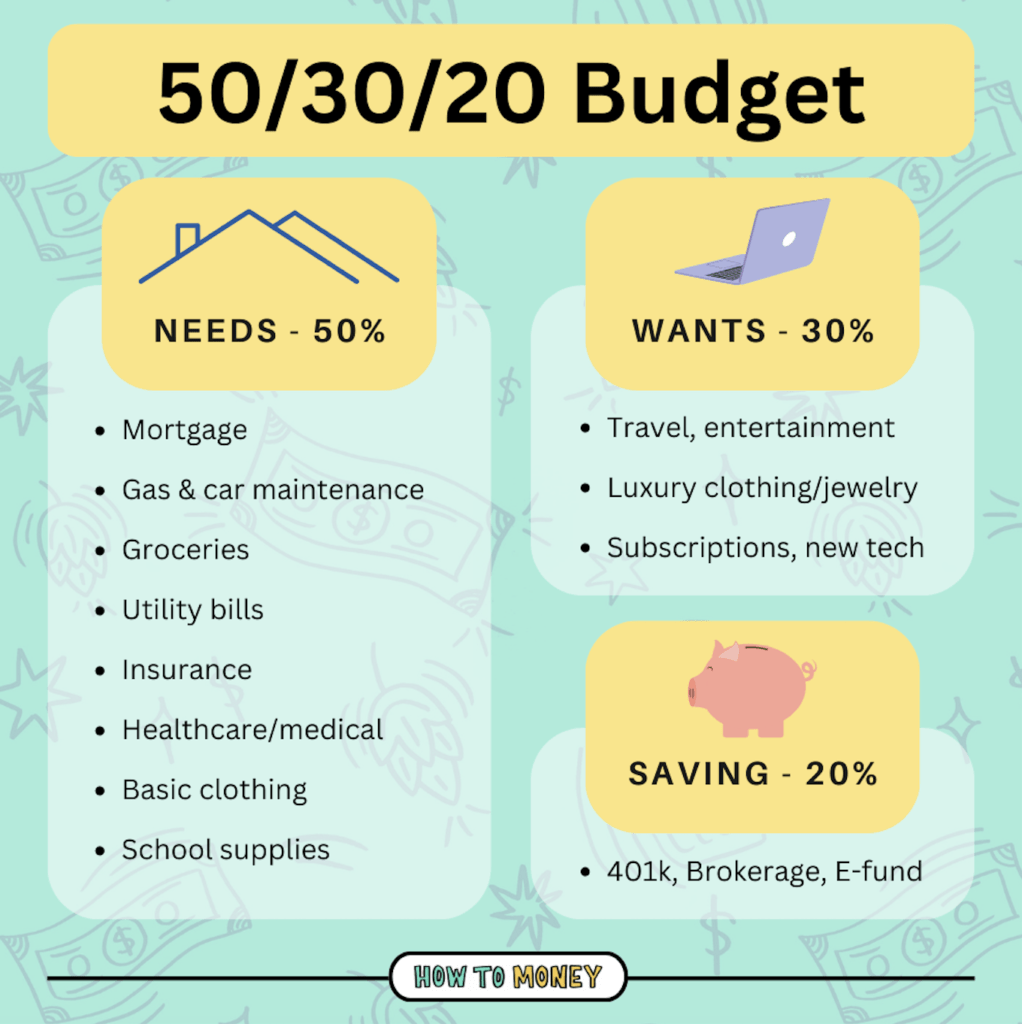

For beginners, we recommend the 50/30/20 budget.

After accounting for your expenses, you may or may not have money left over at the end of the month to put toward your emergency fund. Don’t worry!

If you’re coming up short on your goal, we’re going to share some tips on how to find more money within your budget to save later in this post.

3. Open Up a High Yield Savings Account

When you save up cash for your emergency fund, it’s important to make sure you save it in the right place. You don’t want to just stick your cash in just any old savings account…

Here’s the thing. Big banks (think: Chase, BOA, Wells Fargo) charge you heinous fees, require minimum balances, and pay you pennies in interest every year. That could delay your ability to amass this crucial e-fund! You and your savings deserve better.

A better place to stash your emergency fund is in a high-yield savings account. They’ll pay you much higher interest rates and are much more transparent with the fees they charge.

We recommend FDIC-insured online banks like CIT, Ally, or Discover.

Earning a higher amount in interest can help to keep inflation from eroding your savings so that your emergency fund can maintain its purchasing power over time.

4. Set Up Automatic Transfers

Financial automation is one of life’s greatest hacks for building wealth.

When your savings are on auto-pilot, you eliminate the roadblock of having to decide each month how much you will save. It’s just done automatically!

Start by setting up an automatic, reoccurring transfer from your checking account to your new High Yield Savings Account. You can do it monthly, or every 2 weeks to match your paycheck deposits!

Deducting that money immediately each month will keep you on track to hit your goal. Plus moving it to a separate account will make sure you don’t get tempted to spend it!

Once the transfers are put in place, just relax and be patient. Let the money build up, and you’ll reach your goal eventually!

5. Celebrate Your Accomplishment

Once you accumulate $3,045 in your high-yield savings account, you will have officially reached money gear 1! Woohoo! 🥳

But before you move on to money gear #2 and start chasing that 401k match, it’s important to take some time to reflect on your hard work and celebrate your accomplishment.

Now, I’m not suggesting you go blow all that money you just saved on a wild weekend in Vegas. But there’s nothing more exhausting than constantly moving the goalpost for yourself. You deserve a small splurge.

Whether you choose to celebrate with your favorite takeout and a movie or to simply take a day off of work to rest up, be sure to treat yourself on the cheap. Reward yourself for reaching this hard-to-accomplish goal.

6. Use Your Emergency Fund as Needed

When emergencies rear their ugly head, it’s your e-fund’s time to shine. Don’t be afraid to use it if you need to!

I know it can feel like a setback to clear out that cash after you worked so hard to save it. But remember: that it’s what it’s there for!

Instead of dwelling on the negative, try to be grateful that “past you” had the financial savvy to plan ahead for this. You’ve already proven that you can build up a nice savings reserve. You can do it again.

Stay away from borrowing money or putting expenses on your credit cards in case of emergency. That’s the absolute last resort.

7. Replenish your e-fund

If and when you do use your emergency funds to get out of a crappy situation, don’t forget to build them back up.

You don’t want your e-fund to stay underfunded for too long. Even if you’ve moved far past money gear 2 and are well on your way to becoming a millionaire, you never want to sit too long with no cash.

Put a pause on whatever other financial goals you have, and rebuild that basic emergency fund.

Hopefully by now, you’ve already developed a solid savings habit. So it’ll be way easier the second time around. You’ve done it once before and you can do it again.

Once you reach that $3,045 goal again, you can return to whatever money gear you were working on before. Rinse and repeat these steps every time you draw on your emergency fund!

Tips for saving up an e-fund more quickly

While the above steps are fairly straightforward, accomplishing them is often easier said than done. Especially if you don’t have a lot of margin every month.

So here are a few tips that can help you to free up more money in your monthly budget to fund your basic emergency fund!

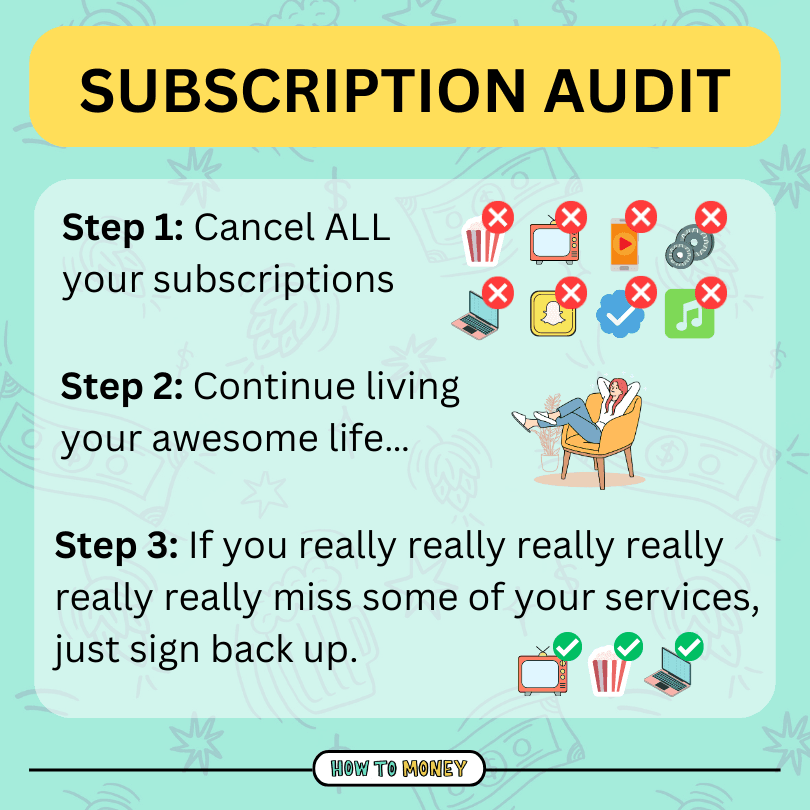

Perform a subscription audit

Not to be a nag, but most of us are spending way more on subscriptions than we might think. On average U.S. adults are spending around $91 per month on subscription services. That’s $1,092 per year! 🤯

It’s not that subscriptions are a bad thing. We love Netflix too!

But we do take issue with the fact that tons of Americans are paying for subscriptions they aren’t even getting value out of

So, we challenge you to cancel any subscriptions you aren’t regularly using. Remember, you can always re-subscribe. They won’t turn you away just because you canceled in the past!

Even if you halve your subscription payments, you’d save around $546 per year, more than 20% of your basic emergency fund!

Change Cell Phone Providers

Another thing you’re likely paying more than you need to is your cell phone plan. There are way cheaper plans out there you might not even know about!

What if I told you that you could cut your cell phone bill in half, all while using the same network and keeping your own phone?

MVNOs are phone companies that operate by leasing access to the network infrastructures owned by the big three wireless companies; AT&T, T-Mobile, and Verizon. This means that you can use the same networks, all while slashing your phone bill by a ton.

For example, switching T-Mobile’s “Unlimited Essentials Saver” plan to the Mint Mobile Unlimited Plan will save you at least $20 per month, or $240 per year.

US Mobile is another sneaky operator that can save you a boatload of money. They let you choose which network backbone you want to use!

Negotiate your bills

Most companies don’t reward you for being a loyal customer. Instead, they increase your bill each year and offer you the same (or worse!) service.

So try calling up companies like your insurance providers, cable companies, and utility providers and ask them if they have any introductory offers you can take advantage of. You’d be surprised at just how often they will be willing to offer you a discount to keep your business.

If the person you are speaking to is unable to accommodate your request, try asking to speak to the customer retention department. These are folks whose entire job is to convince you to stay, so you may have more luck with them.

When all else fails, don’t be afraid to switch companies! Shop around and see if better deals exist!

While switching providers sounds like a total pain, it’s never as bad as you might think. The savings will be well worth it.

Consider starting a side hustle

If you’re struggling to save money on your current income, it may be helpful to start side hustling!

A side hustle can help you earn more income, all while exploring your interests and hobbies!

When picking your side hustle, try to make sure it is something scalable, with room for long-term growth.

Gig work like driving for DoorDash or Uber can help you reach a short-term money goal. But a true well-fit side hustle can help you to massively increase your earning potential for the future.

Ask for a raise

Another way to earn more money and save more for your emergency fund is to consider asking your employer for a raise.

Yes, it’s scary. But it also works!!!

Getting comfortable asking for a raise is one of the most important ways to advocate for yourself financially. Even if they say ‘no’, you can rest well knowing you stood up for yourself.

Consider offering to take on more responsibilities around the office or working to improve your skills. Then, arrange a meeting with your boss to discuss your performance and compensation package.

Remember to always be polite and not to treat it like a battle. At the end of the day, it’s all about finding an arrangement that keeps both parties happy and ready to work!

Use your tax refund

Lastly, one of the best ways to bolster your emergency fund is to use your tax refund!

In 2024, the average tax refund was a whopping $2,850, which is almost what you need to fully fund your basic emergency fund.

While your return may be lower, any lump sum of money saved all at once can help to catapult you closer to your goal.

Tax refunds are not “free money” that can be spent on vacations and electronics. It’s your money. Save it for a rainy day instead – you’ll be so thankful you did.

The Bottom Line:

The very first financial step everyone should take is saving up a basic emergency fund. It protects you against life’s everyday emergencies, stopping you from accumulating debt or screwing up your other financial goals.

Plus, having cash on hand gives you more peace of mind in everyday life. No more living on the edge and feeling anxious about money all the time!

While saving your first few thousand dollars might seem intimidating, you can achieve it slowly but surely. Habits have a way of compounding, so focus on the simple action of squirreling money away from every paycheck. You will get there. Then, it’s time for Money Gear 2!

Related Posts: