Today’s question came in from Karl in Rosewell, New Mexico!…

“Hey, Matt and Joel. This is Carl, My wife and I are empty nesters living in Roswell, New Mexico.

In the past 4 years, our credit score has moved from a sub-600 to consistently over 750. Our credit cards are paid in full every month. We have two home loans for our new residents and our rental, plus a car loan from our credit union, and that’s the full extent of our outstanding debt.

Here’s my question. During the credit building phase of our life, we opened a lot of credit card accounts for about $150,000 worth of credit over 20 cards. Some of them have never even been used once.

We regularly use the Wells Fargo Active Cash for the 2% back and have earned over $5,500 in cash back there And the Chase Amazon Prime, which gives 5-6% back in Amazon credit when I shop on Amazon. I just opened 1 more with the only airline that flies out of Roswell.

Again, all of our cards are paid off in full every month. A couple of those cards have been closed recently due to inactivity, and others have sent notices threatening to do the same.

How hard should I work to keep those accounts open? I don’t need access to cash, but I don’t want to hurt my credit that I’ve worked so hard to build.”

The short answer:

You definitely won’t “trash” your credit score by closing a few credit cards. And even if there is a small negative impact, it should be a short-lived dip that you can recover from with time.

That being said, it might be best to test the waters by closing just a few select cards first. In slow fashion, not all at once.

Begin with the credit cards that have the smallest available credit lines and ones that have been opened the shortest amount of time.

Let’s get deeper into specifics and also talk about maximizing rewards too!…

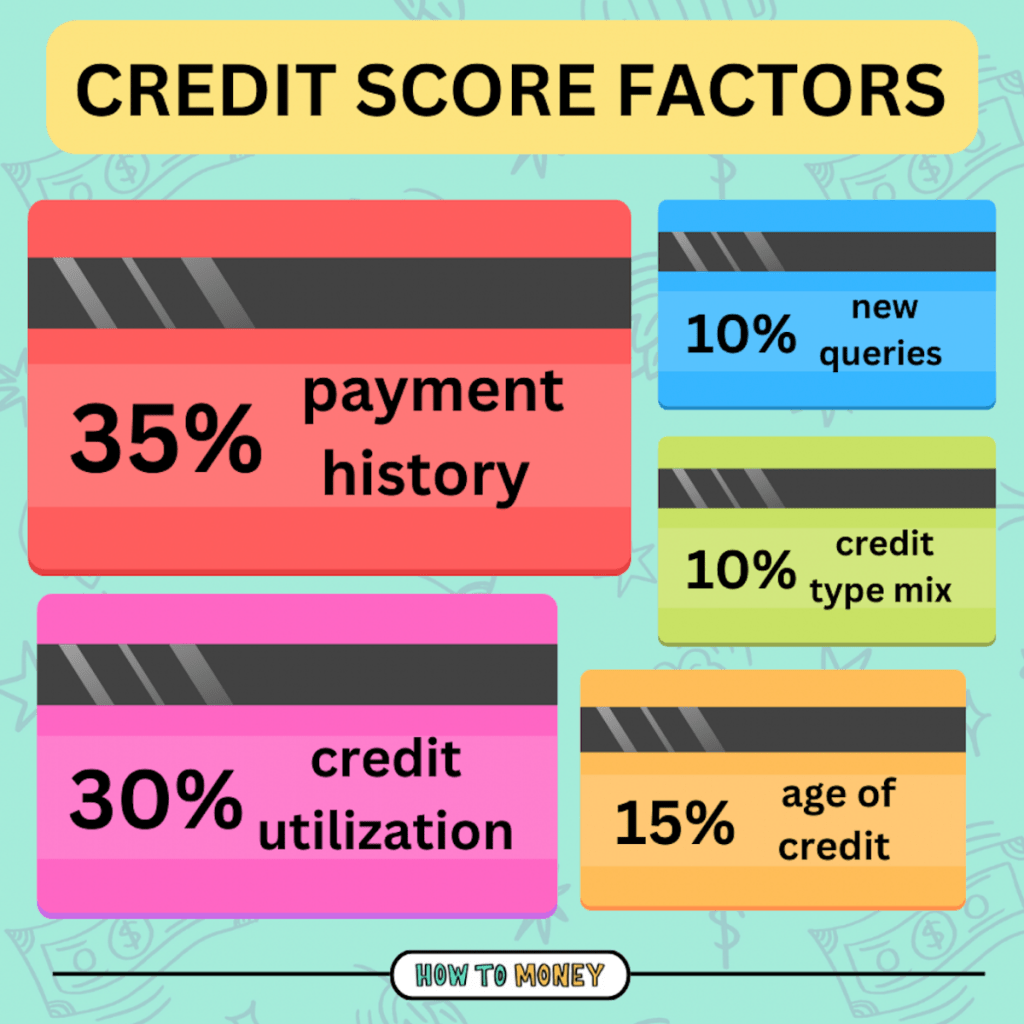

What factors make up your credit score?

By the way, congrats on boosting your credit score so much over the years, Karl!

Your story is proof that no matter how many credit lines you have open, it all comes down to responsible usage. Just paying that bill off every month shines bright and increases your score over time.

Here are the main factors that affect your credit score.

Payment history and credit utilization combined make up a whopping 65% of your score.

Age of credit, new credit queries, and type of loans make up the remaining 35%.

When you close a credit card, the two affected areas are age of credit and credit utilization.

If you close a credit card that has been open 20+ years, your overall age of credit might suffer. Similarly, if you close a card with a $40k available credit line (out of your total $150k), this will hurt your overall utilization ratio.

But, if you choose to close a few cards with smaller credit lines, that have only been opened a couple of years, the impact will be much smaller.

Will a small drop in credit score hurt you much?

Another thing worth mentioning… Will a small dip in your score actually change much in your financial life?

Some people live or die by their credit score and believe every single point is super important.

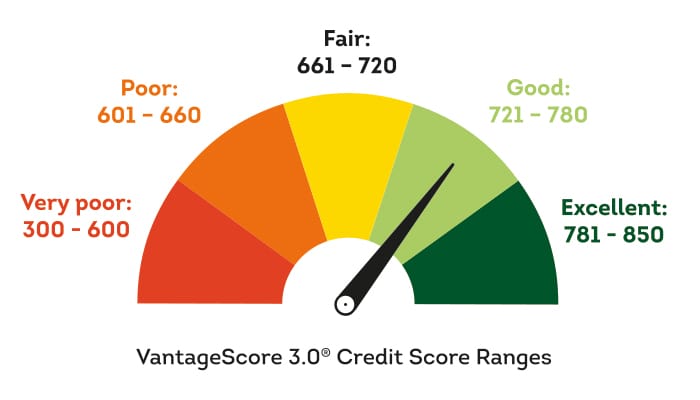

But the truth is, most creditors look at “ranges” when they assess your credit worthiness. 750 is the same as 775 in many cases. A 710 might be looked at the same as a 680 score because it’s in the same general range.

Here’s a chart from TransUnion showing the credit score ranges:

So ask yourself… If a couple of your accounts closed next month and your score dropped by 20 points, would that hamstring your ability to lease an apartment or get the best interest rate on a home loan?

The more likely you are to get an additional line of credit, the more important it is to play the game and keep those cards active in your credit mix.

Managing multiple credit cards

If you’re getting notices from a credit card company about potentially shutting down a card because you aren’t using it, you should probably just use it for something small to keep it active.

Our fave suggestion is for you to put one or two small recurring monthly bills on that credit card so that it has regular activity. Maybe your Netflix bill, or use that card only for gas purchases.

Make sure that the card gets paid automatically every month like the rest of them. You’ll want to use an app to track all your expenses and transactions across all cards, so nothing is forgotten.

If you have 10+ credit cards, you need a solid system in place. We wrote a great article about how to best manage multiple credit cards – check that out for sure.

Keep maximizing rewards

It sounds like you’re handling the top rewards categories well already. But you may want to revisit all the cards and cross-reference the benefits with your current spending.

Having a few credit cards at your disposal, if you use them properly, is a great thing. We advise all listeners to carry a handful of credit card options so they can get the best rewards for every purchase they make.

You’ve got the main bases covered already, Karl. A 2% cash back card for general spending, an Amazon card since you shop there regularly (no annual fee and 5% back on every purchase!) plus an airline-specific card for your flights.

Depending on where and how much you fly, you might want to look into a catch-all travel rewards card for you and your wife!

The Bottom Line:

If your credit score is super fragile and can’t take a momentary hit, it’s better to be safe than sorry. Instead of closing those credit cards, make some small purchases to keep those lines open instead.

But most likely, it wouldn’t be the end of the world if 1 or 2 of those credit cards got canceled. Especially if you get rid of a newer card with a relatively low credit line. You might not even notice much of a score drop.

Above all, consistent healthy usage is the key to building (and maintaining!) an excellent credit score. You can do this with 1 card, or 20 cards.

Good luck, Karl. Cheers for the great question!

For the full version of this discussion, check out Podcast Episode #799 (it’s the last question in the episode)

Related posts: