Unless you’ve been living in a cave for the past few years, you’ve no doubt noticed people freaking out about record-breaking rates of inflation. Or perhaps you’ve experienced the horror of going grocery shopping and seeing the prices of milk and eggs and thinking….what…the…?!

Costs of basic necessities like gas, food, airfare, utilities, healthcare, automobile repairs, rent, and clothing have soared putting a pinch on many people’s wallets. In fact, inflation (or the Consumer Price Index) recently reached levels that hadn’t been seen for nearly 40 years!

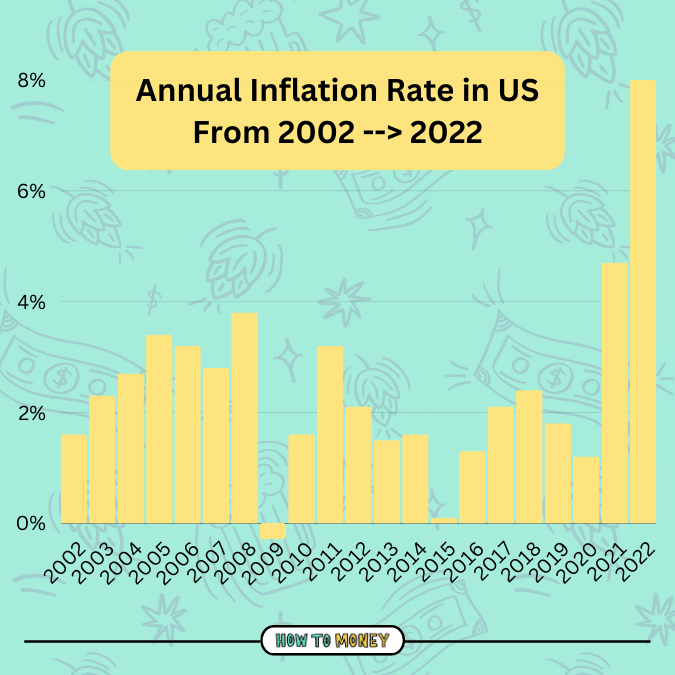

The aftermath of the COVID-19 pandemic in 2022 saw inflation hit 8.5%, its highest level since 1982. (In the late 70s and early 80s, inflation rates topped 10%.)

With inflationary price increases continuing to make the headlines, virtually everything is getting more expensive. In this article we’re going to discuss what’s happening with inflation and how it both hurts and helps your finances. Specifically, we’re going to address how to keep inflation from wrecking your finances.

What is inflation, exactly?

The technical definition on inflation is: a persistent, substantial rise in the general level of prices related to an increase in the volume of money and resulting in the loss of value of currency (opposed to deflation).

In plain english: inflation is essentially when prices go up. Or an even better definition is when the purchasing power of a currency goes down.

Common examples of basic inflation would be the cost of a postage stamp or a gallon of milk. Both of those items cost about 50% more now than they did in 1990. Ever hear your grandma talk about how she could get a candy bar for a nickel or how her house cost $20,000? (At which point you just want to say, “Don’t rub it in, Grandma!”) However, the one thing she conveniently fails to mention is that 77% of households in 1950 were earning less than $5,000 a year. That’s because inflation has been doing its thing behind the scenes every year. It has a substantial impact on both the prices of goods and services and wages too.

Important note: These numbers are national averages, based on all types of products and services. You personal inflation number may be very different. Here’s a great calculator to help determine your personal inflation number.

Long-term vs. short-term inflation

So…how long does it take for inflation to impact the purchasing power of your money? That depends on the rate of inflation. If inflation is 2% — roughly what we saw prior to the pandemic – that will cut the value of your money in half over the course of 35 years. If inflation hits 3%, your money gets cut in half after just 23 years. A 4% rate would see the value of your money halved in just 17 years!

That’s why hiding your hard-earned cash under your mattress or burying it in your backyard is a bad idea! If you take that route, inflation will likely cause more harm to your dollars than the bed bugs and earthworms.

As we’ve witnessed over the pandemic years, short-term or temporary inflation is a legit thing too. Remember when lumber prices blew up due to the pandemic supply chain issues which coincided with much higher demand? Or when egg prices ballooned for a few months? There is a meaningful difference between short-term inflation, which is small-term disruptions in prices for a particular good or service and long-term inflation. It can be difficult to discern in the moment though how much of an impact these short-term price spikes will have in the long-term.

Why inflation can be good

It’s true… inflation isn’t always a bad thing. In fact, the Federal Reserve (AKA: “The Fed”) wants inflation to happen, at least within reason. That’s partly because falling prices actually incentivize consumers to hold off on making purchases. Instead, they wait for prices to fall even further, which may harm the economy even more. A small amount of inflation encourages consumption which helps the American economy keep humming along.

However, problems start happening when inflation ramps up and spirals out of control. It’s similar to a surge of electricity to your household electronics. That’s when things get fried and don’t work like they’re supposed to.

Government spending

A once-in-a-lifetime global pandemic saw governments around the world turn on the spending spigot in a way that had never been done before. Trillions of dollars in government spending occurred in an effort to combat the harmful economic effects of COVID-19.

We’ve never experienced government spending like this before in history! Stimmy checks and stay-at-home orders led to flush bank accounts. That combination created an economy where too many dollars were chasing too few goods, leading to the inflation spike.

NPR put the massive spending into perspective. They explained that, “If that amount of money alone were the GDP of a nation, that nation would have the fourth or fifth largest economy in the world this past year.”

Good interest rates for HYSA

Inflation is more than just rising prices for goods and services. It is also the gradual depreciation of the dollar. Cash under your mattress is almost like a burden because it loses value month after month if it is not used.

The solution is to put your cash into interest earning accounts. Specifically, we’re talking about a high-yield saving account, or HYSA. As of this writing, there are accounts that are paying out over 5% interest! That’s a massive positive change for savers.

High inflation means It’s time to switch banks and relocate your money to an institution that is competing for your business. Savings accounts at internet banks such as CIT, Ally, and Discover provide vastly higher interest rates than traditional banks you see on every corner as you drive around town.

Another benefit of moving all your cash out of reach into a HYSA is that it’ll stop you from dipping into your savings account. Having that money out of reach gives you less temptation to spend it!

Cheaper technology

Despite the fact that this inflationary reality continues to linger, that doesn’t mean everything will cost more. For instance, computers and TVs continue to go down in price – costing much less than they did 20 years ago.

In fact, you’ve got a pretty inexpensive supercomputer in your pocket right now. You know, the one that also makes phone calls that you probably don’t use it for. Actually that smartphone replaces a bunch of gadgets you used to own like a flashlight, calculator, iPod, video/still camera, and more. So even though inflation marches continually higher over the years, technological progress does stem the tide in some ways.

Wages inflate, too!

Without a doubt, inflation affects wages too. You know that laughable, 1% to 3% cost-of-living increase you get from your employer? Pre-COVID, when inflation rates were so low, that microscopic raise was actually enough for your pay to slightly outpace the price increases of most goods and services each year.

While your pay would ideally outpace inflation, that cost-of-living increase is important. And since 1950, prices are up around 1,000% but median household income is up closer to 2,500%.

Although wage increases and technological progress are things that seem to affect us more directly than what the government does, they aren’t things that we have direct control over.

What can you do about inflation?

Sadly, we can’t predict the future and just wait until inflation cools. Here are some safeguards you can do here and now to ensure your money is in good shape.

- Invest more — The main reason to start investing is to build wealth. But before that, the first goal of investing is to beat inflation and to avoid seeing our wealth get destroyed through inactivity. Don’t neglect your workplace retirement account and/or IRA.

- Housing — can also be a good hedge against inflation. Primary residences are the No. 1 financial asset that most Americans have. The rising values of homes have beat out inflation and since the 1960s homes have risen an average of 4% annually. Also, low-interest rate debt like having a 30-year fixed mortgage in the 3% range can actually be beneficial when inflation is high. You might want to reconsider paying extra to pay off your mortgage early when you can earn more in a straight-up savings account.

- Prioritize eliminating high-interest rate debt – especially debt that comes with variable interest rates. As inflation has persisted, it has most likely affected the interest rate you’re paying on debts like credit cards and HELOCs. It’s a good idea to focus even more on getting those paid down quickly.

- Get on a budget and adapt it accordingly – If you’re trying to live on the same budget numbers from 2011, I bet you’re having a tough time. You need a budget. But you also need to update it as prices shift. We’re not talking small changes on a monthly basis. Double check your budget once or twice a year to make sure that you can still get by on that gas or grocery amount you’ve allotted.

Here are several more tips and strategies to battle back against inflation.

The Bottom Line:

Over the past few years, inflation has caught everyone’s attention, and for good reason. We are all witnessing increased prices everywhere we look and it’s difficult to know how to respond.

However, it’s important to know that it’s possible to combat the effects of inflation in your own life. Taking some proactive steps now will allow you to weather the impact of rising costs. Prices are always on the rise, but so is innovation.

All in all, don’t freak out too much about inflation prognostications, but do be prepared. It’s critical to focus on the things we can control. While none of us can affect the overall rate of inflation, our personal choices are the most influential determinants in how much we spend for products and services.

Related posts:

Beer from episode…

While chatting about the benefits of inflation, we enjoyed a Be Easy Citra by Monday Night Brewing! And please help us to spread the word by letting friends and family know about How to Money! Hit the share button, subscribe if you’re not already a regular listener. And give us a quick review in Apple Podcasts or wherever you get your podcasts. Help us to change the conversation around personal finance and get more people doing smart things with their money!

Best friends out!

By the way, from a boomer, the AI unit called HAL, the name was picked because they are the letters just in front of IBM.