Do you live in a high-cost-of-living area where the rent is out of control and the average property values make you feel sick? (Me too 🙋♂️). How can you ever afford to buy a house when every local listing on Zillow is 7 figures, even for crappy run-down shacks!?

One avenue you might want to research is rentvesting.

Rentvesting is essentially renting where you live, while investing in property elsewhere. It can let you enter the real estate market at a cheaper price point, while continuing to live where you love.

This isn’t a new concept by the way – people have been rentvesting for decades. But it’s gaining more traction recently with younger folks who are savvy with rent vs. buy math.

Personally, I’ve been rentvesting for over a decade. In this post I’ll share some of my personal experiences buying and owning rental properties, and give you the lowdown on the pros and cons of the rentvesting strategy. Let’s do it! 🏡✨

What is Rentvesting?

Picture this: Instead of owning a single expensive home that you live in, why not own 2-3 inexpensive homes that other people live in?

Depending on where you buy, the incoming rent from those investment properties could fully cover (or more) the cost of renting an awesome home for yourself in a more expensive city!!

There’s no rule that says your first home purchase needs to be your primary residence. In an ideal world every American would have a fair opportunity to own the home they live in and put down roots locally. But sadly that’s not in the cards for a decent chunk of folks these days. Prices seem to be getting more out of whack every day.

Simply put, rentvesting is choosing to be both a renter and an owner. Rent wherever you want to live. Own where it’s a good investment.

Why Rentvesting is Awesome:

Rentvesting lets you have all the benefits of being a renter, as well as most of the upsides of home ownership.

Here’s a handful of reasons rentvesting can be a smart move for younger folks…

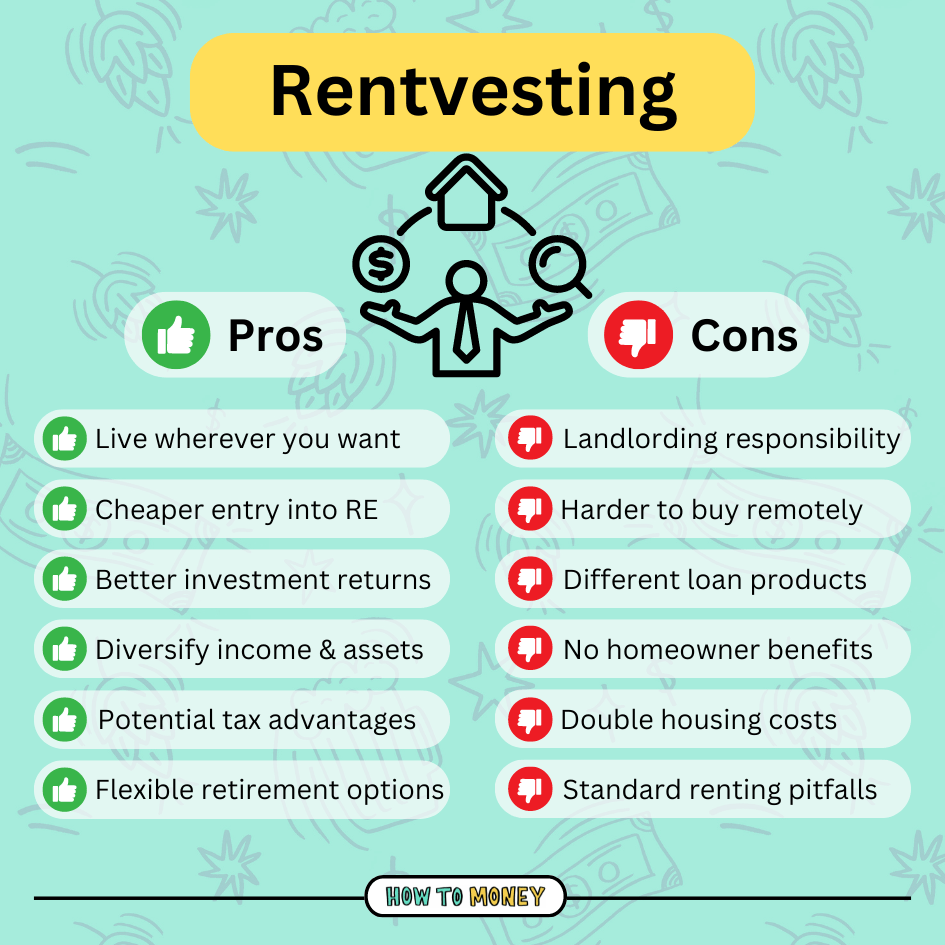

1. Live wherever you want

As a renter, you’re not tied down to any specific location. Nor are you “boxed out” from any city because of ridiculous property values.

Rentvesting lets you live wherever you choose. And you can even move at the drop of a hat because you’re not physically tied down to a specific house.

Personally, I live in a fancy part of Los Angeles. And before that I lived in Hawaii for 5 years. My wife and I love the beach and always want to be near the ocean.

But buying a home in West LA is not a financial reality for us – or in any fancy beach town for that matter. The homes on my street are $2-3 million and I don’t have that kind of cash to throw around!

Renting is our best option to live where we love. Yes, the rent isn’t cheap here. But it’s nowhere near what we’d be forking over to actually buy a place.

2. Easier entry into the property market

To buy an $800k home right now you’ll need about $160k in cash, as well as a minimum salary of ~$150,000/y just to qualify for the mortgage.

Those stakes are pretty high!

The downpayment alone could take over a decade to save up. And I don’t know about you, but being mortgaged up to my eyeballs doesn’t sound like fun.

What if I told you that you can buy a beautiful, small duplex in a cute Texas town for only $300,000? That’s a much easier investment to tackle.

Smaller properties can be stepping stones to bigger, more expensive properties.

3. Potential for better investment returns

Primary residences are usually sub-par investments. Especially in pricey, urban markets.

But rental properties in more affordable areas can be very lucrative. What they may lack in long term appreciation, they more than make up for in higher monthly cash flow.

For example, a $1M property in Austin metro might demand $4,000 per month in rent.

But a couple hours outside of Austin, you could own 3 x $300k properties that bring in $8,000 per month in rent collectively. That’s a substantial difference in monthly income!

Rentvesting works best when you own properties in areas with a low buy-to-rent ratio.

4. Diversified income and assets

A common problem we have in the US is that many Americans are “house poor”. Their life savings are tied up in home equity, and they get stuck at their 9-5 job to be able to afford the monthly payment.

Rentvesting shakes up that traditional model.

By owning rental properties, you’re creating separate income streams. You’re also spreading your investments into several smaller buckets vs. all tied up in a single asset.

5. Potential tax benefits

I want to stress the word potential here… Because everyone’s income, state laws, and tax situation will vary a little.

That being said, owning investment real estate comes with a handful of tax benefits that regular homeowners don’t get.

For one thing, operating expenses are tax deductible. Things like home maintenance, insurance, mortgage interest, and anything associated with running the rental business can be deducted against the property income.

Depreciation is another tax deduction you can claim for investment properties. Although it will be recaptured when the property is sold.

Challenges and downsides

Before you run out and make offers on some cheap properties in a far-off state, you should know that rentvesting is not everybody’s cup of tea!

Here are a few things that complicate the rentvesting strategy…

1. Landlording responsibilities

Managing tenants requires a unique set of skills. It’s not terribly hard, but it’s not a cakewalk either!

There’s a big learning curve when it comes to finding great tenants and managing them well. Anyone thinking about rentvesting needs to seriously evaluate whether they’re up for the challenge. Becoming a remote landlord can be like a part-time job!

Hiring a property manager is always an option. But, that comes with added costs which takes a chunk out of your profits.

2. The buying process can be harder

Since rentvesting means buying in a different location than where you live, it can be challenging to find, evaluate, and close on the right property.

Whether your desired investment area is just a couple of hours away or on the other side of the country, it’s harder when you are farther away. You need to build a team of local people you can trust to find the right property.

Remember, you’re buying as an investor, not an owner occupant. So the criteria for choosing a profitable property is a little different than shopping for a dream home you would personally want to live in.

3. Investment loans vs. home loans

If you’re buying a home to live in, chances are you’ll qualify for some awesome new homeowner loan products. You’ll get reasonably low rates, an array of down payment options, etc.

But if you’re not planning to occupy the house you buy, getting a loan can be a little trickier.

It might require a minimum 20% down payment. Some banks might also tack on an extra .5% or 1% to the mortgage rate just because it’s an “investment property”.

4. Forfeit some tax benefits

A huge advantage for people who sell their primary residences is avoiding some (or all) capital gains tax when it comes time to sell the house.

Here is the exact IRS rule. But in general, you can exclude up to $250,000 of appreciation gains from your income, or up to $500,000 of that gain if you file a joint return with your spouse.

But if you’re rentvesting and don’t live in the house you are selling for at least a 2 year stretch in the past 5 years, you’ll have to foot the entire capital gains tax bill upon selling.

Another tax benefit you might forfeit is any first-time home buyer credits. These are only available to people who move into the home they are buying.

5. Two sets of housing costs

When you’re rentvesting, you are kind of responsible for double housing costs.

As a renter, you’ve obviously gotta pay rent, utilities, etc.

As an owner, you’re also on the hook for the mortgage, taxes, insurance, etc.

Yes, you will get incoming rent from that second place to offset some costs. But the fact remains you’re still responsible for both sets of costs and need to budget accordingly. Set extra savings aside and plan for potential vacancies!

6. Renting pitfalls

While renting has a ton of flexibility, it can sometimes backfire if you are forced to move or have a terrible landlord.

For anyone who wants complete control of where they live, owning the house is better. Renters can’t make desired renovations or share in the profits of house appreciation.

Emotional aspects of rentvesting

There’s something to be said about the “pride” of homeownership.

People who own their homes tend to feel proud to have a tangible asset they get to touch and feel every day. Owning a little slice of the community can be incredibly rewarding!

But as a renter, sadly, your housing choice might be frowned upon. It’s silly, but for some reason there’s a stigma associated with renting – just tell your Boomer grandparents that you are planning to rent forever, and watch the disappointment in their face.

However, as a rentvestor, you can still feel that pride of ownership. It’s just a different mindset.

Personally, I own more real estate in this country than most of my neighbors do. Even though they own their homes and I rent mine, I sleep quite well at night knowing I am building wealth through real estate. It’s just not via the traditional path.

Tips for Successful Rentvesting

Now that you’ve got an understanding of what rentvesting is and the good/bad/ugly, here’s a few extra things to consider if you’re hoping to pursue this strategy…

1. Assess your financial situation, honestly

No matter the property location or value, if you’re not financially ready to buy, don’t do it!

There’s no rush to enter the real estate market. Better to take your time and do it right than start writing checks your ego can’t cash. (I’ve always wanted to write that in a blog post. Yay!)

Start by assessing your budget and savings pile. Figure out how much you can comfortably allocate for a down payment, and make sure you have plenty of cash reserves.

Having a solid understanding of your monthly expenses is key, as well as the new ones you’ll be responsible for is crucial. The goal is to become a cash flow and budgeting expert, before you buy a place.

2. Choosing good investment properties!

The whole point of rentvesting is to own properties that are more profitable investments than the house that you are living in.

Rental properties are about math. Not picking cute or pretty houses with adorable curb appeal.

Successful real estate investors do TONS of research and take a very conservative approach when buying. They manage rentals like a business, and try to remain unemotional when making decisions.

Here’s our beginner guide on buying your first rental property. It only scratches the surface, but it’s a good place to start.

3. Be patient and stay the course

After you buy a rental property, it takes a while to “stabilize”. You’ll learn a million new things as a first time landlord, which can be overwhelming.

But eventually, things settle into a rhythm. And the more time that passes, the more compounding you are able to experience.

So don’t throw in the towel too early and abandon everything when you hit some turbulence. Patience pays off when it comes to rentvesting!

4. Scale if you can!

If things are going great, why not double-down and buy more properties!?

With more experience under your belt, chances are you will get better at finding good deals, managing people more effectively, etc. Hopefully as you scale, you’ll get better and better.

5. Figure out your “end-game”

Rentvesting is a great way for younger folks to enter the property market. They can buy houses based on their budget, not the location they live in.

But it might not be a good forever strategy. When you’ve found a place you want to live in for the rest of your life, it could be time to buy a house there.

If that’s the case, it’s a good idea to set some clear goals for your rentvesting strategy.

For example, maybe you want to buy 1 rental property every 5 years until you have 5 properties. At that point, the goal could be to sell 3 properties, using the equity to purchase a home locally to live in. The other 2 rentals can be kept as investment properties.

It’s ok if your game plan changes over time (mine has a lot!). But starting with the end in mind will help you make the right decisions on the front end and avoid distractions.

Is rentvesting right for you?

Here’s a quick summary again of the pros and cons of rentvesting.

Remember, you get all the pros (and cons) of renting. But you also get all the pros (and cons) of being a property owner.

If you or your partner is absolutely gung-ho on the American dream of owning a primary home, rentvesting might not be a good fit. Keep saving up that downpayment, and search for a place that fits your lifestyle and budget.

But if you’re a long way away from settling down, or have no desire to own a home, rentvesting might make sense. Mathematically, it could work out in your favor!

Alternatives to rentvesting

Like I mentioned earlier, rentvesting isn’t for everyone. There are many ways to build wealth – and some don’t involve buying real estate at all!

- House hacking: This strategy involves buying a place to live in, and renting out a portion of it. Like a duplex – living in one unit and renting out the other! Here’s a full guide on house hacking.

- Buy with a friend: If you can’t afford to buy a house, you could potentially split costs with a friend or family member. Careful though, this can be a tricky relationship to navigate!

- Index and chill: You can grow a huge amount of wealth without even investing in real estate at all! As long as you invest regularly (in something like index funds) you can grow a mammoth nest egg that can provide enough cash flow to cover your rent, forever.

There’s no cookie cutter solution that fits everyone’s lifestyle. You gotta select the path that suits you best!

The Bottom Line:

In a nutshell, rentvesting offers a fantastic opportunity for young people living in high-cost areas to break into the real estate market without sacrificing their lifestyle. You can continue to get all the benefits as a renter, while also achieving potentially higher investment returns as a property owner. It’s can be the best of both worlds.

So stop scrolling Zillow and freaking out about “missing the chance” to buy your dream home. Rentvesting could be the perfect solution. Detach your personal life from your investments, by renting that dream home and buying investment real estate elsewhere.

Happy rentvesting! 🏡✨

Related posts: