Good morning, and happy Tuesday!

Guess what?!… Today’s newsletter is #26, which means we’ve just crossed the half-year milestone of sending these weekly emails! 🥳

They say “when you’re doing something you love, you never work a day in your life”… And we are lucky enough to be experiencing this first hand.

It’s **because of YOU** that we are so blessed at work… So thank you, sincerely, for reading and listening to our stuff. We love you.

OK, enough with the mushy crap, let’s talk about money!! 👇👇👇

TO DO

Make sure your investments –> are invested! 🤦♀️

Last week we learned that around 35% of people’s HSA accounts are sitting in “core positions” a.k.a cash. This money is earning nothing, losing value to inflation, and forfeiting tax advantages for growth!

Same with other investment accounts… sometimes people transfer money into them, but then forget to buy index funds afterwards. Or some folks forget to re-invest dividends and cash starts to pile up in their portfolio without them realizing.

So today: Log into your investment accounts, and if you see money sitting in “Core Position”, “FDIC Money Market”, “SPAXX” or “Cash”… consider moving it into an actual investment, like a total stock market fund or an S&P 500 where the money is working for you. 💪

Related: Saving vs. Investing — Know the difference!

CHARITY

Do your givin’, while you’re a-livin’!

You may have read a few weeks ago that Patagonia’s founder, Yvon Chouinard, just gave away his entire company (worth ~$3 Billion) to charity to continue fighting climate change.

Yvon said, “Hopefully this will influence a new form of capitalism that doesn’t end up with a few rich people and a bunch of poor people”.

What a legend! 🤩

Here are a few other inspiring millionaire/billionaire giving stories:

- Percy Ross spent ~20 years giving away his $30 million fortune to readers of his newspaper column called Thanks a Million. After giving everything away, he said “In many respects, I’m far richer today than when I started.”

- Retail giant Chuck Feeney gave away his entire $8 billion fortune over the past few decades. He finally went “broke” in 2020, saying, “to those wondering about Giving While Living: Try it, you’ll like it.”

- Warren Buffett’s Giving Pledge now has 236 signatures from billionaires, all pledging to give away the bulk of their fortunes *before* they die. Buffett said “The way I got the message out was to get a copy of FORBES, look down that 400 list and start making phone calls! Bill and Melinda did the same thing. So keep publishing the list so I can milk it” 🤣

Billionaires aside, we encourage everyone to include some type of charity in their budget (even if it’s a tiny amount).

A big component of growing wealth is having the right attitude towards money, and not just looking to satisfy your own desires, but trying to help the needs of others as well.

Giving is such an important practice to begin implementing ASAP. It’s not a principle or stage of enlightenment that you reach “someday”. Rather it’s like working out- the earlier in life you get started, the better off you’re going to be in the long run.

More resources:

- 🎙 Podcast Ep 281: Giving Away Your Money Will Make You Richer (46 mins — we talk about vetting charities, different reasons we give our money away)

- 👨💻 Great Blog Post: How to include charity in your budget (5 min read)

- 📚 Yvon Chouinard’s Book: Let My People Go Surfing (A very inspirational read! It’s a mix between personal autobiography and how he built Patagonia from the back of his surf van all the way to becoming one of the most environmentally responsible companies on earth)

TOGETHER WITH CARDRATINGS

Big news- The HTM Credit Card Tool is live!

One of the most common personal finance questions is —> What’s the best credit card for me?

So to help answer that we’ve partnered with CardRatings and have just launched an awesome new credit card search tool! (It looks like the screen shot above)

Here’s how it works: you start by clicking all your rewards preferences, like whether you prefer airline miles, cashback or whatnot… Then the credit card tool will search all current cards and promotions out there and filter the ones that meet your criteria.

All the results are shown in an easy to compare list, highlighting the main features and terms. Finding the best credit card for you just got easier!

Check out the HTM Credit Card Tool– let us know what you think!

SAVING

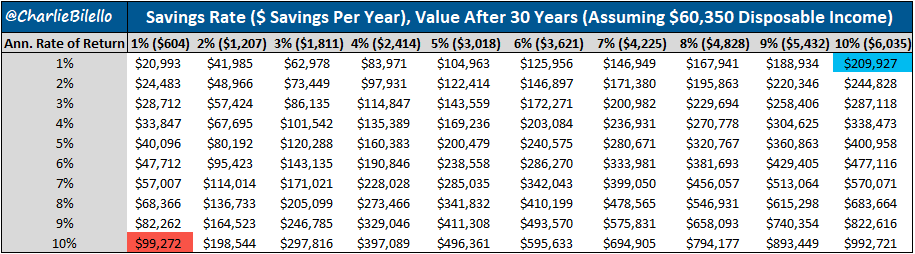

Pop quiz: Saving vs. investing…

Question… Who do you think has MORE money after 30 years…? 👇

a) someone who saves 1% of their income, and earns a 10% return

b) someone who saves 10% of their income, and earns a 1% return

c) someone who saves 5% of their income, and earns a 5% return

Without a calculator, most people would guess person a), because we’re mostly fixated on earning high ROIs to grow money faster…

But the correct answer is actually b). A person’s savings rate means more than investment returns! The more you save initially, the more you have later – even with lower compounding returns.

Here’s the chart data, via Compound Advisors 👇👇👇

(this assumes an investor is starting with $0, and saving on a set schedule for 30 years)

A few conclusions:

- Most people should stop chasing high investment returns and focus on saving more of their paycheck. (the avg US savings rate right now is 3.5% 😥)

- Savings is even more impactful in low/negative return years (pssst. we are in one of those negative years right now! 🎉)

- Good news: How much we save is something that is IN OUR control (vs. we can’t control investment returns exactly).

Soooooo… perhaps it’s time to re-evaluate your savings rate and see if you can squirrel away a lil bit more?

Related stuff:

- 💻 WalletHacks: 105 Easy Ways to Save Money (broken down by different spending categories)

- 🎙 Podcast Ep 163: Saving vs Investing (37 mins)

- 📝 HTM Blog: Why most people lose money in the stock market

- 🔢 Spreadsheet Calc: For all you nerds who want to play around with investment vs saving numbers, here’s a calculator we replicated from compound advisors. (click File –> Make a copy to edit the sheet)

ICYMI

Word on the street…

House Prices 📍

Via realtor.com, here are the top 10 cities where home prices have dropped the most since June. Spoiler alert: Austin, Phoenix, Palm Bay, Charleston & Ogden have the highest declines in median listing price, ranging from negative 8-10%. (Psst. We still believe a house isn’t the *best* investment out there for most people!)

Debt Relief 👩🎓

The federal student loan debt relief application is now LIVE! Head on over and fill out the form if you qualify.

Social Security COLA ⬆️

Due to another hot inflation report last month, it’s official now that anyone receiving Social Security benefits will have a COLA (cost of living adjustment) increase of 8.7%, starting next year! This is the biggest increase since 1981.

Winter is coming 🔌

And our electric bills are going to be higher this year 😭… A new US Energy forecast shows we should all expect an increase in energy bills averaging 6-7% more than last year. This is due to global fuel issues and a colder winter predicted for 2022-23. 🥶

GM Energy 🚘

Last week General Motors announced it will launch a new business line, making and selling energy products like solar panels, home batteries, and energy storage products for homes and small businesses. Kind of like what Tesla started — back in 2015! (better late than never, ey? 🤷♂️)

Financial Abuse 🚫

October is Domestic Violence Awareness month! And reports show that 99% of domestic violence survivors also experienced some type of financial abuse. Here’s a great article explaining what financial abuse is, examples, and how to escape it. If you are in trouble or being abused, please call for help, you are not alone!! 800-799-7233.

HOW *YOU* MONEY

Cody, 36y/o from Raleigh, NC ⛱

Occupation: Product Analyst

Salary: $85,000 /year

Paycheck deductions: -$2,700/month (Taxes, health ins, 401k, HSA)

Rent: -$1,365/m (+$280 for all utilities)

Other debts: -$46k student loans, payments on pause!

Living expenses: ~1,650/month

Leftover savings each month: ~$1,300 per month!!

How are you investing your excess savings each month?

- I put $500 a month into a savings account so when January 1st rolls around I max out my Roth IRA at the beginning of the year.

- I put $200 into a travel fund so I always have some money to pay for planned and impromptu travel throughout the year.

- I put $600 into a buy a rental property fund with a goal of reaching $75,000.

Biggest “craft beer equivalent” splurge:

Coffee and lattes, tiki drinks, travel and new experiences. I’m also a fiend when it comes to backpacks. I have to try really hard to not fall victim to those sweet Boundary Supply and Wandrd bag ads.

Best savings hack/advice:

Set up a conscious spending plan to see how much money you have left after expenses and debt payments (I made one you can copy and use), then set up automated deposits to goals that are most important to ensure your money is working for you. I use Betterment for checking, savings, and investment accounts. It lets me set up as many goals and automated deposits as I want. This way I can see and manage all my auto deposits in one service.

Anything else you want to share?

Read “I Will Teach You to Be Rich” by Ramit Sethi. He was on a How To Money podcast a few years ago, go listen to it. That’s who inspired me to build a conscious spending plan, which showed me where I could adjust spending to make sure I could max out my Roth IRA. I’m now on year 3 in a row of maxing out my Roth. I wish I had read his book way sooner!

Recent money win, and how did you celebrate?

I booked my trip to Peru using credit card points for all flights, except for one $65 Southwest ticket since Southwest doesn’t federate with other airline booking systems. I’m going to celebrate by eating all the food and going on all the adventures when I get there!

What’s your biggest money challenge right now?

Having more savings goals than I have disposable income. My vehicle is 19 years old and nearing 220k miles. I expect in the next 4 or 5 years I’ll need to replace it and I’d like to get a sweet electric SUV (I’m thinking Rivian), which means spending at least $70k. Any money I have left over after satisfying my automated savings goals I put into my New SUV fund.

**We share these money profiles because some of the best money hacks and advice comes from YOU, the community… If you’re up for being featured, we’d love to hear from you –> fill out the How You Money form here (we only post once you give permission!!)**

Have a great week y’all!

Best friends out 🍻

*****

* Advertiser Disclosure: How to Money has partnered with CardRatings for our coverage of credit card products. How to Money and CardRatings may receive a commission from card issuers.

* User Generated Content Disclosure: Responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.