The end is near. At least for most Americans. That’s because the money sins that people commit en masse are leading to desperate money situations. And we need a mass conversion experience – worthy of a Billy Graham stadium sermon – when it comes to how Americans handle their money.

The end is near. At least for most Americans. That’s because the money sins that people commit en masse are leading to desperate money situations. And we need a mass conversion experience – worthy of a Billy Graham stadium sermon – when it comes to how Americans handle their money.

Here are the worst money sins you can commit. Avoid these and you can be one of the enlightened few (visualize a green halo above your head) that will be well prepared monetarily for the future – no matter what comes.

Having a car note

This is a great money sin for which there is no absolution aside from paying it off and never doing it again. Americans are taking out car loans like one might take candy from a baby. They are taking out longer term loans than ever before as well which only compounds the problem. The effect this creates is that when you get tired of your ride, you are likely upside down in it. That means an even worse car loan situation when you eventually trade that car in for an upgrade. This is a sick and debilitating cycle. Don’t take out car loans. There are no circumstances that make it ok.

Not saving for retirement

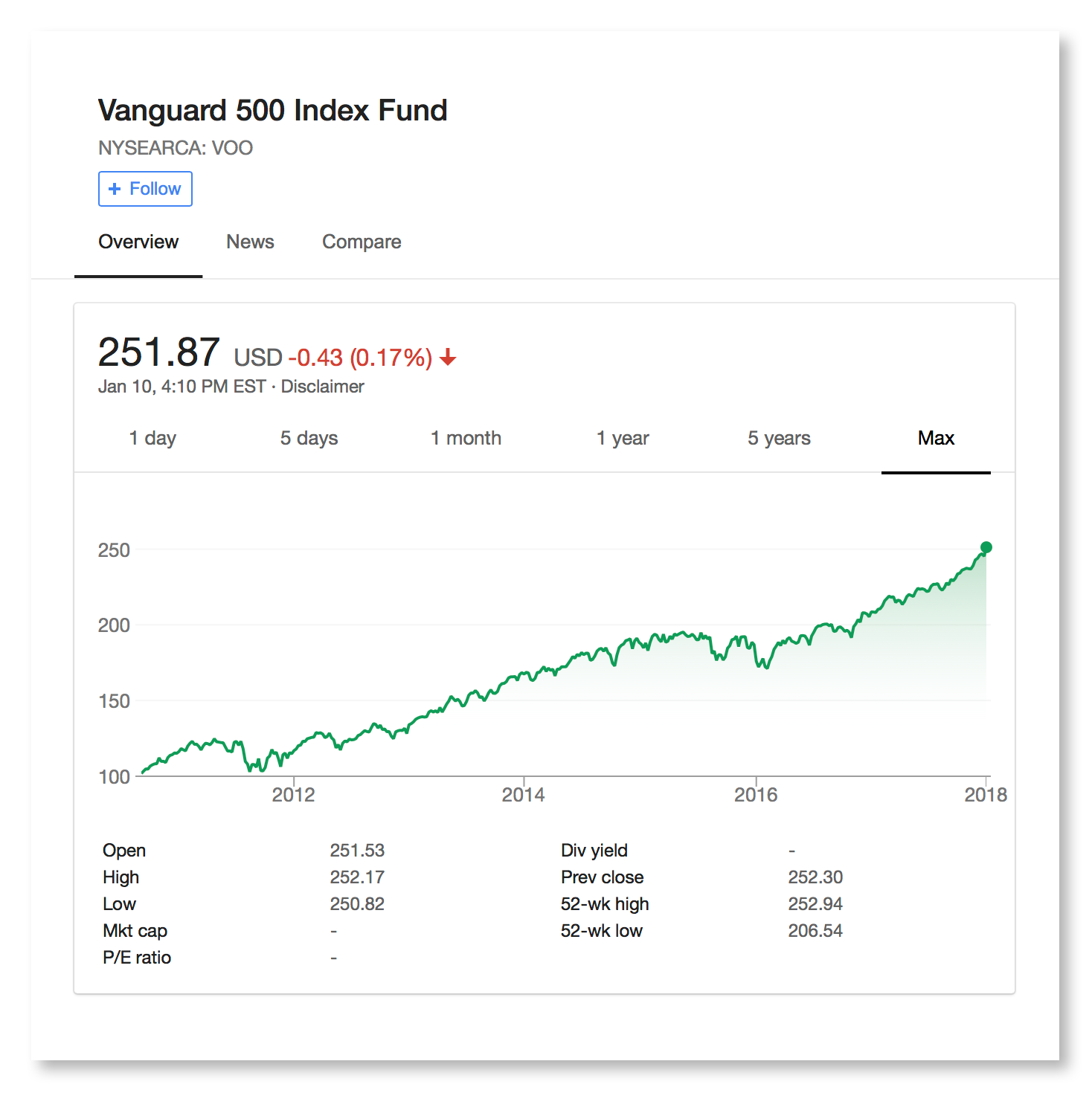

Not sure where invest your money? Take Warren Buffett’s (4th richest man in the world) advice and put it in a low-cost index fund like VOO.

Are you trying to disappoint the money gods? If you aren’t contributing to your 401k at work or to your own IRA, their anger is intense and the lightning bolts are coming your way. The only way to remedy this is to start contributing monthly to a retirement account of your choice. If you have access to a 401k through your employer, this is likely your best bet. Most employers offer a healthy match if you’ll contribute a portion of your salary. Don’t have a 401k? There are many other ways you can start investing for the long term. Our preference here at HTM is that you start a Roth IRA with a fantastic company like Vanguard.

Forsaking your budget

Thou shalt have a budget. Wasn’t that on the tablets that Moses brought down? Ok, I guess it didn’t quite make the cut, however, a budget is crucial for almost everyone. If you don’t see and document where your dollars go, how can you ensure that they are being allocated to the right places? And if your dollars are marching off to do the bidding of your impulses, and not oriented towards your goals, you are digging a money ditch that can be hard to climb out of.

When most people hear the term “budget” they immediately start to think of a drill officer yelling at them to get their money affairs in order – stat! But really, a budget is a reflection of your values. It provides the framework to help you avoid spending frivolously and aids you in putting your hard-earned dollars towards the things that matter to you. Creating a budget can lead to some life-changing soul searching. And that’s a good thing. You can listen to one of our recent podcast episodes about budgeting for more.

Giving in to impulse purchases

At $1000, a shiny new iPhone is easily becoming the most expensive impulse purchase today.

Impulse purchases are mighty sinful. They can kill that aforementioned budget and lead to credit card debt that might make you feel like you are in Dante’s seventh circle of hell. Impulse purchases are essentially akin to taking a bite out of the apple in the garden of Eden. It just looks so good – but the results are harsh and long-lasting.

Do whatever it takes to curb thoughtless and knee-jerk purchases in your life. If you purchase a latte every time you walk by a Starbucks, take a different route and avoid that temptation altogether. If you find yourself perusing your favorite online store a few evenings a week and purchasing new clothing, institute a rule that you aren’t allowed to buy any new clothing items until you donate a similar item from your wardrobe. That will at least cause you to think through those purchases before you click and enter your card info.

Psychology Today did a great write-up on why we actually end up purchasing on impulse. Knowing the why behind our actions can be incredibly helpful as we seek to change our behavior.

Related: Should you buy it checklist!

Taking out terrible loans

The worst sin you can commit – equivalent to money murder – is taking out a payday loan or title loan. These short-term loans charge exorbitant rates of interest. And people taking them out often find themselves beholden to a second and third loan from these loan providers. It’s a vicious cycle.

Sadly, taking out loans for everyday purchases is commonplace in American society these days. You can get a loan when you need a new HVAC system…or for minor dental work…or for a new bike…or just to snag a new loveseat. We’ve become a society that focuses not on what they can truly afford, but on whether they believe they can afford the payments that they string out over a long period of time. Be very reticent to take out loans for smaller purchases. This sin is deadly.

Ps. If you do use credit cards, make sure to ALWAYS stick to the credit card best practices.

“Investing” in rapidly depreciating assets

I can’t tell you the number of times I’ve heard people use the word “investment” in reference to a television or a car…or any other number of assets that actually depreciate quite rapidly. It’s ok to splurge on a new TV (if it’s in your budget), but don’t think of consumer purchases as an investment. Putting lots of money into your car or consumer electronic items is a lifestyle purchase, not an investment. And it is most definitely a money sin to call a rapidly depreciating purchase an “investment.”

Simplify your life. Stop committing heinous money sins against your future self. Truly invest your money by finding things to spend your funds on that will actually provide a return on your investment. Even putting your money in a home isn’t a guaranteed way to grow your money; just check out this calculator at NerdWallet to see if you should rent vs buy. But for the love of all that is holy, don’t call your fun purchases and investment just to soothe your conscience.

Lacking basic insurance coverage

You know what breaks my heart? Turning on the local news and seeing an apartment fire. It’s obviously a horrific situation. But what often compounds that tragedy and causes financial suffering for years to come is the fact that almost every single person in that complex likely lacked renters insurance. Statistically, only 37% of renters actually have renters insurance coverage.

Forsaking basic insurance coverage like auto, home, renters, and term-life are money misdeeds that could dig you a deep financial grave. Most of these insurance coverages are actually quite cheap as well. Renters insurance will likely cost you $20 a month or less. Term-life coverage, if you are young and in good health, will have a similar monthly expense. If you can’t afford the expense of car insurance, you really need to forego having a car at all. The consequences of not being covered are far greater than the minimal monthly expense.

These money sins are incredibly prevalent in our society, but don’t let the transgressions of others lead you astray! You can change. You can avoid these pitfalls. Turn from your money mistakes and see the beauteous light of real financial happiness. Taking the narrow path and putting aside these money misdeeds will impact your future self in many positive ways.