Today’s question comes from Nicholas in Richfield, OH…

“Hi, Matt, and Joel. I had a question about an investment option for $60k that I currently have sitting in my Vanguard money market account.

A little background on my wife and I. I am 38 years old and a schoolteacher. My wife is 33 years old and a nurse. We are in money gear #7. We have a full 6 months of savings in a HYSA account for our emergencies. We fully fund both of our Roth IRAs and put about $7k a year into a 529 plan for my daughter.

We max out my wife’s 401k each year. I put about $7.5k in my 403B account. I also contribute about $9.5k to my state teacher retirement for my pension.

We have a taxable brokerage account with about $24k in it. Our house and our cars are all paid off.

My question to you is: Should I dollar cost average all of this $60,000 into VOO? And then if I should, what kind of time frame should I be looking at to do this?

I was thinking maybe over the course of a year. Should I look to spread this out even longer? Should I look into short-term CDs to put some of it in there?

Or are there other options I haven’t considered? Thank you for your time.”

The short answer:

Wow, Nicholas! What you and your wife are doing is incredible. You’re both working in salt-of-the-earth professions, and on top of that you’re crushing it financially. Congrats!

The quick answer to your question is: Investing ALL of that cash in a single lump sum is historically a smarter financial move vs. dollar cost averaging.

Considering the stock market goes up 75% of the time, you’re more likely to come out ahead from a compounding perspective by tossing it all into VOO in one fell swoop.

But, that’s not the only option for investing or saving that money. Here’s the longer answer:

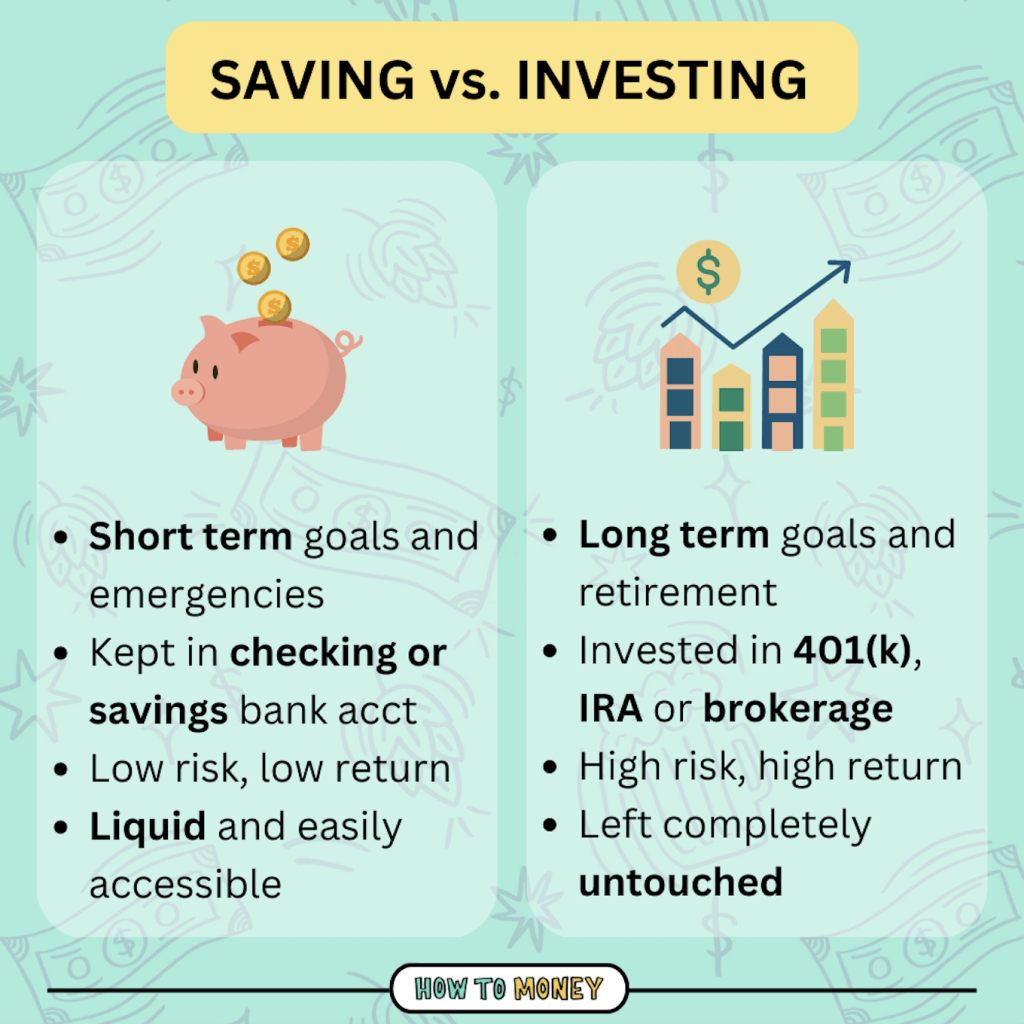

Saving vs investing

So what should you do with an extra $60k when you’re already maxing out your 401k and have paid off all your debts?

You mentioned both savings and investing options. Which route you choose to go will depend on your specific family goals.

Ask yourself: What do you want to reserve that $60k for and when do you need it back?

If this is money you intend to use in the next 2-3 years, I’d go with a CD or HYSA.

If you’re planning on renovating or upgrading your home, or upgrading your car or something, you’d want some of that money to be relatively liquid.

For long-term investing though, you’d be sticking it into your after-tax brokerage account.

If you wanted to keep $14k aside to fund both you and your wife’s Roth IRA’s come January, that might be a good option too.

Especially with CD rates falling, as long as you have a solid e-fund (you likely need a smaller one given that you live frugally and have no debts), I’d op to invest rather than save.

DCA vs lump sum investing

We love the idea of putting that money into index funds – or VOO specifically as you mentioned.

Should you do it all at once or slowly over time? Data would point to a lump sum investment being financially smarter.

I know, it’s tough to invest when the market is at all-time highs. But, emotions will mess you up and suggest that you invest little by little.

But in the long run, given historical performance, you’ve got a better chance of making a higher return by investing all at once.

Nobody can predict what is going to happen in the next 6-12 months. The stock market could keep ripping, or it could drop a bit.

One thing’s for sure though… in the long run, it always goes up. So in 30 years, you’re going to be sitting on much more no matter how you invest today. There is no “wrong” decision.

I suggest you play around with this DCA vs. Lump Sum calculator. Given your dollar amount and time frame, you’ll quickly realize your best option is to invest in a lump sum.

Dealing with emotions

It’s hard to turn off human emotions when investing. Money is emotional, after all! It’s a very real factor.

So if you feel like you couldn’t stomach a meaningful drop in the market soon after putting the full $6k0 in, it’s ok to dollar cost average over a 6-month or 1-year timeline!

Even if it’s not the most optimized thing in the world, the peace of mind alone might be worth it. You’re already ahead financially, so not every single money move needs to be 100% optimized.

The risks of dollar cost averaging, however, are that you miss out on gains. Or, fail to invest it all and find yourself still with a huge chunk of cash this same time next year.

If you do go the DCA route, make sure you automate those contributions on a recurring two-week or first-of-every-month schedule. That way you don’t forget or attempt to time the market over that timeline.

Spend a little!

It’s also worth mentioning another option: Spending and enjoying some of that money right now.

You’re already well ahead in terms of retirement planning and long-term goals. You’ve eliminated debts completely & you’re socking away what is likely a big chunk of your paycheck towards investing goals.

We hate to disincentivize investing, but we’d suggest spending some time pondering your medium-term hopes & dreams.

It’s rare, but some folks actually over-invest for their future. If you’ve done well on the investing front over a long period of time, it’s important to take stock of what we want our lives to look like now. Spending some of those dollars now could lead to increased joy. And you’ll still have plenty decades down the road!

By all means, if you are stoked with your current life and truly want to invest the money, great! But the truth is you and your wife might retire with far more than you actually need given your lifestyle and habits.

Most money shows don’t push people to invest less. But hey, we are not most money shows!

The Bottom Line:

Congrats on your solid money situation. At this point, we’d recommend taking a step back and figuring out your short and medium-term goals for your family. This helps determine whether you should save (HYSA or CD) or invest (brokerage account) that money.

If you do end up investing that money long term, history says to do it in one single transaction. Invest the money ASAP, because time IN the market beats timING the market.

Good luck Nicholas!

For the full version of this discussion, check out Podcast Episode #892 (it’s the 2nd question in the episode)

Related posts: