Good morning and happy Tuesday!! ☕️

Here’s a common question we get… “What if I invest my money and the market crashes?”

And here’s our usual response —> What if you invest and the market doesn’t crash? What if it goes UP?

Sometimes flipping the question ⤵ flips the perspective. ⤴

- “What if I apply for that job and I don’t get it?” —> What if you apply for that job and you DO get it?

- “What if I save a bunch of money and die next year?” —> What if you don’t save any money and live until you’re 110!?

- “What if I buy a house and decide to move after only 6 months?” —> What if you absolutely love it and live there forever?

Something to try this week: If you have any scary decisions ahead or self-doubting questions right now in your life… try flipping the script.

It might shine some much needed positive perspective on the situation 💪🙌😎

TO DO

Use those old gift cards! 💳

Did you know… 47% of U.S. adults say they have at least 1 unused gift card, voucher or store credit, adding up to $21 BILLION nationwide!!?

That’s a lot of money! And every day that money is losing value to inflation, expiring, or being lost in a random drawer somewhere.

If you have a gift card or store credit: Use it!

- Plan a date night!

- Buy someone a gift for Christmas

- Sell it on a site like CardCash

- Here’s an awesome site to check your state laws to see if you can trade in low balances for cash (for example, in California any gift card balance under $10 can, and legally must, be exchanged for cash by the retailer)

Let’s all spend our gift cards and reduce that 21 Billion statistic down to at least 20.9 Billion, yeah?

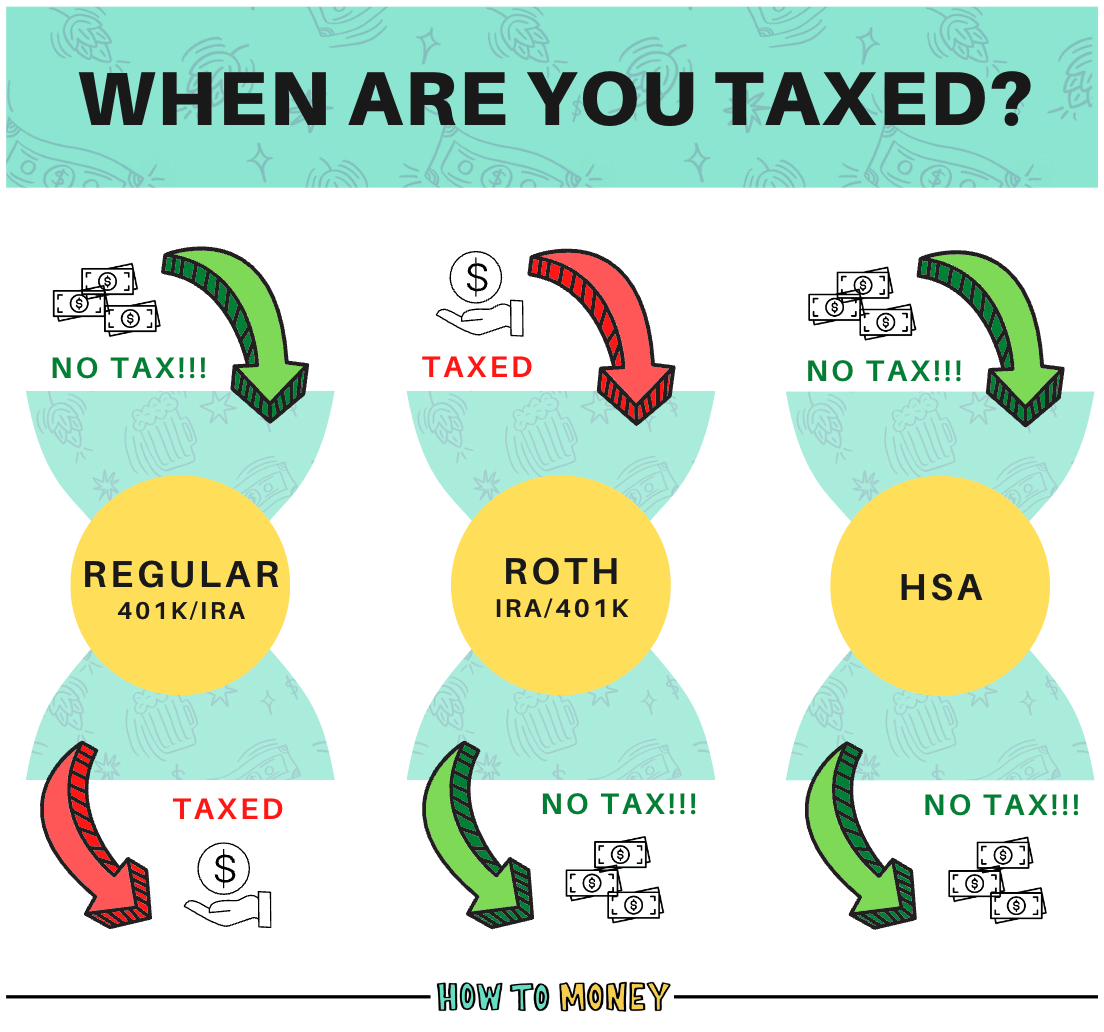

TAXES (OR LACK THEROF)

Roth vs. Traditional vs. HSA

For the most part, taxes are unavoidable in life. But, by using a tax advantaged retirement account, you can kind of control *when* you pay taxes. (which could lead to paying significantly less throughout your lifetime!)

Here is an oversimplified quick view of when you’re taxed, with these tax advantaged retirement accounts…

Traditional 401(k)/IRA: No tax when you put money in, but you’ll have to pay later when you take it out in retirement. The benefit here is that if you expect to be in a lower income tax bracket later in life (most people do) you can pay a lower amount of tax later, versus a higher amount now. The only caveat being that rates of taxation are likely to be higher than where they are currently.

ROTH 401(k)/IRA: Everybody’s favorite account! 🥰 You pay taxes on your income now, and then invest that money into a Roth… Once it’s in a Roth you don’t EVER get taxed again!! (assuming you keep it in there until retirement age)

HSA (Health Savings Account): This is THE MOST tax efficient investment vehicle available. But, annual contribution limits are pretty low ($3,650 for self-only and $7,300 for families for ’22). You also need to be enrolled in a HDHP and all withdrawals need to be for qualified medical expenses. However, if you still have funds in your HSA when you turn 65, you can tap those funds for any reason- just like with a traditional IRA. The thing is, the HSA has a branding problem: we prefer for you to use it as a way to invest for retirement and less as a tool to save for current medical expenses.

Which retirement account is the BEST? —> That depends on your age, income, employer, health, and a bunch of other personal factors. Honestly the best solution is maxing out ALL OF THEM! 🤣

**Probably a good time to remind you that we are not tax professionals and again this is an oversimplification of the US tax laws. Each retirement account has various withdrawal nuances, contribution limits, etc so please do your thorough research before stuffing money into these accounts and becoming filthy rich**

More info:

- 🎙 Episode 83: The Beauty of the Roth IRA (40 mins)

- 🤷♂️ New HTM Blog: Should I invest in a Roth or Traditional IRA?

- 💻 401k vs. IRA: What’s the difference? (5 min read)

- 📝 HTM Blog Post: HSA: The Ultimate Retirement Account (5 min read)

INVESTING

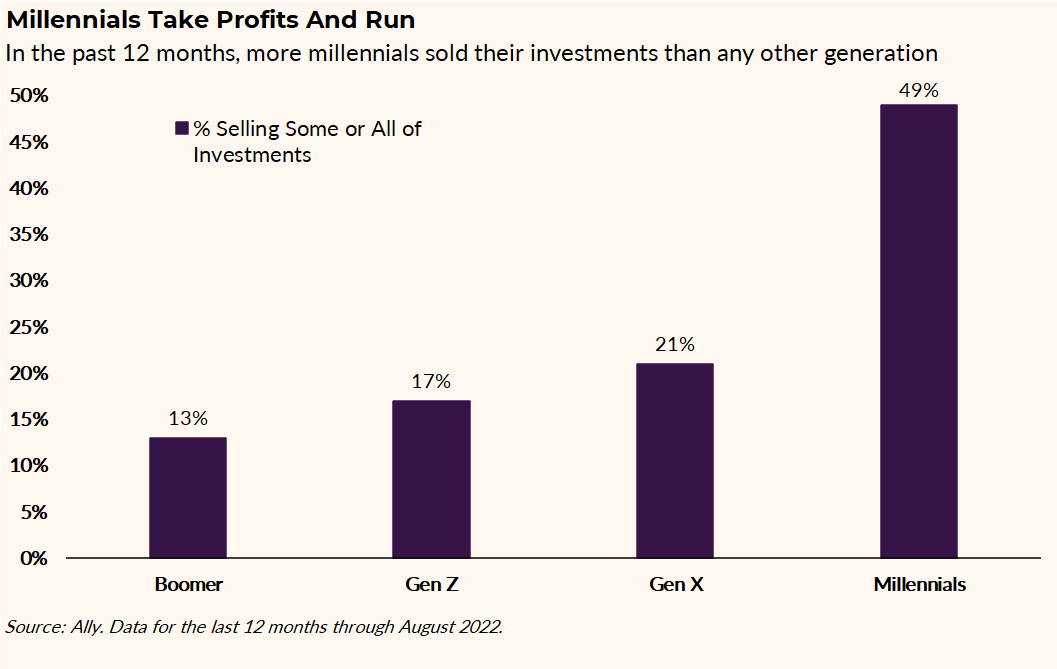

Interesting (and sad) chart of the week 😭

This one comes from our friends over at Ally, based on a recent survey they conducted on investors over the past 12 months.

Here is the generation breakdown of respondents that admitted they sold “some or all of their investments” 👇👇👇

WHY did these Millennials sell? Here are the two most common survey responses:

- Inflation: “I sold my investments to cover my household expenses”

- Crypto: “I lost some or all of the money I had invested in crypto”

There are a million things I could comment about this, but I’ll spare you and just share the top 3…

1) The importance of an emergency fund

There’s a reason that building a basic emergency fund is our first Money Gear. Having cash on hand to pay for unknown expenses (or sudden increases in living costs) means you won’t have to pull from your investments at inopportune times.

2) Crypto volatility and risk

Stocks are volatile, there’s no doubt about that… But crypto is EXTREMELY volatile. The highs are high, and the lows are low (and in some cases, ZERO). With such massive swings and potential total loss, crypto should only be invested in with a small portion of your portfolio.

3) Time is your biggest asset

Millennials (26-41 year olds) still have plenty of time to invest and grow their wealth. But in order for compound interest to do it’s thang, that money needs to remain invested for the long haul. Wherever you put it –> leave it.

Related resources:

- 🎙 Podcast Episode 521: Is The Stock Market Broken? (55 mins)

- 💻 HTM blog post: How to move out of your parents house

- 📚 Book Reco: The Simple Path to Wealth (not too long, and has great explanations and how to’s for long term investing)

ICYMI

Extra, extra, read all about it…

Inflation 📉

Over the past 12 months the “all items index” increased 8.3%, so says the latest CPI data report. Food, shelter and medical care indexes were the largest contributors, but these increases were mostly offset by a -10.6% decline in the gasoline index.

Loan Forgiveness 🏛

While student debt relief isn’t subject to *federal* taxes… depending on your home state, you might have to pay *state* income tax on any forgiveness amount you receive. Here are 7 states likely to enforce state tax (NC, IN, MS, AR, MN, WI and Taxifornia) — keep in mind rules might change on this before forgiveness or filing happens!

College 👩🎓

Apparently 2 out of every 5 college grads have regrets about their degree! Here are the most regretted (and lowest paying) college majors per Washington Post.

Zelle Scams 🙅

If a stranger “accidentally” sends you money via Venmo or Zelle, this is probably a scam… Don’t return the money or interact with them —> just report the transaction right away to your bank.

Michael Jordan 🙏

Nearly half a million students across 639 high schools will have access to personal finance courses, thanks to a MASSIVE donation from Michael Jordan and the Jordan Brand! The grant was given to Next Gen Personal Finance who is on a mission to make sure ALL high schoolers graduate with better personal finance knowledge! 🥳

HOW *YOU* MONEY

Sarah & William, 30y/o from Richmond, VA 🏛

Occupations: HR Manager (Sarah), Special Ed Teacher (William)

Combined Salaries: $130,000/year

Paycheck deductions: $2,500 taxes, $300 health ins, $2,076 retirement accts,

Rent: -$1,600/m

Other debts: -$400/m (car) and ~$8,000 (student loans **just announced this is being forgiven!!**)

Living expenses: -$1,500/m

Leftover savings each month: ~$2,450!!

How are you investing your excess savings each month?

We max out both of our Roth IRA’s at the very start of the year (I keep a high balance in my savings account to fund), and I fully fund $20,500 into my 401k over the course of the year. William contributes the max to his work-sponsored retirement accounts which is actually very minimal (he has limited options as a public school teacher) so to add flexibility and get us closer to FI I typically put ~$1,400 into a taxable brokerage account each month.

Biggest “craft beer equivalent” splurge:

As a couple– Travel! My husband and I have fallen in love with the Caribbean and I will spend lots of money for a nice AirBnB and flights to an island where we can snorkel with sea turtles. Personally, I (Sarah) have also just gotten back into horseback riding!

Best savings hack/advice:

This one might be controversial but I do use rewards apps to earn gift cards. Then when I WANT something from Amazon, I tell myself I can’t buy it until I have enough money in gift cards. I know survey sites and points sites are a time suck so I really limit the time I spend on them but the act of delaying helps me to not spend impulsively, and when I use gift cards it feels like an extra special treat that I got for free! Another BIG thing for me has been salary negotiating. I have gotten two 50% increases in the last two and a half years. I also do a little side hustling with some babysitting gigs!

Anything else you want to share?

I am a recovering alcoholic (7 years sober!) and as of 8 years ago, I was in a hospital ICU for 5 days with pancreatitis, alcoholic hepatitis and bleeding esophageal varices. I went to inpatient treatment and got into recovery and have not had a drink since October 3, 2014. My sobriety and spiritual recovery are most important to me; however, once I had some footing in program, I had to work on my finances because I had a maxed out credit card that I wasn’t paying on; $15,000 in student loans that were in default because…I wasn’t paying them AND I wasn’t in school and had no degree to show for the debt; a credit score of (I kid you not) 300; and NEGATIVE $13 in the bank! Negative! Because of overdraft fees and insufficient funds fees. I was living with my parents and unemployable for about a year. BUT I slowly started getting a clear picture of my finances and how to improve them and thanks to education from podcasts such as yours, I am a total Money Nerd and have a healthy income, a six-figure net worth, a credit score that is ALMOST 800 and most importantly, a husband who has never seen me drink and two sassy cat babies 🙂 So no matter where you are right now, it can get better!

**Have YOU got an interesting story or money profile to share? We’d love to hear it (and share it). Fill out the How You Money form here**

Cheers for reading, as always. Not sure what the craft beer equivalent is in your life… but whatever it is, we’re wishing you a week FULL of it!!

Best friends out 🍻

PS. Big THANK YOU to Ally’s Lindsey Bell for including us in her list of fav money podcasts. 😊

*****

* Advertiser Disclosure: How to Money has partnered with CardRatings for our coverage of credit card products. How to Money and CardRatings may receive a commission from card issuers.

* User Generated Content Disclosure: Responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.