Today’s question comes from Peter in Texas…

“Hi, Joel and Matt. I’m twenty four and I’m currently stationed in Apostle, Texas with the Army.

I’ve been hooked on your podcast for about seven months now, and thanks to you guys, I’ve paid off a 72 month car loan prematurely, shaving off 53 grueling months of interest. I’ve also been budgeting with YNAB, and have hit Money Gear 5!

Back in college, I grasped the idea of compound interest, and how Roth IRAs were a great vehicle for financial freedom. I’m a natural saver, but I lacked confidence in investing at the time, so I turned to an Edwards Jones advisor for assistance.

My advisor puts my deposits into an investment savings account consisting of mutual funds to grow my money, and pulls money out of that account to max out my Roth IRA each year. My Roth account consists of mutual funds too.

From the beginning of 2020 until now, I’ve contributed a total of $42,000 to the investment savings account. Its current value sits at $19k and my Roth IRA sits at $43.6k.

I’ve noticed that you guys referenced Vanguard and Fidelity for Roth IRAs and also lean towards index funds. Should I switch my portfolio to index funds for better returns in this wealth building phase?

Or should I consider shifting to Vanguard or Fidelity? If so, how would I navigate this switch? Thank you both for your priceless guidance. Take care.”

Matt & Joel’s Reponse:

First and foremost, thank you for your service, Peter!

You’re a young dude with a lot of life ahead of you. So we’re glad to hear you’re starting to invest early and making smart moves with your money.

You got rid of that car loan QUICK, which means you’re highly motivated. That’ll help you make rapid progress!

Using helpful budgeting tools like YNAB is a brilliant move too. Apps like that can offer the insight and motivation to keep doing the right things. You’re crushing it on so many levels.

The short answer regarding your advisor: We think this is work you can do on your own. Moving money to a Roth and picking index funds really isn’t all that difficult.

Let’s talk more about the process of ditching your advisor, and self managing your accounts…

Advisors cost a LOT

The reason we’re not typically enthusiastic about you having an advisor at your age is because a good portion of the money you could be investing is lining the pockets of the advisor.

The tiny fees they charge might seem insignificant. But boy do they add up over time. They seriously eat into the compounding process and erode your potential wealth.

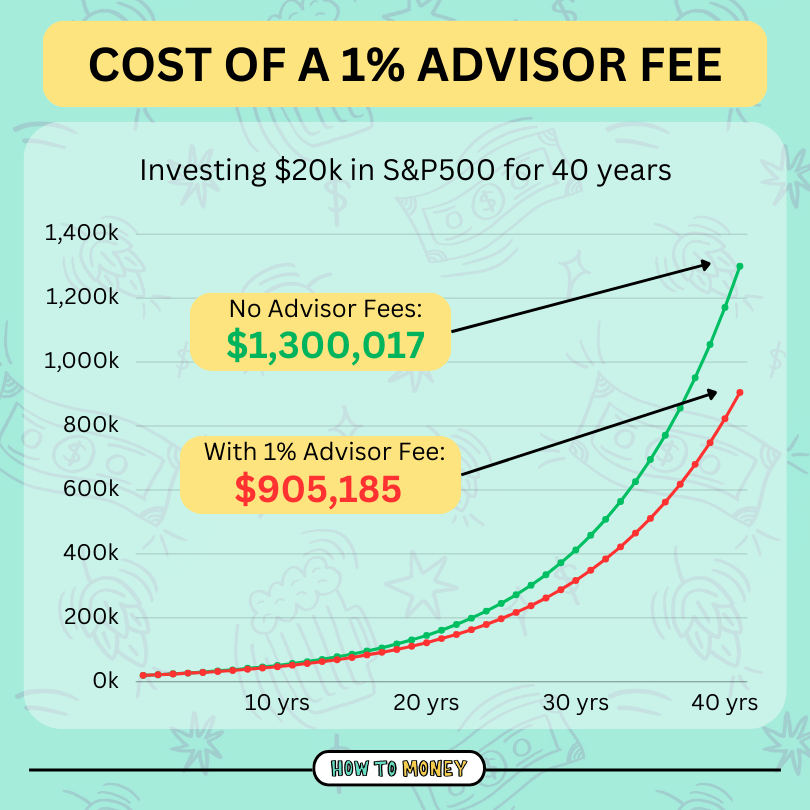

A 1% fee every year could cost you hundreds of thousands of dollars after decades of compounding. It’s crazy to think about!

I get why you went in that direction starting out. Investing can be confusing, especially for beginners.

But at this point you’ve received a solid financial education listening to this show, and probably other checking out other free money resources.

So I think it’s time to mosey on down the road and take the DIY approach.

That way, all the fees you pay your advisor (and also the management fees of the funds they have you invested in) would be saved and work for you inside of tax-advantaged accounts.

DIY investing

When you manage your own investments, you don’t just save fees. You get to pick the index funds and brokerage firm that you like and feel comfortable with.

You mentioned Vanguard, which is an excellent choice. They don’t charge monthly account fees, and they promote broad, low cost index funds. Fidelity is a great choice, too. You can open a Roth IRA in less than 10 minutes online, at no cost.

We’ll talk about transferring your accounts over from Edward Jones in a little bit.

As for which funds to pick, here are our favorite index funds.

At your age Peter, you can afford to hold a pretty aggressive portfolio. That’s because you’ve got decades on the investment horizon for those investments to grow.

It’s not uncommon for folks your age to have a 100% stock portfolio, or maybe 90% stocks and 10% bonds.

Ditching your advisor

So how do you break up with your advisor? We’ve got an article with helpful scripts to let them down gently and end things on a positive note.

Start with a simple email outlining your growing confidence and desire to self-manage your assets. It’s kind of like the old “it’s not you, it’s me” break up approach.

I’d request any important documents and statements you might need to keep for the future. You’ll definitely want to keep track of those original contribution amounts.

Don’t be surprised if the advisor fights back and tries to keep your business. They’ll use all types of tactics to instill fear and make you feel like you’re making the wrong move.

Be prepared to stick to your guns, and tell them you truly want to self-manage. It’s nerve wracking, but trust me you’ll feel great afterwards.

Moving to a new broker

Next, contact Vanguard (or whichever low cost broker you choose) directly and inquire about the process to move your accounts over.

The form you’ll typically need to fill out is called an ACAT (automated customer account transfer). This should make the migration clean and easy. They will simply transfer all the assets from one custodian to the other, without cashing out any investments and having to rebuy.

Lastly, once all the funds have landed in your new broker account, it’s time to change investments!

The good news is inside your Roth IRA (or any tax-advantaged account) you won’t pay any capital gains for buying/selling funds. So you can sell whatever positions Eward Jones had you in, and move everything to cheap index funds.

Future contributions

You mentioned your current advisor moves money around on your behalf. This is something you’ll want to handle yourself going forward.

The best way will be to automate those monthly contributions. Set up repeating transfers into the accounts you want to fund. You’ll likely want to have both a Roth IRA and a brokerage account with your new low-cost brokerage firm.

Money Gear #5 is a great place to be. After you’ve taken advantage of those accounts, it’s time to keep moving up the gears!

Not all advisors are bad

By the way, we’re not completely against financial advisors. They can make sense for certain folks.

If you need an advisor, we’ve partnered with the folks at Wealthramp to help you find one that meets our high standards. Wealthramp works with a network of independent, fee-only fiduciary advisors you can trust. You can even schedule a complimentary meeting. If you’re in need of a professional who can help you keep your financial goals on track, start here.

The Bottom Line:

I know it might seem daunting, but you’re doing a great job. And the bottom line is that breaking up with your financial advisor will help you build an even bigger pile of wealth in the future.

Keep learning and keep your investing real simple. You got this! 💪

For the full version of this discussion, check out Podcast Episode #823 (it’s the 1st question in the episode)

Related posts:

- Investing 101: A Beginner’s Guide

- 6 Reasons Why Most People Lose Money in the Stock Market

- How to Invest During Volatile Markets

**Affiliate disclosure: How To Money may be compensated by Nectarine if you use our affiliate link to make a purchase, which creates an incentive and conflict of interest. We are not current clients or employees of Nectarine.