Good morning, wealth builders!!

Fill in the blanks…

1) This week I will save money on _______…

2) But being frugal allows me to splurge on _______, which I love!

3) When my paycheck lands on _______ day, a portion will be auto-transferred into my ______ account.

4) I invest my money in _______, because building passive income is important to me.

5) Financial freedom means _______ to me, and nobody is gonna get in my way of achieving that.

OK, now let’s put these words into action. 👇👇👇

TO DO

Search For Missing Money

About 1 in 10 Americans have unclaimed property, aka “missing money” floating around out there that they don’t know about.

Head on over to MissingMoney.com, a free site that helps you search the databases across all states and provinces to find unclaimed funds. We recommend checking this site every so often, as new properties are added every day!

*Bonus points* if you search for your friends and family members too! Helping others find lost money is 🏆💪🙌

CREDIT CARDS

Are Reward Points Actually Worth It? 💳

We talk about taking advantage of credit card points all the time — but we rarely discuss how the poor use of cards can turn a perk into a punishment.

Let’s not forget, banks are in the business of making money. For all the rewards and cash back they’re doling out, they’re raking in far more from other people thanks to the poor spending habits of most credit card users.

Most people apply for credit cards with good intentions, but might end up paying more in interest, than the rewards they think they’re accumulating. Here are some scenarios to watch out for:

1) Not paying the full balance each month: If you don’t pay the full statement balance, you’re likely paying interest in the range of 20-25%!! This racks up quickly and eclipses any rewards you might be getting.

2) High annual fees: If you gain $20 in rewards each month, but pay $295 for the card annually, you’re actually underwater! A good practice is to annually review your cards and figure out which ones are worth keeping. (pro tip: Instead of cancelling them, call the credit card company and ask to migrate to a lower tier card with no annual fee)

3) Letting points/rewards expire: If you earn a bunch of rewards, but never actually use them, what’s the point? Treat yourself to a statement credit, request a cash back deposit, or even opt to take a trip with those points!

4) Rewards that encourage shopping more: Many credit card reward programs are designed to encourage spending. And although some of it might be “free” or discounted, usually it leads to spending more than you usually would in the first place. (For example, getting a 90% discount on a pair of cowboy boots… You might be thinking, “Woohoo, I got a massive discount!” but the reality is you spent more than you typically would because you never wear cowboy boots… even if you’re binge-watching Yellowstone.)

5) Low interest (at the beginning): Balance transfer cards and 0% APR cards are great when you first get them. But when rate changes, boom! You’re hit with massive fees that end up costing more than just tackling your debt properly in the first place. Balance transfer cards can be a helpful tool, but only when you use them properly.

All in all, credit cards are a blessing and a curse. Sadly, more people are on the curse side than the blessing side. Be careful you are not one of them!

Related:

- 💻 The Vox Post: Your credit card points might not be worth it

- 🧑💻 What’s in Our Wallet? Here are the cards Joel and Matt use!

- 🙌 HTM Blog: Top Frugal Habits to Save Money in Everyday Life

INVESTING

The TRIPLE Tax-Advantage of HSAs

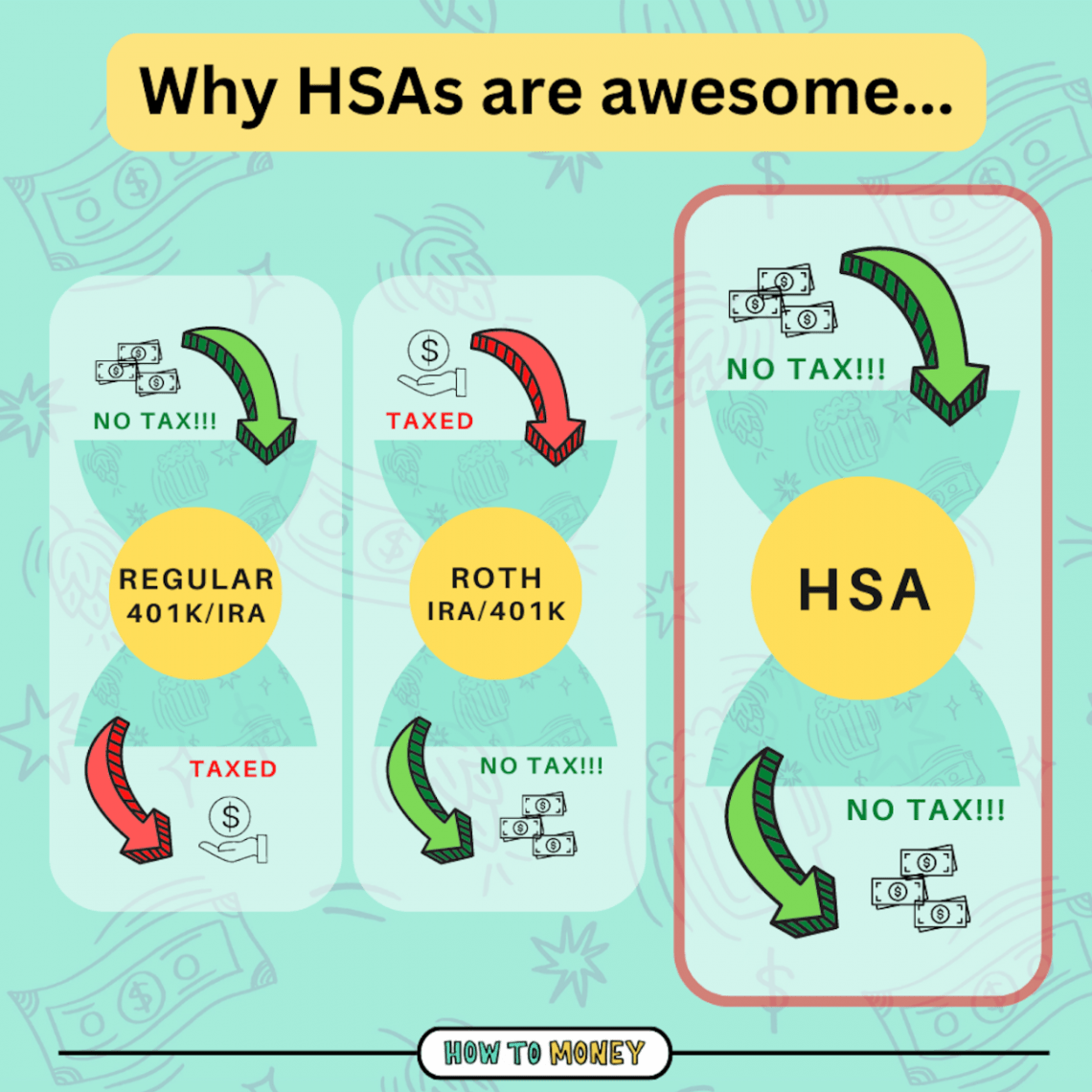

401k accounts and IRAs are awesome because you pay no income tax on the money you put in. But, you pay taxes when you withdraw money later.

Roth accounts are awesome because you pay no tax on growth or when you withdraw money. But, all the dollars you contribute today are taxed.

HSAs… They are in a class of their own.

There are 3 main tax benefits for HSAs:

1) No tax going in: For work sponsored plans, HSA contributions are deducted from your paycheck, pre-tax! For self directed HSAs you can deduct contributions when you file your taxes.

2) No tax on growth: Interest, dividends, and growth all remain within your HSA account, compounding without taxation. This is why it’s important to invest those funds, not save, for maximum tax exempt growth.

3) No tax going out: When you withdraw funds for qualified medical expenses, you pay no tax. Triple tax-advantaged status UNLOCKED!

You might be wondering… What if I save up too much money in my HSA and have no medical expenses to deduct? Well, in that scenario, at age 65 your HSA is treated just like a traditional IRA. You’ll be taxed on withdrawals, but pay no penalty or fees. Another option — at age 65 you can use your HSA money to pay for medicare premiums, deductibles, copays, and coinsurance. Bottom line: you won’t run the risk of over contributing!

More about HSAs:

- 👨💻 HTM Blog: Using your HSA like an investing genius!

- 📝 Mad FIentist: Saving medical receipts & delaying reimbursement

ICYMI

Other Stuff Happening in the World…

12 Cents 🌭

Sam’s Club has reduced the price of their hotdog + soda combo from $1.50 down to $1.38. A saving of 12 cents… So what? Every penny counts! (BTW — their food court is available to both members and non-members 😉)

Pet Boom 🐕🦺

According to new BLS data, US households are spending double the amount on pets compared to 10 years ago. This is partly because of the pandemic pet boom, and partly because pet services (like vets) are being scooped up by private equity firms. 🤔

Pay Boost 🎯

Target just announced they are raising their minimum wage to $24 an hour in certain locations. (it’s already at $15 nationwide). This shows just how competitive the labor market is – especially in that lower-tier range. In addition to that pay bump, Target has decreased the number of hours that employees need to work to be eligible for health benefits, down to 25 a week!

Bank of Mom & Dad 👨👩👦

A recent Credit Karma report revealed that about a third of parents with adult children are providing them with financial support (and in many cases jeopardizing their own retirement as a result). It’s never been more important to teach your kids about saving/investing and becoming self sufficient!

FRIENDS OF HTM

Beth Moncel of Budget Bytes

Before Beth was a food blogger, she was a microbiologist with a degree in nutritional science.

Now, she has a massively popular site called Budget Bytes where you can find simple, delicious recipes that are designed for folks with small budgets. Beth’s passion in life is to help others realize that good tasting food doesn’t have to be complicated, or expensive!

Food is one of the biggest expense categories for most households (after housing/transport), so why not try and learn some new cooking hacks this year to cut down your food bills — and make some good eats while you’re at it. Check out Beth’s blog, Insta, and cookbook!

That’s all for now, folks. Wishing you a mega productive week ahead, followed by a weekend of well deserved relaxing. Catch you next week!

Best friends out 🍻

*****

***some of the links in this newsletter are affiliate links and we receive a small commission if a product is purchased. Don’t worry, we only recommend stuff that we believe in 💯***