When it comes to buying a car, we always recommend finding a used, reliable vehicle and paying for it in cash. This avoids taking a massive depreciation hit on a brand new car, and allows you to avoid paying high interest rates for many years by avoiding a car loan altogether. However, we know that buying a car in cash isn’t always possible. Sometimes you have to finance a used car. So, what is the best way to do it?

In this post we’re going to talk about when financing makes sense, and lay out the step by step process of how to finance a used car.

The benefits of financing a used car

If you can’t buy a car outright, financing a used car will likely be your best option. Taking out a car loan can come with certain perks – it’s not always a horrible idea. The key is buying used vehicles instead of new, and getting the best deal on a loan you can. Here are some of the benefits of financing a used car.

Affording a better car

When you finance a used car (vs. paying cash), you might be able to afford a better vehicle. If you only have $5k in savings, the range of cars you can buy outright is quite small. Most of your available options will have tons of miles and unknown history. So you won’t be able to safely say that a $5k car will last you decades.

But if you used that $5k as your down payment, and got a car loan for another $15k, this dramatically increases the likelihood that you’ll be able to buy an extremely reliable used car. One that you can keep for decades to come.

Although getting a loan isn’t preferable, if it gets you into a more reliable set of wheels, it might just work out better in the long run.

Less depreciation

All cars depreciate in value. But used cars depreciate more slowly than brand new ones.

Studies show that new cars can lose around 20% of their value in just the first year of ownership! After that, each year they continue to lose around 15% of their value annually until they are four or five years old. That’s no chump change! For example, if you purchase a new car for $40,000, you can expect that car to be worth around $17,600 at the five year mark. Ouch!

Buying used means the prior owner takes the biggest depreciation hit. And you can swoop in at year 5 and get a solid vehicle with a lot of life left for a great value. Sure, the car will continue to depreciate while you own it. But at a much lower rate.

Less costly

Just like other used items, used cars cost less than their fancy new counterparts. The average cost of a new car is $48,389, while the average cost of a used car is around $28,371. That’s a $20k difference. You’ll see much more room in your budget month to month after financing a used car. While the average car payment for a new car is a whopping $730, the average monthly payment for a used car is $520.

Still sounding crazy expensive to you? You’re not alone in that. But the good news is that these are just averages. You don’t need to spend this much to get a reliable used car. In fact, there are a plethora of reliable and affordable used cars that you can sometimes even snag for under $5,000-10,000. Many of which will last you for years to come! You just need to be willing to do some extra research and shop around!

Less stress

I don’t know about you, but every time I own something brand new, I’m terrified of damaging it. Getting that first scratch on your brand new car can be super upsetting. While it’s important to take care of your car, getting a scratch on a used car that’s already a little bit dinged up is a lot less stressful than denting a brand new ride!

It’s also less stressful to finance a used reliable car vs. driving around a clunker that could break down at any moment. It sucks to be in debt and have monthly payments on a vehicle. But it sucks even more not knowing if your car is going to start and if you’ll make it to work on time.

How to Finance a Used Car

Financing a used car can be a little confusing, especially if you’ve never done it before. But if you follow these steps, you’ll be cruising down the open highway in your new ride in no time! Here’s how to finance a used car.

Step1: Take a look at your credit score

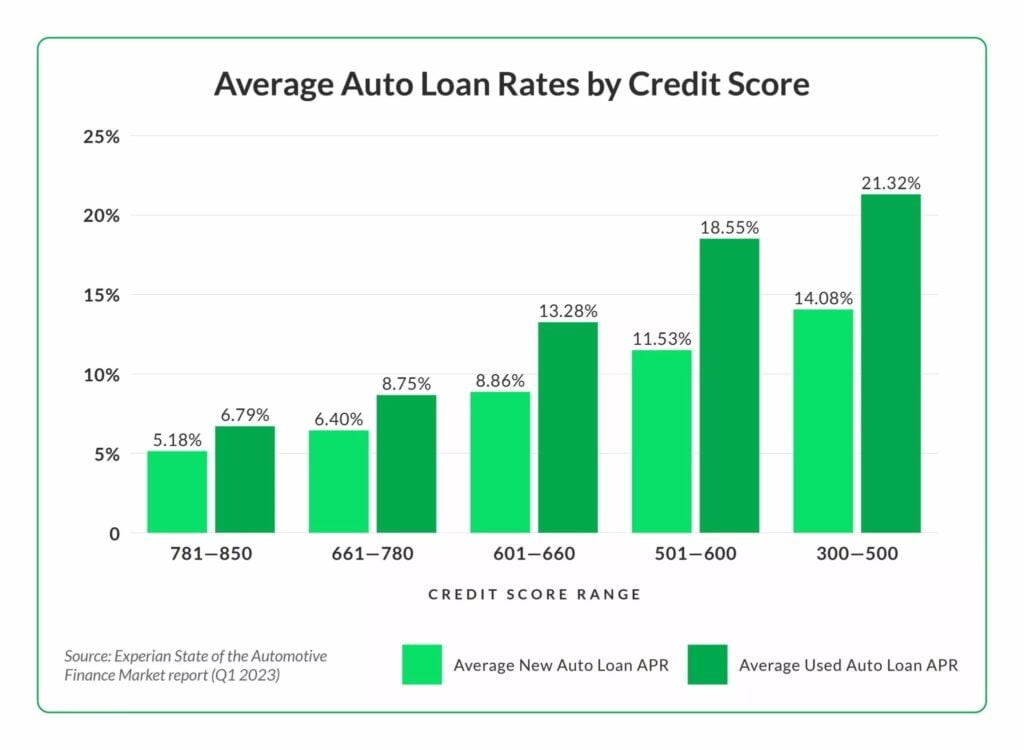

Your credit score will be a big factor when it comes time to finance a used car. It determines how much you’ll pay for your car over the life of your loan. The higher your credit score is, the better interest rate you will qualify for. On the flip side, a poor credit score will mean getting stuck with higher interest rates. Or, potentially not being approved for a loan at all.

Here’s a chart from MarketWatch, using recent data from Experian…

As you can see, if your credit score is in the high 700’s, you can look forward to the best loan rates. But if you’re in the low 700’s (which is still considered a “good” credit score), your rates can be 1-2 percentage points higher.

If you know that you’ll need to finance a used car in the near future, work on increasing your credit score. Checking your credit report is a great way to ensure there are no mistakes dragging your score down (you can get a free credit report here). Paying off any debt can also help to give your credit score a boost. It will lower your credit utilization rate. This makes up 30% of your score. And as always, be sure to always make credit card and bill payments in full and on time!

All in all, maintaining healthy credit can help you to save hundreds (or even thousands) of dollars over the life of your car loan. Make sure to prioritize rebuilding your credit score if it needs a little boost.

Step 2: Determine your needs

Next up, determine what you need when it comes to a good used car. No one needs a slick two door Lamborghini. But you might need an extra row of seats if you’re part of the Monday night soccer carpool. Or maybe you need an SUV with a lot of storage because you’re hauling gear back and forth for work. Making a list of features you can’t live without in your used car can help you to narrow down what models you’re interested in purchasing.

When considering your needs, be sure to think a few years into the future as well. We get the most value from our cars when we drive them for longer. So you want your next car to be something that is likely to suit your lifestyle for the next decade. That 2-seat Smartcar could be a good option for you and your spouse now, but if you’re looking to have kids in the next few years, it’s just not going to cut it.

Step 3: Make a budget

Next, it’s important to make a car budget to determine how much you’ll be able to afford. When making your budget, you need to come up with two numbers; how much money you’ll be able to use as a down payment, and how much you will be able to afford paying towards your car loan each month.

When it comes to your down payment, you want to put down as much as you can. The more money you put down, the less interest you will pay over the course of your loan. Plus, having a larger down payment can even mean walking away with a lower interest rate!

You’ll also need to figure out how big of a monthly payment you will be able to afford. For each person, this will be different. You’ll need to look at your monthly budget and determine how much money you’ll have available to put towards transportation.

This number isn’t what a lender says you can borrow. We’re talking about what makes sense in your budget. We recommend spending no more than 10% of your monthly income on your transportation expenses (including gas, insurance, maintenance and your car loan).

Lastly, don’t forget to factor in the cost of maintenance over the life of the car. AAA recommends saving at least $50 each month for routine maintenance, but we would also recommend saving the same amount each month for unexpected costs. If you drive a lot, or own an older car, you may want to save up even more. Here’s a longer guide to figuring out how much you should spend on a used car.

Step 4: Get pre-approved for a loan

Getting pre-approved for a car loan can be a helpful step in completing your budget. It’ll give you a baseline idea of what loan rates you’ll qualify for and will allow you to start comparing rates. You can get pre-approved using car buying websites like Carvana, from local credit unions, or from banks.

As for loan rates, it is almost always the cheapest option to get a loan at a local credit union. Credit unions are not-for-profit organizations, so their fees and interest are usually the lowest – often by a wide margin!

Don’t worry- when you get pre-approved, you aren’t actually committing to the loan. However, it’s important to note that lenders will do a hard check on your credit, which can affect your credit score. To cut down on damage to your score, make all of your inquiries within a 14 day window. If you do so, your inquiries could be rolled into a single inquiry, minimizing any drops in your score.

Step 5: Choose the length of your loan

Next, it’s time to choose your loan term.

When purchasing your car the frugal way, it’s important to choose the shortest loan term possible that will allow you to meet your monthly payments. While a longer loan term will, of course, result in lower monthly payments, you’ll pay more for your car overall. Here’s an example:

Brian decides to buy a used car for $15,000. He puts down $5,000 and takes out a car loan at 9% for the remaining $10,000, and pays it back over 5 years, or 60 months. Although his monthly payment is only $285.48, he ends up paying $22,128.56 for his car over the life of the loan.

On the other hand, Susan buys the same $15,000 car, puts down $5,000, and takes out a car loan at 9% to cover the remaining $10,000. However, instead of a 5 year loan, she takes out a 3 year loan, or 36 months. Her monthly payments are higher, costing $437.33 monthly, but her car will only end up costing her $20,743.73 after her loan is paid off.

If you’re interested in crunching the numbers for yourself, we recommend playing with this auto loan calculator!

Step 6: Shop around for your car

Now comes the fun part! It’s time to shop around to find the perfect car for you!

When car shopping, you have a few different options. You can get your used car from a dealership, a private seller, or even one of those “car vending machines” like Carvana offers. But before you start shopping, it’s a good idea to research which car makes and models are the most reliable as the years go on. Not all used cars are created equal. Some makes and models have a better reputation for holding up over time. Purchasing a more reliable car can save you thousands of dollars in maintenance over the long run.

If you’re looking for a reliable used car and aren’t sure where to start, this article from Consumer Reports details the cars with the lowest maintenance costs over a period of ten years. Here’s a chart from that article too. Toyota for the win!!!

Once you’ve narrowed down your search to a few models, you can begin looking on the internet for a car that meets your criteria. Once you find something you like, be sure to test drive it to ensure you like the way it drives!

Step 7: Check the car history & schedule and inspection

Before you fall in love with a car, it’s crucial to make sure you check out the vehicle’s history report. This can give you important insights into who has owned the car in the past, what it was used for, and will detail any accidents or damage the car has suffered.

Review all the information thoroughly. You’ll want to avoid cars that have been in accidents, cars with salvaged titles, and ones that haven’t had routine maintenance. Some dealers will provide a history report for free, but if you’re shopping privately, you’ll have to obtain your own. You can purchase a vehicle history report from websites like Carfax or AutoCheck.

Also, be sure to schedule a car inspection with a mechanic you trust before you purchase any used car. A good inspection can protect you from purchasing a dud that will fall apart right after you buy it. Spending money here can save you thousands in the future. Even if the car you are buying comes with a clean history, this step is a necessity!

Lastly, it’s a good idea to google “common maintenance problems with xyz year/model”. The internet has awesome information on common vehicle defects, and you can check to see if your potential car has any potential looming expenses.

Step 8: Negotiate

No matter where you are purchasing your car, there is always room to negotiate. Don’t be afraid to ask for a lower price for the car you have your eye on.

When it comes to asking for a discount, it’s important to be realistic. For example, don’t ask to buy the car for half of what it’s actually worth. Do your research and come prepared with data that supports your ask. Remember to keep your cool if the answer is no. You can always walk away and buy your car elsewhere.

And even if they can’t budge on the price, see if there are any extra perks you could snag for free, like an extended warranty, free mats, or even a SiriusXM subscription!

Related: How to negotiate when buying a car

Step 9: Resist the dealer add ons

When you’re financing a used car, you want to pay as little as possible in fees and add-on expenses. Don’t let the seller or dealer trick you into things you truly don’t need. If you’re buying your car at a dealership, it’s likely that the dealer will offer to throw in a few extra features for a “super low price.” But spending more on your car than you need will only hurt you in the future.

If the dealer offers you a warranty on your car, make sure to do your due diligence before even considering it. Check to see if your used car still has the original warranty in effect. If you’re buying a certified pre-owned car, you may already have extended coverage on your car.

In all cases, you probably don’t need the extended warranty. A better option could be to save the money you would spend on the warranty into a sinking fund for car maintenance, and self insure as much as possible!

Step 10: Finalize your loan details

Once you and the seller come to an agreement, it’s time to finalize your loan details! Typically, if you’re buying your used car from the dealership, their financing department will try and offer you their own loan services. But, you are usually under no obligation to accept their financing terms. Bring all that research with you from step #4 when you got pre-approved, and use the lender that makes most sense to you financially.

Dealers have incredibly high markups not just on car prices, but financing options also. They are big profit centers. So bringing your own loan and negotiating financing outside of the dealership is key to getting the best deal. Don’t let the dealer bully you into accepting their high-priced loans.

If you’re buying from a private party or online dealership, you’ll need to get in touch with your individual loan provider for details on how to finalize your loan. This might require an inspection by the loan servicer (they want to make sure you are buying something that is absolutely worth the cost of the loan). If you get confused, don’t be afraid to get on the phone with customer service. Their job is to help ensure that you fully understand the borrowing process and to assist you in finalizing any last details.

Step 11: Take care of important documentation

When financing a used car, you’ll need to ensure all the relevant documentation is done correctly. Lenders will typically put a lien on your car title – meaning the car acts as collateral for them in case you don’t pay your loan. They can repossess the car if you default on your payments.

Dealers are the easiest to work with when it comes to documentation, as many have direct contact with the DMV. They mail you the title, handle all the registration, etc. If you buy your car from a private seller, you’ll need to make sure they take care of this.

You’ll also need to call your insurance company and ask them about the process of purchasing a new policy for your new-to-you car. Oftentimes there is a 30 day grace period in which your new car is covered by your older policy. After that, you’ll need to make sure you have a fresh policy set up for your new ride. However, be sure to contact your insurance provider to learn the ins and outs of your specific coverage.

Step 12: Repay your loan

Lastly you’ll need to make sure you make your car payments on time every month. We recommend automating your payments so that you’ll never be slapped with late fees if you accidentally forget to pay. With each payment, you’ll get closer and closer to fully owning your car!

If you can, make it a personal goal to crush your loan as fast as possible. You do this by throwing any extra savings each month to pay down the loan balance. The more you pay down, the less you’ll pay in interest, and quicker you own the vehicle free and clear!

The Bottom Line:

While we always encourage people to buy used cars with cash, if you’re going to finance a car, we want you to do it the right way! By setting a strict budget, shopping for the best rates, negotiating the best price possible, and paying off your loan as quick as possible, you’ll minimize the overall cost of your new car.

Once you pay off your car, drive it for as long as possible. The real win is getting to enjoy years without car payments, and putting all that money into investments for the future. Hopefully you can save up cash for an outright purchase the next time you need to replace your wheels.

Related Posts: