Maybe you’ve got a great investment opportunity but don’t have the cash currently to pull it off. Or perhaps you’re trying to catch up on your retirement contributions and are thinking about investing via leveraged funds. No matter the reason, is it a good idea to borrow money to invest?

Borrowing money to invest is more common than you might think. For example, when you take out a mortgage to purchase a property, you are in essence borrowing money (from a bank) to purchase an investment (an appreciating asset). Similarly, when you take out a student loan, you are borrowing money to invest in yourself with the goal of increasing future earning potential.

However, not all debt is created equal. When you borrow money for a house investment, education, or to start a business, this is typically classified as “good debt”. When interest rates are low, and fixed, and the asset is stable, borrowing money to invest can work out in your favor.

On the flip side, borrowing money to invest in cryptocurrency, hot stock tips, or a get-rich-quick scheme is far riskier. Not only is there more volatility and uncertainty in these investments, you’ll often be borrowing at higher interest rates. So it both costs more and there is greater downside.

What does borrowing to invest look like?

Financially speaking, it can make sense to borrow money for investing if the return on that investment will outweigh the cost of the loan. For example, borrowing money at an interest rate of 5% and investing in something that pays 10% returns can be a smart move. If calculated correctly, you can use “other people’s money” to make money yourself.

However, in reality, this is much easier said than done. That’s because usually there’s no guarantee that the investment you choose will have a higher ROI. There’s always a risk when you invest money! And many people underestimate the true cost of borrowing money.

Here are some common ways people borrow money to invest:

Taking out a personal loan to invest

This is when you borrow money from a lender and invest it however you please. Whether the new investment prospers or fails, you are personally on the hook for paying that money back.

Home equity line of credit (HELOC)

A HELOC is when you borrow money from a bank or mortgage lender, and they use your home as collateral for the loan. HELOCs typically have floating interest rates, which can be dangerous over the long term. If interest rates rise, your payments could become unmanageable.

Margin investing

This is when you borrow money from your broker, for example, Robinhood or Schwab, to invest in stocks. Margin investing requires at least some skin in the game, or cash deposit before you begin investing. Brokers typically multiply your buying power, charging you interest for investing any money above your cash deposit amount.

Margin investing amplifies your profit or your losses. If investments perform well, you can make great money and pay little in borrowing costs. But if investments perform poorly, your money can be lost swiftly and ruthlessly.

Margin trading and investing with leverage are one of the most common reasons people lose money investing in stocks. It’s akin to gambling. Don’t do it.

Long-term investors know that market downturns will come and go, and riding them out is part of the investing process. The longer you keep money invested, the less likely you are to lose money. But with margin investing you’re taking a gambler’s mentality. Your account can go to zero because you’re using money you didn’t have to invest in the first place. Brokers will force you to sell at a loss if you have no margin left.

So why do people borrow money to invest?

By now you might be wondering why folks bother risking so much to borrow money and invest.

Well, it’s because most starry-eyed optimistic newbie investors (or gamblers) only think about the potential upsides and ignore the downsides. They invest mostly based on hope and getting lucky, vs. mathematics and being patient.

Borrowing money to invest can accelerate wealth building, in theory. When you invest with borrowed cash, you’re able to purchase more investments than you otherwise would have been able to, meaning you can increase your potential returns. For example, if you invest $1,000 and earn 10% on your investment, you’ll have made $100. But if you borrow and invest $20,000 and earn 10% on your investment, you’ll have made $2,000, minus the interest and fees you’ll pay on your loan.

But with high highs, come low lows. And for most normal people just trying to build wealth for the future, most of these approaches are not worth the risk. Plus, with the interest and fees you’ll owe to the lender, it’s unlikely that the amount of extra money you’ll earn will feel worth the stress and anxiety of investing with borrowed cash.

Taxes on gains

Oh yeah, let’s not forget about taxes! For any gains you make on investments, you’ll have to pay taxes – either long term or short term capital gains. And depending on your current tax bracket, this could be a hefty percentage cut out of your profits!

While taxes aren’t always bad, they’re an often overlooked cost when it comes to overall ROI. If you borrow money to invest and only make a slim margin, taxes could minimize your profit severely.

The Risks of Borrowing Money to Invest

Borrowing money to invest comes with some serious risks and downsides. Here are just a few of the ways in which borrowing money to invest can hurt your finances.

Leverage can amplify your losses

Probably the biggest reason to stay away from borrowing money to invest is the fact that doing so can amplify your losses should the investment fail.

If you own something outright and it loses 20% of its value you still own 80% of it. But if you borrow money to invest and that investment goes down 20%, the results are far worse. In addition to the pain of watching your investments take a nosedive, you’ll have to deal with the double whammy of also needing to pay back your loan, plus interest!

It gets even worse. If you lose too much of those borrowed funds and aren’t able to pay it back in a timely manner, your lender could seize any collateral property and seriously damage your credit score. Borrowing money to invest can have devastating effects on your life. It’s almost like racking up a bunch of credit card debt after a big shopping spree – except you don’t even have anything cool to show for it at the end!

Your loan interest rate may not be low enough to make meaningful money

To put it simply, the higher your interest rate is to borrow money, the less likely it makes sense.

For example, if you were to take out a cash refinance on your home at 7% interest with the goal of investing those dollars, you would need your investments to grow by over 7% each year to see any profit on that money. With stock market returns averaging ~8-10% each year, that doesn’t provide you much margin. Plus, just because this is what stock market returns look like on average does not mean that these returns are guaranteed. Do you really want to risk it all to earn 1-3%?

To put that into perspective, getting a $100k HELOC and making just a 1% margin is only $1000 profit each year (that’s before considering fees, and taxes owed on gains). Is it worth taking on $100k in debt to maybe make $1,000? Nope. 🙅

HELOCs aside, the average personal loan interest rate is 12.22%. That’s WAY too high for most investments to truly make sense. If you believe your investment is going to consistently return more than that, you are either dreaming or exaggerating the potential return. Or you might be talking to the next Bernie Madoff.

Could hurt your debt-to-income ratio

If you take out a hefty loan to invest, it could hurt your DTI, or debt-to-income ratio. Your debt-to-income ratio is calculated by dividing your monthly debt obligations by your monthly gross income. For example, if you have a $300 monthly car payment, and a $500 student loan payment each month, and you make $3,500 each month before taxes, your DTI is about 22.8%.

Having too high of a debt-to-income ratio makes you seem like a risky borrower to financial institutions. This makes it more difficult to get approved for credit cards or loans in the future. It can also mean a lower credit score, and being offered higher interest rates when borrowing more money. Even some apartments can require you to have a low DTI to rent them. If you borrow money to invest, your debt-to-income ratio will increase until you pay your loan off.

Some personal loans don’t allow you to invest borrowed money

Even if you were able to find a personal loan with a low interest rate, some lenders don’t allow you to invest in stocks, mutual funds, or other common investment vehicles. Lenders know that borrowing money to invest can be akin to gambling, so they prohibit it when they give you money. For example, SoFi does not allow you to use their personal loans for real estate investing, business purposes, or investing in the stock market.

If you forget to read the fine print of your loan terms, you could end up paying fees to take out the loan and not even be able to use it for your intended purpose. Finding the perfect lender to borrow money to invest may be a more difficult task than you’d initially think.

Emergencies happen

I hate to sound like a pessimist, but just because you’re doing well financially right now, doesn’t mean that will always be the case!

The truth is, emergencies happen. People get sick, layoffs happen, and cars break down. And while you can take steps to hedge yourself against financial hardship by reducing your expenses, creating a bare-bones budget, and fully funding your emergency fund, investing borrowed money does the opposite.

Borrowing money to invest is like the antithesis of creating an emergency fund. You’re making yourself more vulnerable instead of protecting yourself. Something could happen in your life that could cause you to not be able to pay back your loan, and then you’d really be up a creek without a paddle.

It’s difficult enough to worry about finding a new job if you’ve been laid off. Imagine how much stress you would be under if you also had a completely unnecessary loan you couldn’t afford to pay back.

The only time you should borrow money to invest:

Despite all the associated risks with investing borrowed money, there is one specific, magic scenario in which it could make sense. And even then, you may find it isn’t worth the trouble.

The only time to ever even consider borrowing money to invest would be if you were offered an excellent APR. And if you could invest in a stable investment opportunity with a guaranteed return. For example iBonds, a CD, or interest within a high-yield savings account. In these cases, you’ll earn a set amount of interest each year, so if you’re able to get a lower APR, you can “guarantee” you’ll make money.

For example, if Uncle Chris wants to loan you $10,000 at 3% interest, you could theoretically deposit that money into a high-yield savings account and earn something like a guaranteed 5% return. Not bad!

Or if your parents want to loan you $100,000, interest-free, to invest in a rental property, take that money in a heartbeat. Invest it wisely and pay them back with the profits.

One note: With iBonds and CDs, you’ll need to leave that money put for a specific period of time. Otherwise you’ll incur penalties that will eat away at your earnings. That’s why even in this dream scenario, you might decide that it’s best to just stick to investing with your own cash.

Investing vs. Paying off Debt

Both investing and paying off debt are important to growing wealth. And there are some situations where one is more important than the other. For example, taking advantage of an employer 401k match is a priority in our 7 money gears. Most folks should invest in their 401k and get the match that’s offered from their employer before paying down consumer loan debt.

But, this doesn’t mean that taking on new debt is OK in order to prioritize investing. In most cases, paying down consumer debt takes precedence over investing. It’s another reason why borrowing money to invest rarely makes sense.

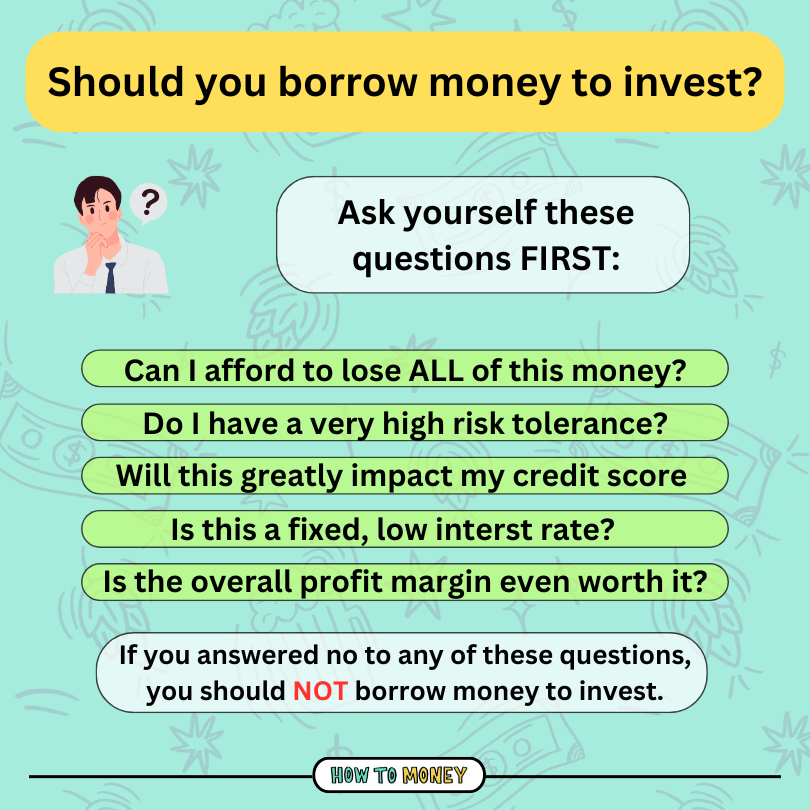

Questions to ask yourself before you borrow money to invest

If you’re still considering borrowing money to invest, ask yourself these questions before taking the plunge:

Think about all the risks. Can you afford to lose ALL the money, very quickly? What will life look like if you have nothing to show or your investing maneuver and are stuck with loan payments for months or years to come?

Adding more debt to your life can be stressful. Do you have a high risk tolerance and can you live peacefully while adding more debt to your life?

Your credit score and worthiness will be impacted when you borrow money to invest. Is that going to wreck any other areas of your finances?

Lastly, consider the interest rate and the true cost of the loan. If it’s cheap or free money, it could fall under the category of “good debt”. Also, carefully consider the investment you’re looking to buy, and make sure it’s a proven, stable asset with solid returns.

Alternative ways to build wealth

As tempting as it seems, you don’t need to borrow money to invest. Anyone can build significant wealth simply by spending less than they earn, and slowly and consistently investing their savings. Here are a few tried and true alternative methods to growing your net worth!

Dollar-cost averaging with index funds

Here’s the thing. A lot of folks are looking for a shortcut, but financially savvy folks know the power of small and consistent investing over time. With dollar cost averaging, you invest a set amount of money on a consistent basis, regardless of what the market is doing. And by investing with index funds, you’re broadly diversified across multiple industries, markets, and economies.

For example, a monthly transfer to your Roth IRA and investing in an S&P 500 index fund will make you a millionaire over the course of a few decades. Taking advantage of your workplace 401k, as well as investing in regular brokerage accounts are good options too.

We’ve covered this strategy in detail within our post about investing basics. It might be boring. But boring is the tried and true method for accumulating meaningful wealth.

Real Estate Investing

Real estate can be another great way to generate more wealth in the future. Purchasing a rental property can provide you with a secondary income stream, and help to diversify your investments.

Even better, if you can’t afford to purchase a rental property, there’s a good chance you can turn your own home into an investment by house hacking. Do you have some extra space you can rent out? Opting to do so can help lower your monthly housing costs, leaving you with more available money to invest each month.

Start a Side Hustle

If you wish you had more cash on hand to invest, consider starting a side hustle! Picking up some work outside of your 9-5 can help you sock away more for the future, eliminating the perceived need to borrow money to invest. Here’s some advice for choosing the perfect side hustle for you.

The Bottom Line:

Unless you’re Winklevoss-rich, or have a Ph.D. in financial economics and market analysis with the backing of larger financial institutions, it’s probably best to shy away from borrowing money to invest. At the end of the day, while it could accelerate wealth building, it’s usually not worth the risks involved. For every success story you might hear of folks who have borrowed money to invest, there are hundreds of folks who lost a significant amount of their savings doing so.

Instead of gambling, stick to the boring old basics of investing to grow your money in a surefire way. And focus all that excitement, energy, and creativity into other areas of your life.

Related Posts: