Advertiser Disclosure

* Advertiser Disclosure: How to Money has partnered with CardRatings for our coverage of credit card products. How to Money and CardRatings may receive a commission from card issuers. Some or all of the card offers that appear on the website are from advertisers. Compensation may impact on how and where card products appear on the site. Lastly, the site does not include all card companies or all available card offers.

We’re all for decluttering and simplifying your life. Why keep something around if you barely use it? But, when it comes to closing an old credit card, it actually makes more sense to keep the account open.

All credit cards, used or unused, play a key role in your credit reporting. If you close cards on a whim it may have long lasting effects that decrease your credit score and make other things in life more expensive, too.

In this post we’re going to cover:

- How closing credit cards affects your credit score

- Alternatives to closing a credit card

- When it might make sense to close one

- FAQ about closing cards

According to Bankrate.com, 12% of Americans actually think that closing a credit card will help their score as opposed to hurting it. Let’s correct that line of thinking right now.

Closing credit cards hurts your credit score

Using credit cards responsibly over time can help you achieve a great credit score. And credit scores hold major sway in our current economic system. Your score can affect everything from mortgage and car loan interest rates, to what you pay for your car insurance. That’s right, most insurers use your credit score to help determine the premiums you pay.

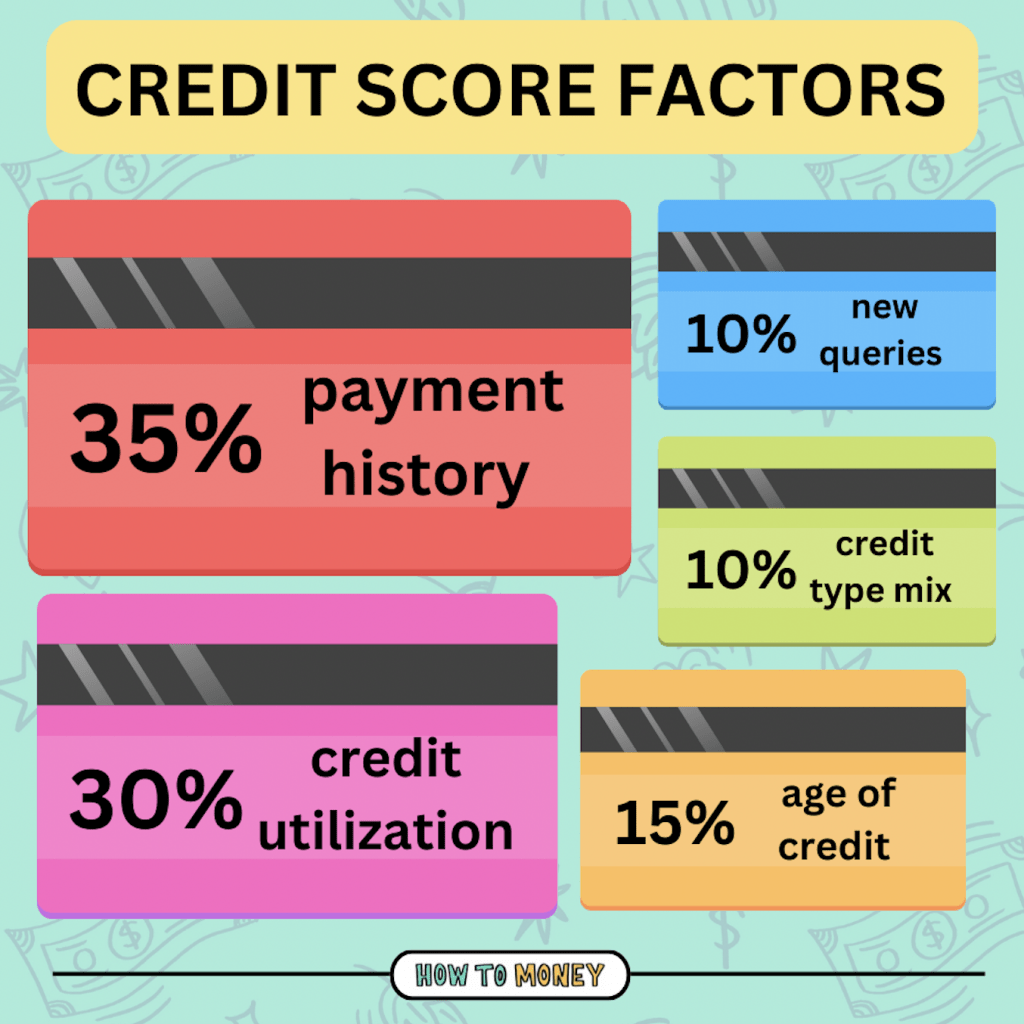

Canceling credit card accounts can have long-lasting negative effects on your credit score. And particularly if you’ve had that credit card for a long time. Here are the key components that make up your overall credit health.

In particular, we’re going to dive deeper into the 2 major components which are affected by closing cards: Credit utilization rate (30% of your score) and age of credit (15% of your score).

Credit utilization rate

The second most major component of your credit score (behind payment history) is your credit utilization rate. In normal human speak we’re talking about how much of your available credit you are actually using. When you close a credit card, you lower the amount of available credit that you have access to, increasing your utilization rate.

For example, if you have 2 credit cards, both with $10,000 credit limits, your overall available credit is $20,000. Now let’s say you regularly spend ~$5,000 across those cards… Your utilization would be 25% (5k divided by 20k).

Now let’s say you cancel one of your cards, lowering your total available credit limit to just $10,000. If you put all of your spending on the remaining card, your utilization ratio would shoot up to 50%! (5k divided by 10k).

As you can see, closing cards lowers your total available credit limit, increasing your utilization ratio. This may make you look like a more risky borrower, lowering your credit rating.

Pro tip: Always keep your utilization ratio as low as possible. Credit card best practices state that you should never have a utilization rate of more than 30%.

Age of credit

The next most important component of your credit score is the length of your credit history. The longer you have accounts in good standing, the higher your credit score goes. If you close a credit card that you’ve had for a while, you are hurting your score by closing that card.

Building up good credit history takes years, sometimes decades. So every time you close an account you’re kind of “erasing” some of that history, making your credit profile look younger.

Alternatives to closing a credit card

OK, hopefully we’ve convinced you to rethink closing any of your old credit cards. It’s not in your best interest. Now let’s go through some alternatives to consider:

1. Convert to a $0 annual fee card: One of the main reasons people cancel old cards is because they no longer want to pay the annual fee. (We get it, we hate fees too!!!) But what you may not know is banks can usually “transfer” your account to another card type, which keeps all your history and available credit line in place. Here’s a list of no annual fee cards you may be able to switch to!

2. Transfer your available credit: If you really want to close an account but keep your overall utilization ratio the same, some banks will let you transfer your credit limit from card to card. In the scenario we mentioned earlier, this would mean instead of having 2 cards with $10k limits each, you would downsize to 1 card but have an increased limit of $20k.

3. Keep using it (a couple of times a year): Make a plan to use old cards a couple of times each year in order to keep them active in your credit mix. Set a calendar reminder so you don’t forget or just use that card to automatically pay your Netflix bill every month. You don’t want your credit card issuer to cancel that card on you due to inactivity. That will also have negative consequences.

When is it OK to close a credit card?

So this begs the question, is it ever ok to close a credit card? The answer to this is yes – but it’s a rare situation indeed.

If you absolutely cannot stop using credit cards while there is an account open in your name, then limiting your access is of massive importance. I would recommend freezing your credit card and locking it away in the depths of your icebox. Seriously. Put your card in a Ziploc bag, fill it with water, and toss it in the back of your freezer. That can be a nice preventative step to keep spending at bay. But if that isn’t even enough, closing your account as a behavior modification to prevent yourself from overspending is your best course of action.

**If you truly need help getting out of deep debt, reach out to MMI or NFCC. Both of these are excellent non-profit resources**

Another situation where you might want to consider closing a credit card is for business accounts, or for joint ownership accounts. If you are getting a divorce or separating from a partnership, you’ll want to cut ties with anything that can negatively affect your credit.

That being said, if you are the primary owner of a credit card account and you want to remove an authorized user, that’s an easy fix by calling the issuer. Some credit card companies even let you add/delete user access within their mobile app. No need to cancel your entire account if you’re just trying to remove a user’s access!

Closing a Credit Card FAQ:

Here are a few frequently asked questions and things you may be wondering…

How much will closing a credit card impact my credit score?

The actual drop that you’ll see in your credit score will vary from person to person. That’s because the specifics of our individual credit score makeup are all particular to the individual credit choices we have made. For example, if you close a credit card that you opened just a few months ago that has a minimal credit limit, the impact will be slight.

If you close a card that you’ve had for 15 years that gives you access to a large line of credit, you’ll feel the impact acutely. Your credit score will take a beating for a decision like this.

Closing a credit card when shopping for a mortgage or auto loan only amplifies the mistake. If you are looking to take out a loan in the near future do not, for any reason, close a credit card.

Can I close a credit card with a balance on it?

Technically you can, but that’s really not a great idea. Even if you don’t plan to use the card, you’ll want to keep the account open while you pay the balance off. This makes sure all your payments are recorded properly and added to your payment history. It also gives you access to the line of credit in the future, vs getting another new card again later.

How many credit cards should I have?

There’s no magic number that suits everyone. We think having at least 3 is a good credit card strategy, as it allows you to broadly collect cash back and rewards across different types of spending.

If you can handle more cards and keep track of them without paying excess fees, go for it! But you may find diminishing returns as you continue to open credit cards after 10+. Keep it simple!

Do unused credit cards hurt your credit score?

If you leave cards untouched for too long you’ll run the risk of the bank closing the account due to inactivity. This can definitely ding your credit score due to throwing off your utilization ratio and shortening the age of credit lines.

This is why it’s extremely important to put at least some transactions on all your cards. Even if it’s buying a 25-cent banana every 6 months, keeping some activity is necessary.

Related: Here are some common credit score myths flying around you should be aware of.

What happens if I get a refund on a closed credit card?

Even though your account may be inactive, it can still have a positive or negative balance. If you receive a refund to a closed credit card, the issuer typically just applies the credit to your closed account. Then they’ll seek to mail you a check. Or in some cases they’ll reach out and ask how you’d like the money disbursed.

What happens to my points/miles if I close a credit card?

This differs a little from bank to bank, so it’s best to call and ask your specific credit card company. But, in general, if you are terminating your account fully (or transferring to a new card type), you’ll be forfeiting any unused points/miles/credits.

This is definitely something you should consider carefully before making major changes to your accounts. Use ALL your points and claim all your available cash back! Throwing points away is like flushing money down the toilet.

The Bottom Line:

If you’ve paid off your credit card balance or you just don’t use it very often, don’t close it! That credit card is often a vital part of your credit score – and having a good credit score has far-reaching impacts because of the way the world works today.

Having a few different credit cards can be incredibly helpful for lots of reasons. No matter how many you have, always be sure to follow the best practices when using credit cards!

Related articles:

- Our favorite cards for different spending patterns

- What’s in our wallet? (The CC’s we personally use).

- Tips to help build up your credit score

*Advertiser Disclosure: How to Money has partnered with CardRatings for our coverage of credit card products. How to Money and CardRatings may receive a commission from card issuers. Some or all of the card offers that appear on the website are from advertisers. Compensation may impact on how and where card products appear on the site. Lastly, the site does not include all card companies or all available card offers.

*Editorial Disclosure: Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

*User Generated Content Disclosure: Responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.