Artificial intelligence is rapidly growing in popularity and user adoption. And it’s not just for writing emails (or making adorable caricatures of yourself). When used correctly, AI can be a powerful tool to improve your personal finances. AI tools won’t magically help you get rich or offer novel investing insight, but they can help you understand your money situation better, uncover blind spots, and make smarter decisions with less effort.

For people who feel overwhelmed by budgeting, investing, or long-term planning, AI can act like a judgment-free assistant for your finances. Experian finds that 2/3 of Gen Zers are using AI to help them make personal finance decisions already. But AI is a tool that can be used for your benefit or for your detriment. It’s crucial to use it wisely.

Let’s dive into the practical, real-world ways AI can help you get smarter, more intentional, and more confident with your money.

Boost Your Budgeting with AI

Budgets don’t only fail because they are ignored. They also often fail because budgets are unrealistic, tedious, or built on guesswork instead of actual data. AI can help take the friction out of the budgeting process by turning your income and spending into a workable plan. Instead of starting with a blank spreadsheet and guessing, AI lets you begin with what you’re already doing, and make smart adjustments from there.

Step 1: Start With Your Real Numbers

It’s not that emotions don’t belong in the world of personal finance. But starting with the facts is crucial. Confronting your money habits can be tough, but you’re never going to make a meaningful impact on your future without using real numbers.

The best way to start? List out all your fixed expenses – think housing, utilities, insurance, car payments, groceries, childcare, other debt payments, etc. This is money that you need to spend each month. To find out how much money you’ll have after your fixed expenses are taken care of, you’ll have to subtract your total from your monthly net income.

Finding your monthly net income will depend on the type of employment you have. If you are a W2 worker, it can be as simple as adding up your paycheck totals each month. If you are self-employed or 1099, add up your monthly income, minus the percentage you set aside for taxes. If you have variable income, it’s a good idea to take an average for the year to have a solid starting place.

Once you have your monthly net income and your fixed expenses in hand, you can pinpoint your “fun money” budget by finding the difference between the two. It’s important to note any automatic deductions you’re making from your payment into a savings or investing account (like a 401k) to have an accurate number to have an accurate picture of how much you’re saving and investing.

Net Monthly Income – Fixed Expenses = Money for Savings, Investing, and Fun!

Step 2: Let AI Crunch the Numbers

Now that you have your numbers, feeding it into an AI software like ChatGPT or Claude can help you get organized. Here’s an example of a prompt you can use:

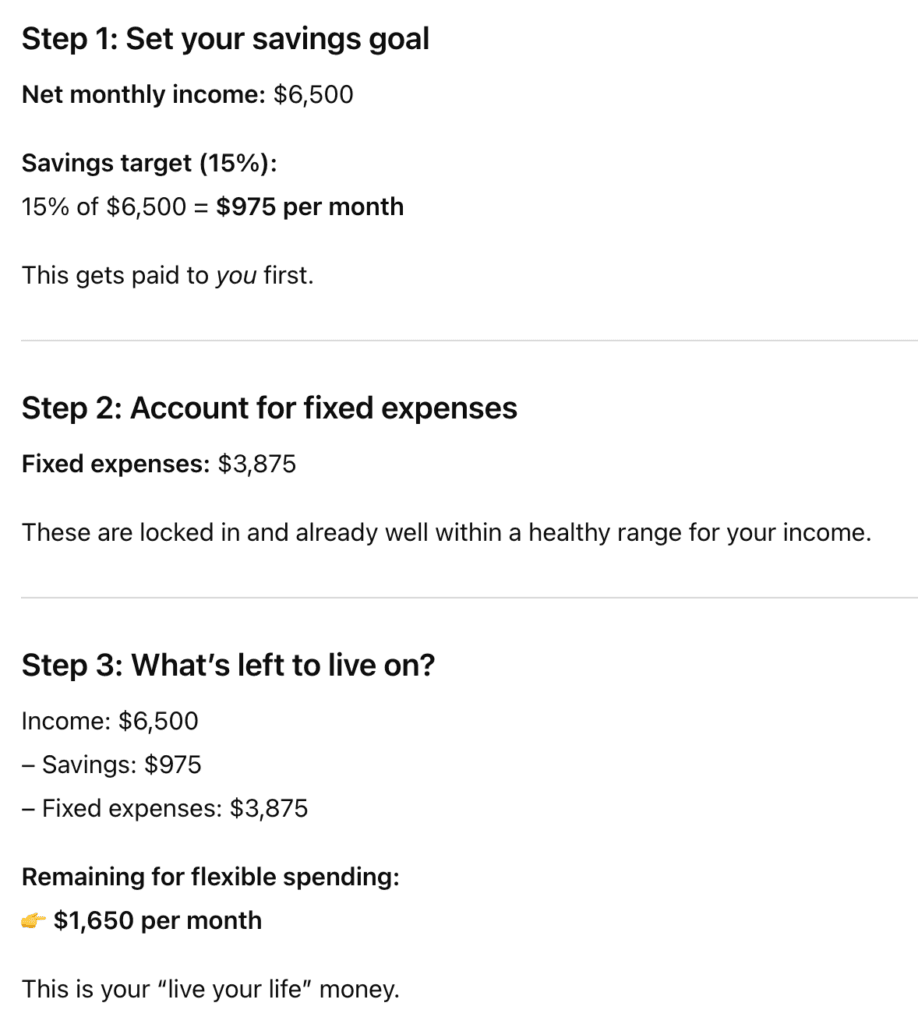

“I currently net $6,500 per month, and my fixed expenses come out to $3,875. I want to save 15% of my net income. Create a budget for me that allows me to save, but also gives me room to live my life.”

From a prompt like this, you’re likely to get a simple breakdown:

ChatGPT calls it your “live your life” money, we call it “fun money” – same deal. This is a high-level overview of your finances. Some people like to keep their fun money as one category and spend on any variable expenses out of that bucket. But if you prefer to break it down further, this is where AI can be even more useful.

If you use any kind of spending tracking app currently, you can pull reports from there to analyze your current habits. Or, you can simply pull your transaction data from your bank or credit card companies. From there, you can ask AI:

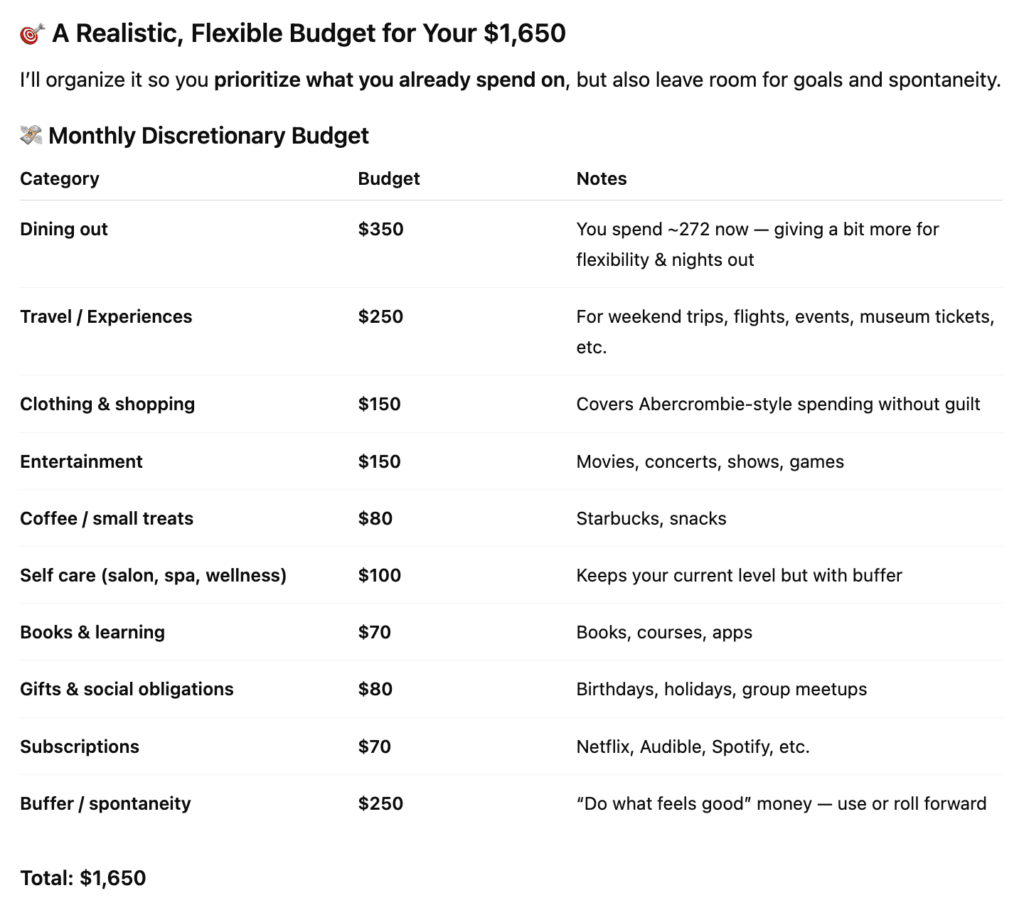

“Here is my current spending from the past 3 months. Please analyze the data and map out my highest spending categories. Then, build me a realistic budget using my disposable $1,650 of fun money per month.”

From that, you can get a more robust budget for your fun money:

Step 3: Adjust, Adjust, Adjust

Your first attempt at making a budget that will last often won’t be your final product. But the great thing about AI is that you can adjust and iterate as much as you want. You can ask AI to:

- Adjust your budget to increase your savings by a certain amount.

- Find problem areas of your budget and recommend ways to re-allocate that spending.

- Build a bare bones budget for emergencies.

If you have variable income, it can be especially useful to have a couple of different budgets (specifically one for lower-income months) to ensure you’re always staying in the green.

Step 4: Turn Your Budget into a System

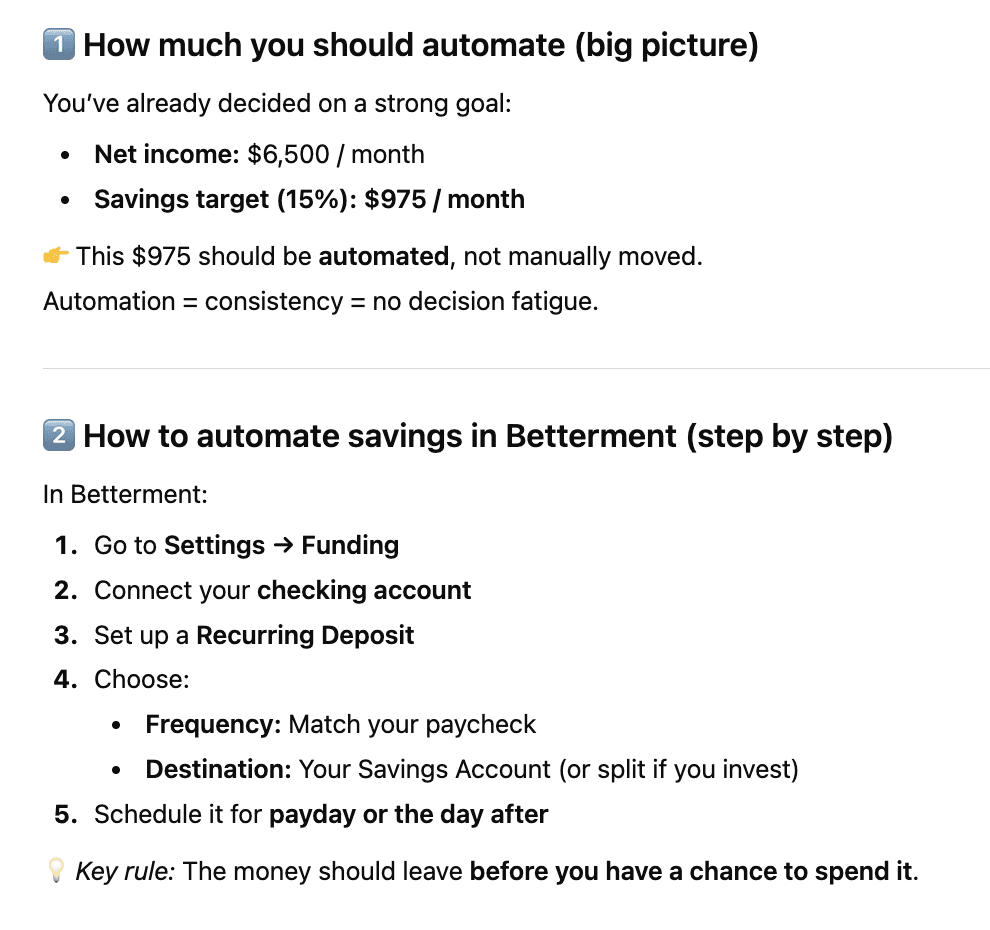

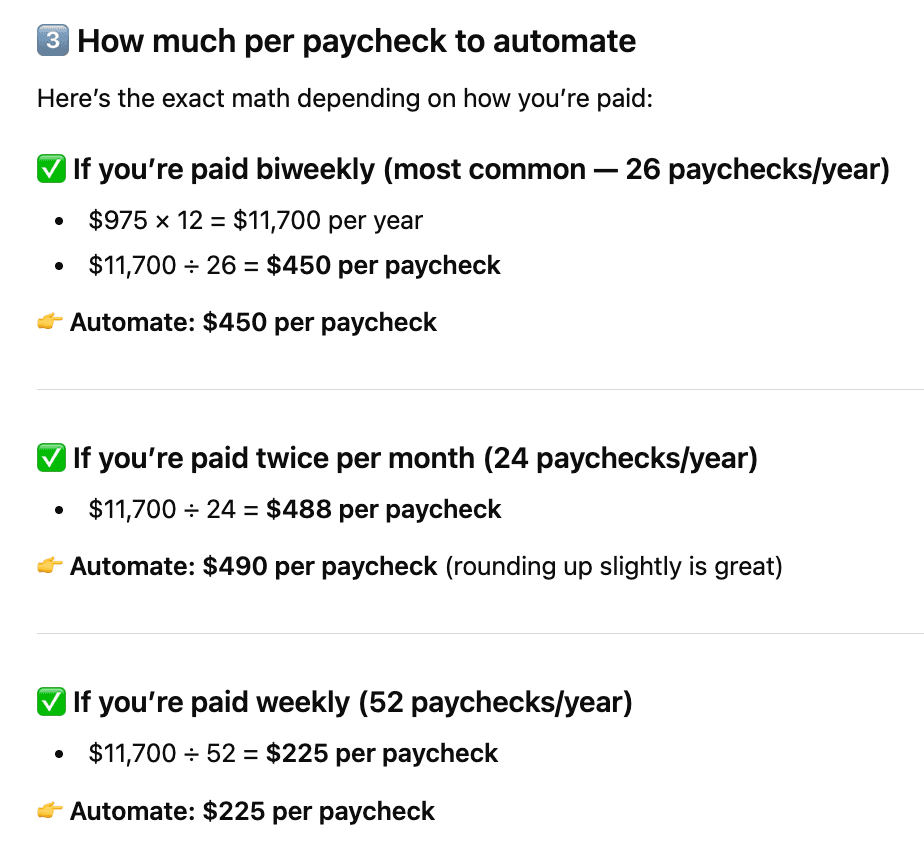

A budget only works if you stick to it, and the easiest way to stick to it is by having it run in the background of your life. AI can help you design systems that make saving and spending automatic, not something you have to think about constantly.

For example, you can use AI to:

- Decide how much to automate into savings after each paycheck.

- Plan sinking funds for vacations or other irregular expenses.

- Create guardrails for discretionary spending.

This shifts budgeting from a monthly task into an ongoing flow that adjusts as your life changes. AI won’t magically fix bad habits you might have picked up along the way, but it can make the budgeting process clearer, faster, and far less intimidating.

When you remove friction and guesswork, budgeting feels less like a punishment and starts feeling like a tool you can control. That’s when real progress happens.

Saving and Investing: Achieving Your Personal Finance Goals with AI’s Help

Having a budget is often the first step to getting your finances in order, but there’s much more that AI can help you out with. We already looked at how to automate your savings using AI, but what if you have multiple different savings goals? And we can’t leave out investing.

Artificial Intelligence tools can help bridge the gap between intention and execution by turning vague goals into clear, prioritized plans. Instead of juggling mental math and taking shots in the dark, AI helps you answer the questions that truly matter:

- How much do I need to save?

- How long will it take?

- What do I do if plans change?

Step 1: Get Specific About Your Goals

A savings goal needs to have certain things: a dollar amount, a deadline, and a purpose. AI can help you define these things, even if your purpose is really just “I should probably save more.”

You can start simple. Prompt AI with a general outline, such as:

“Help me define realistic savings goals based on my income and expenses.”

From there, AI can help break down your goals into categories, such as:

- Emergency Fund

- Short-Term Goals (travel, car maintenance, gifts)

- Long-Term Goals (down payments, new car)

This clarity makes it easier to understand what you want to prioritize and how to get there.

Step 2: Prioritize Your Goals

Most people aren’t saving for just one thing; they’re saving for everything… all at once. Saving also isn’t a one-size-fits-all proposition. AI can help you rank goals based on urgency, risk, impact, and your own personal feelings about each goal.

AI can answer tough questions like:

- How can I ensure I’m funding my emergency fund sufficiently while also saving enough to take a vacation next year?

- If I want to put more money into a down payment fund, what other spending categories should I pull back on?

This helps you create a plan that matches your values and lifestyle (even as changes occur), not just trying to fit your spending reality into a generic financial template.

Step 3: Create a Personalized Execution Plan

After prioritizing, AI can help turn your plan into actionable steps. It can calculate how much to save for each goal per month, suggest the best accounts to use, and, as we saw above, even offers specific advice to implement automatic transfers!

AI helps make things less complicated. For instance, you could ask it:

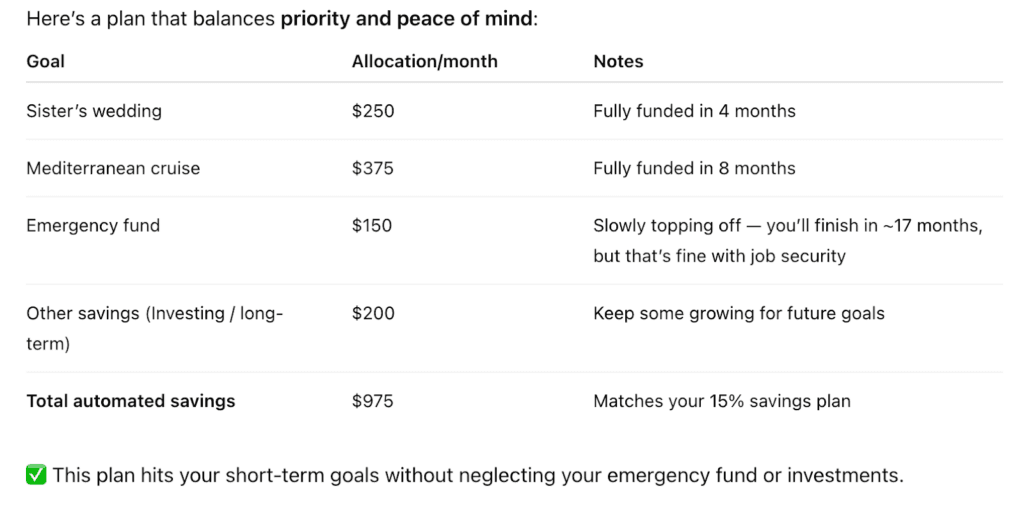

“I need an additional $2,500 in my emergency fund for it to be fully funded; however, I am not too worried since I have solid job security. I am more concerned about saving the $1,000 I need for my sister’s wedding in 4 months. I am also going on a Mediterranean cruise in 8 months that will cost about $3,000. I want to save for these goals, but I don’t want to neglect my emergency fund. How should I proceed with my savings?”

Even with specific goals and tolerance levels, AI can help you put all your thoughts into an organized plan. Not only does this save you time and headaches, but it also allows you to have a better understanding of when you’ll achieve your goals. That enhances peace of mind!

AI can also help you adjust quickly if life circumstances change. Maybe you get a raise, have an unexpected expense pop up, or have a shift in your priorities. This is where having a clear plan comes in handy – you can simply iterate instead of trying to build it all from scratch, or worse… work it all out in your head.

There may not be any way to make saving completely painless, but AI certainly makes it clearer. And when you know exactly what you’re saving for, how much it takes, and how your choices affect the outcome… saving becomes intentional instead of reactive. That’s how goals go from wishful thinking to funded reality.

Planning Retirement Goals with AI

Retirement can feel overwhelming. There are so many decisions to make, from how much to save to which type of account to how to invest your money. AI can act as a personalized sherpa or guide, helping you figure out exactly what works for your situation, timeline, and goals.

Step 1: Decide How Much to Save

One of the biggest challenges in retirement planning is knowing how much to contribute. AI can help you run personalized scenarios based on your income, expenses, and expected retirement age.

For instance, you can ask AI:

“I earn $80,000 a year. How much should I contribute monthly to retire at 65 with a comfortable lifestyle?”

That will likely give you a broad guideline, but one you can use as a starting point. From there, you can generate different models, such as prompting it with these questions:

- How much will I need to contribute if I start in 3 years?

- How will market growth assumptions impact my timeline?

- If I increase my contributions by 1% each year, how will that impact my timeline?

By comparing different scenarios, you can ensure your contribution amounts are realistic, achievable, and aligned with your vision of a great retirement.

Step 2: Choose the Retirement Account

If you have an employee-sponsored retirement account, you won’t have much choice on where your retirement funds are housed. You will, however, often have a choice between a traditional or Roth 401(k). AI can help you decide how much to contribute to each account by considering your current income, tax bracket, and expected retirement income.

You can ask questions such as:

- Which account will help me pay less in taxes over time?

- How will different contribution strategies impact my take-home pay and long-term savings?

- Should I split contributions between Roth and Traditional?

By running through personalized calculations, AI can help you choose the account type that maximizes your future wealth. If you don’t have access to an employee-sponsored retirement account, AI can also help you find other options, such as IRAs or Solo 401ks!

Step 3: Determine Your Asset Allocation

Once your contribution amount is set, the next step is deciding how to invest your money. The mix of stocks, bonds, and other investments is often based on your personal goals as well as your risk tolerance.

AI can help:

- Determine your risk tolerance based on your age, goals, and how comfortable you are with market swings.

- Suggest percentages of how much should be allocated to stocks vs. bonds.

- Rebalance your portfolio as you get older or as your retirement vision changes.

It’s important to note that we don’t think AI should be in charge of picking individual stocks for you to invest in. As great as it would be… AI isn’t a crystal ball. It’s not great at predicting the future and it can’t tell you what to invest in to become a millionaire overnight.

When it comes to where you invest, we always recommend low-cost index funds or ETFs. That’s because they are well diversified, and the fees are minimal.

Step 4: Automate and Adjust

Artificial Intelligence can also help you execute your plan and stay on track by:

- Setting reminders to increase contributions to your chosen account (or explaining how to automate them!).

- Tracking progress based on your goals.

- Helping you adjust contributions when you receive raises.

Your retirement plan is dynamic. It will likely change many times between now and when you’re ready to retire. AI can help you make these changes without it being overwhelming.

And while AI doesn’t replace professional advice, it does make retirement planning simpler and actionable. By helping you calculate contributions, compare account types, and allocate assets, AI takes the guesswork out of building a retirement strategy that works for you.

Keeping Travel Fun (and Less Stressful!)

Big expenses –- think vacations, weddings, home projects – are where budgets fall apart. Unfortunately, it’s easy to underestimate the total cost, especially in today’s age, where a quick search will show you a base fare, but not the total after all the extra fees are tagged on.

AI can help you reverse-engineer the experience: start with your budget, then build a plan that fits within it.

Step 1: Start With a Clear Budget

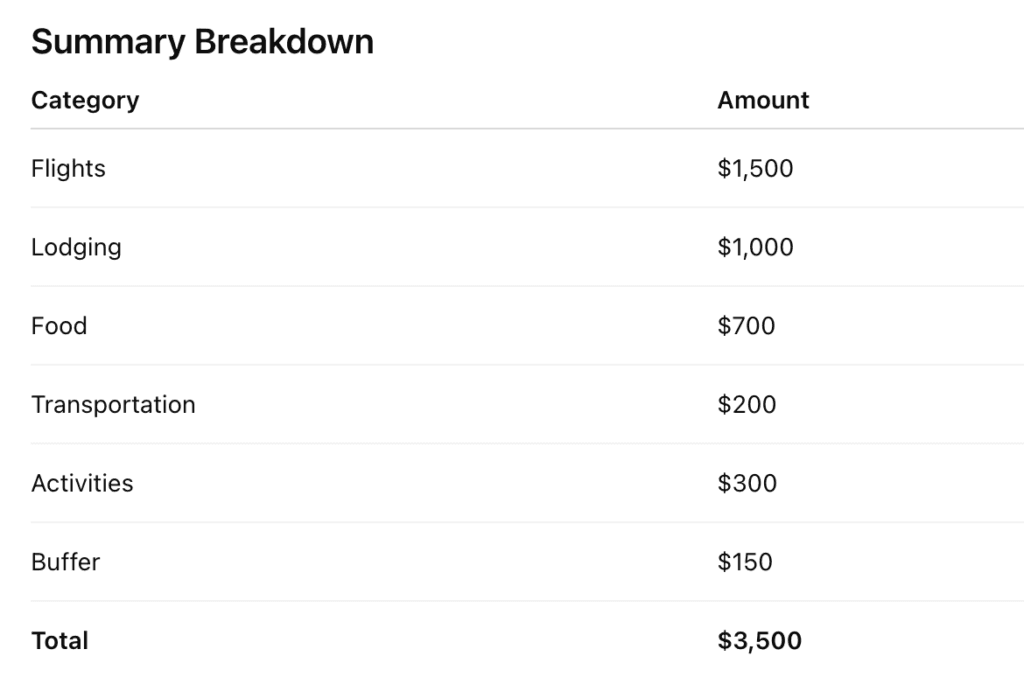

Before committing to a boujee vacation in Italy, give AI a number. You can ask it:

“I have $3,500 total for a 5-day trip to Italy for two people. That needs to cover flights, hotels, food, and activities. Help me break this down into spending categories.”

AI can help you put together a reasonable idea of how much you’ll spend on each component of your trip.

This gives you a general idea of how to break down your budget before you start browsing flights and booking activities.

Step 2: Have AI Help You Search Strategically

There are limitations to what AI can do, and you shouldn’t rely 100% on what it tells you. There are well-documented cases of AI hallucinations and inaccurate information. But AI tools can still help you search smarter and reduce the time spent comparing and contrasting options.

You can prompt AI with questions such as:

- What are the typical round-trip flight prices from NYC to Rome in September?

- What neighborhoods in Rome are affordable, but also centrally located?

- What is the average nightly cost for a 3-star hotel in that area?

By starting with guidelines like this, you can verify prices on your preferred booking platform and start building out your budget.

Step 3: Plan Your Activities

Excursions can often be the budget-buster of vacations. When you’ve already made it to a foreign country, and you see all the amazing activities available to you, it can be easy to think: “Well, I’m only here this one time, I have to try it!” By planning your days and activities in advance, you can avoid spending on a whim.

Try asking AI:

“With $300 allocated for activities in Rome, what experiences should I prioritize?”

AI can help:

- Rank different attractions.

- Suggest free or low-cost activities.

- Estimate ticket prices.

- Help you plan activities in an order that makes sense for your trip.

Once you pick out what you want to do, you could even have AI build you a sample itinerary!

Step 4: Decide How to Fund It

Building a dream vacation is all fun and games, but it’s important to make sure it’s a realistic goal. Planning when to go, what to do, and what to eat is exciting… planning on how to pay for it all could be daunting.

You might ask AI:

- How much should I save per month if I want to take this trip this Fall? What if I push it until Spring?

- I have X amount of credit card points. Can I use that for any portion of my trip?

- Is this trip reasonable given my other financial goals?

By creating a plan, you keep your travel aligned with your other money priorities, instead of letting it become the reason you delay them.

And this doesn’t just work for travel and vacations – any large expense, such as a wedding, repair, or business venture, can be aided using AI. Start with your total number, break it down, compare options, and adjust. AI is a tool to wield for your benefit. By being in control of your spending, you can tackle large goals without future regret.

Best Practices For Using AI as a Tool to Help With Your Personal Finances

AI can be a powerful tool for organizing and planning your finances, but only when used intentionally. The goal isn’t to hand over control; it’s to make better decisions, faster, with less stress. There are a slew of great ways to use AI to help you out. There are also a lot of ways you shouldn’t be using AI.

Do: Use AI to Clarify Goals and Priorities

AI excels at helping you turn vague intentions into concrete plans. You can:

- Ask it to help rank goals by urgency, timeline, and emotional importance.

- Use it to visualize tradeoffs.

- Revisit your goals as life changes.

Financial decisions are rarely about the math alone. AI can help structure your thinking and build a plan that works for you.

Don’t: Treat AI Like a Crystal Ball

Again… as nice as it would be, AI cannot predict market shifts, guarantee returns, or account for unexpected life events. You should avoid:

- Asking for “can’t miss” investment ideas.

- Trying to time the market based on AI’s predictions.

- Having blind faith in any and all AI responses.

Do: Use AI for Budgeting and Scenario Planning

AI can help you plan out the endless “what if” questions. You can have it:

- Test how different savings rates affect your timelines.

- Compare spending tradeoffs before pulling the trigger.

- Help you plan for large expenses.

Don’t: Share Sensitive or Personal Identifiable Information (PII)

You should treat AI like you would any site. You should never input:

- Bank account numbers.

- Social security numbers.

- Login credentials.

- Security questions.

In modern society, information leaks happen regularly. You never know where your information could end up. A good rule of thumb is that if you wouldn’t post the information publicly, you shouldn’t be sharing it with a large language model.

Do: Ask for Explanations

AI isn’t a close personal friend. Asking “What should I do?” may not get you a very useful answer. Instead, ask more pointed questions, deliver information, and allow it to help you decide how to proceed, such as:

- What are the pros and cons of this option?

- What assumptions are going into this decision?

- What would happen if my income changed or I had an unexpected expense?

Don’t: Let AI Override Professional Advice

AI is a planning and education tool, not a licensed advisor. It should not replace professional advice if that is what you’re looking for, but it can:

- Help you prepare questions before you interview a financial professional.

- Break down the advice given to you and help you synthesize it.

If you’re looking for professional help (or you’re not happy with your current advisor), you should check out our review of Wealthramp.

Do: Use AI to Stay Consistent

AI can serve as a journal for your financial goals. It’s great for:

- Monthly budget check-ins.

- Savings milestone tracking.

- Reframing setbacks without judgment or shame.

Don’t: Continuously Chase Optimization

While AI is great for answering what-if questions and being able to tweak things for every possible scenario, don’t get stuck in a never-ending cycle of improvement iterations. Technically, AI can generate endless “better” versions of a plan. To prevent yourself from perfection paralysis:

- Avoid constant tweaking of budgets or plans.

- Choose a “good enough” plan and begin executing.

At the end of the day, AI works best in personal finance when you wield it wisely as a support tool, when it supports your judgment, not as a way to farm out your decisions. Use AI intentionally to plan, test, organize, and reflect – but keep final decisions consistent with your values, risk tolerance, and real life.